The money we use every day, this financial system, is actually standing on a colossal, invisible structure of ’trust’. And at its deepest core, the bedrock supporting everything, is ‘US Treasury Bonds’. Thanks to this system, the world has experienced unprecedented growth, but now… that bedrock has begun to shake. As the structure, where the entire world relies on the ‘debt’ issued by a single nation, reaches its limit, “creaking” signals are appearing throughout the system.

This article is a journey to dissect the heart of the modern financial system, diagnose the problems within it, and explore why new alternatives have become necessary. The key keywords of this journey are just three: ‘Trust’, ‘Collateral’, and ‘Liquidity’. Civilization ultimately moves by ‘belief’. The piece of paper holds value because of the belief that it is ‘money’, and the promise of a nation to ‘repay’ makes ’treasury bonds’ the safest asset in the world due to the belief in that promise. This article aims to discuss how that belief is created and maintained, and what future unfolds before us when that belief begins to crack.

Part 1: The Pyramid of Trust and a World Where ‘Debt’ Became Money

1.1. The Hierarchical Structure of Modern Finance: A Pyramid Supporting the World

The easiest way to understand today’s financial system is to think of the ‘Pyramid of Trust’. This pyramid is composed of multiple layers of money and credit, structured so that more fundamental and secure assets are located on the lower layers.

In the past, ‘gold’ was at the very bottom of the pyramid. But today, that position is occupied by ‘US Treasury Bonds’. US Treasury Bonds are the ultimate refuge sought by everyone in times of crisis, and are virtually considered a ‘risk-free asset’.

| Layer | Financial Asset | Simplified Explanation |

|---|---|---|

| Layer 1 (Bedrock) | US Treasury Bonds | The ultimate collateral that serves as the benchmark for all financial activities. The very ground of this pyramid. |

| Layer 2 | Central Bank Reserves | The vaults of central banks. Most are filled with US Treasury Bonds. |

| Layer 3 | Commercial Bank Money | The money we deposit in banks. Banks create this money by using collateral like treasury bonds. |

| Layer 4 | All Credit Products | Stocks, corporate bonds, real estate loans, etc. All value is priced based on Layer 1 treasury bonds. |

The stability of this entire pyramid depends on how strong the bottom layer, the bedrock, is. If there’s a problem with the reliability of US Treasury Bonds, it’s not simply a matter of bond prices falling. It becomes a truly colossal threat that could bring down the entire building of the financial system.

All financial products are essentially ‘rights to receive something later’, in other words, claims. A bank deposit is the right to demand money from the bank, and a loan held by a bank is the right to receive principal and interest from the borrower. In times of crisis, people abandon uncertain claims and rush towards the lower layers of the pyramid, seeking more certain claims. It’s like people evacuating to higher ground during a flood. They sell corporate bonds to get cash (bank deposits), and if banks are unstable, they withdraw cash to hold banknotes (issued by central banks) in their hands.

And even central banks of various countries hold US Treasury Bonds as their ultimate safe asset. The destination of this “flight to safety” has always been US Treasury Bonds. But what if the safest place everyone flees to, the US Treasury Bond itself, becomes the source of risk? A situation where there’s nowhere left to run. This is the fundamental dilemma facing modern finance.

1.2. The Evolution of Collateral and Currency: A World Where Debt Became Money

Historically, money was based on tangible assets with intrinsic value, like gold. But today’s money is based on ‘debt’. It’s a remarkable paradox to call US Treasury Bonds a “pyramid of trust operating as debt.” The fact that the safest asset in the world is actually the ‘IOU’ from the US government, the world’s biggest debtor. This belief relies on the historical fact that “the US government has never defaulted on its debt since its founding.”

The fact that the US dollar is the world’s reserve currency further solidifies this system. To conduct global trade, dollars are needed, and the safest place to hold dollars earned through trade is ultimately the US Treasury Bond market. This gives the US an incredible privilege, like an unending spring, to borrow money at low interest rates whenever needed.

Within this structure, the US national debt is no longer just a US problem, but a kind of ‘public good’ that keeps the global financial system running. Just as air and water are needed for the world to function, safe and abundant dollar-denominated collateral assets, namely US Treasury Bonds, must be continuously supplied for the financial system to operate. This is a tremendous benefit for the US, but also a structural constraint that forces it to continue increasing debt regardless of its own fiscal condition.

Let’s take an example. If a Korean company exports semiconductors to Germany, it receives payment in dollars. This company needs a safe place to store and manage the earned dollars, and the first place it thinks of is the US Treasury Bond market. As countless transactions like this occur globally every day, enormous demand for US Treasury Bonds is constantly generated. Ultimately, the US issuing debt is not a bug for maintaining the current system, but an essential feature.

Part 2: The Heart of the System and Signs of Its Cracks

2.1. The Repo Market: The Hidden Heart of the Financial System

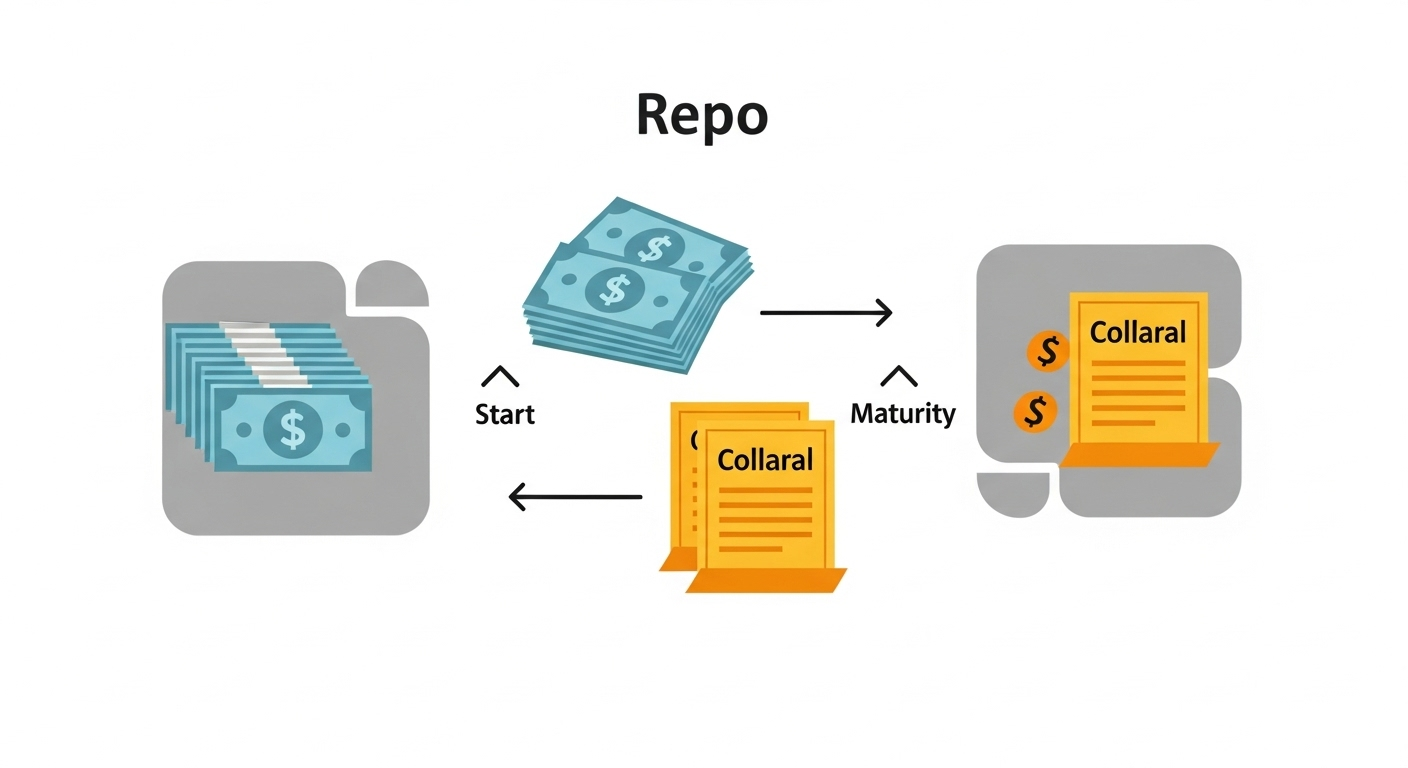

If the financial system were a vast city, the repo market would be like a complex ‘underground water pipeline’ supplying water to the entire city. It’s not easily visible, but the moment this pipeline gets blocked, the city immediately grinds to a halt. A repo is a transaction where financial institutions pledge high-quality assets like US Treasury Bonds as collateral and borrow cash for very short periods, like one or two days. Simply put, it’s a ‘bond pawn shop’. That’s exactly what it is. In this market, US Treasury Bonds are treated not just as securities, but as cash itself.

No matter how much water (money supplied by central banks) is in the city’s reservoirs, it’s useless if the water pipelines (repo market) that deliver water to each household are blocked. Financial institutions access the ‘water pipes’ of the repo market through the ‘faucets’ of treasury bonds to procure urgently needed cash.

This vast underground market is connected to our daily lives. For example, when we buy a car on installment in Korea, a financial company (e.g., Hyundai Capital) acquires the ‘right to receive money every month’. The financial company bundles thousands of these loan receivables to create a product called an ‘Asset-Backed Security (ABS)’, and can borrow ultra-short-term dollar funds in the repo market in New York using this security as collateral. The car installment payments made by a consumer in Seoul contribute to the liquidity of the New York financial market. It’s quite fascinating. In this way, the financial water pipes span the globe, and a blockage in one place affects the water pressure everywhere.

2.2. A Lesson from a Collapsed Trust: The LIBOR Scandal

LIBOR, the benchmark for trillions of dollars in loans worldwide for decades. Ah, this is a prime example that dramatically illustrates the flaws in this trust system. LIBOR was calculated by averaging the ‘subjective estimates’ submitted by a small number of large banks in London, who stated, “We estimate we could borrow money at this interest rate.” It was essentially a ‘gentlemen’s agreement’.

However, in 2012, the shocking truth was revealed that these banks had been colluding and manipulating interest rates for years for their own profit. This was not just a few banks’ misconduct. The fact that the most critical benchmark of the system was based on ’lies’ shook the trust of the entire financial world to its very core. The old trust system, based on ‘honor’ and ‘relationships’, had completely collapsed.

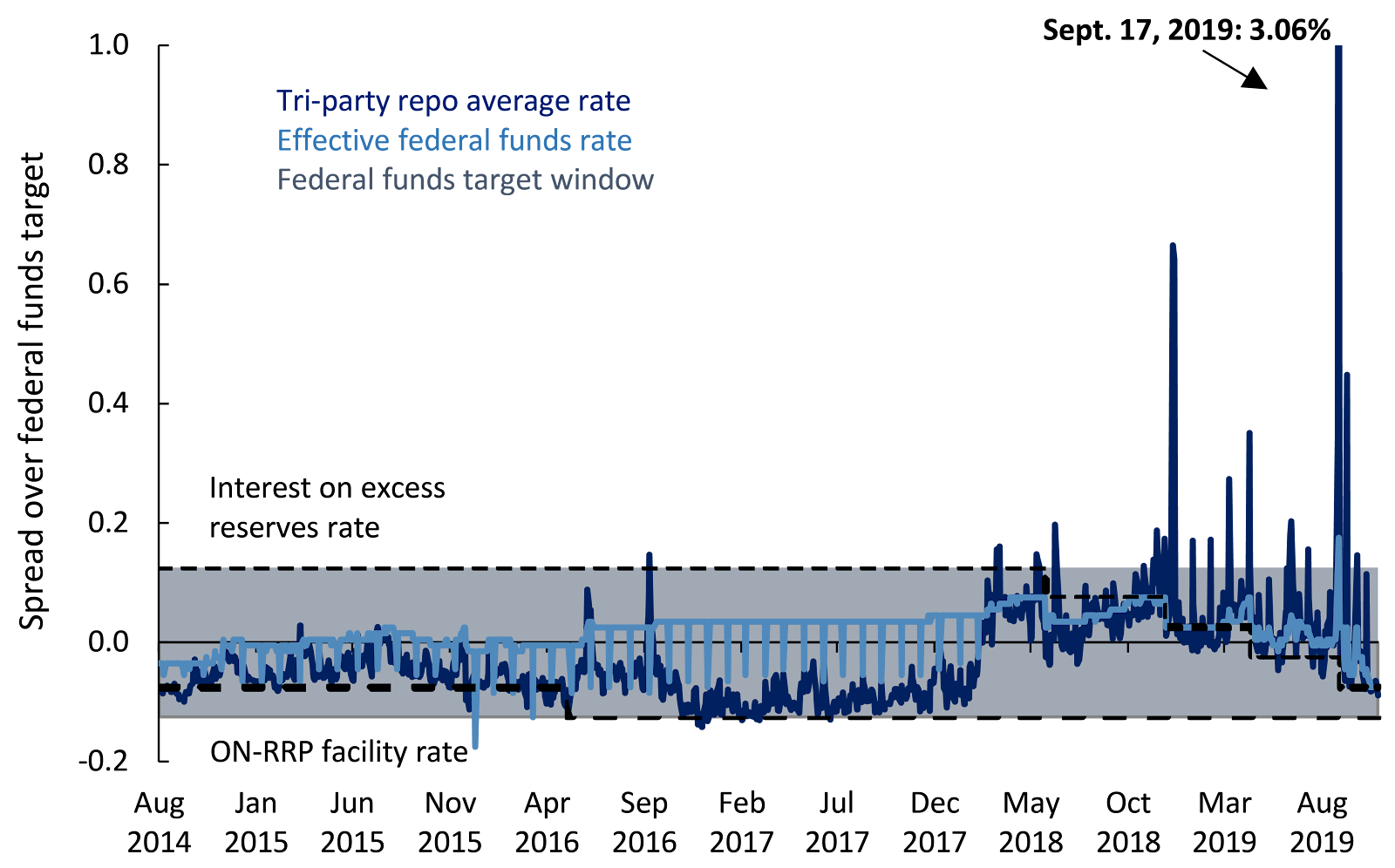

2.3. In-Depth Analysis: September 2019, the Day the Financial System’s Heart Nearly Stopped

Following the LIBOR incident, the financial world needed a new benchmark interest rate that was more transparent and impossible to manipulate. Thus, SOFR was introduced. SOFR is calculated not based on banks’ ’estimates’, but on interest rates that were ‘actually traded’ in the repo market, using US Treasury Bonds as collateral, as explained earlier.

On the surface, this seemed like a reasonable solution. However, it harbored a truly fatal implication: it resulted in tying the global financial system even more deeply, or rather, subordinating it, to a single collateral asset: ‘US Treasury Bonds’.

And on September 17, 2019, a chilling incident occurred in that very repo market, where the system’s heart nearly stopped. The repo rate, which normally hovered around 2%, suddenly spiked to over 5% and even 10%. This was akin to the ATMs of major financial institutions suddenly malfunctioning. While market liquidity was temporarily depleted due to the overlap of corporate tax payments and new treasury bond issuances, even large banks that had ample cash due to stricter regulations since 2008 hesitated to lend, thinking, “Uh oh, I’m scared too.”

| Date | SOFR Rate (%) | Description |

|---|---|---|

| September 13, 2019 (Fri) | 2.20 | Calm state |

| September 16, 2019 (Mon) | 2.43 | Pressure begins from tax payments and treasury settlement |

| September 17, 2019 (Tue) | 5.25 | Interest rate spike, Fed begins emergency intervention |

| September 18, 2019 (Wed) | 2.55 | Stabilization begins due to Fed intervention |

| September 19, 2019 (Thu) | 2.15 | Returns to normal levels |

As the market neared paralysis, the central bank, the Fed, had to inject hundreds of billions of dollars in emergency funds directly into the market for the first time since the 2008 financial crisis. The 2019 crisis revealed a crucial fact: the financial system had become so dependent on the Fed’s constant support that it could hardly function without it, effectively becoming addicted to central bank intervention.

2.4. The Paradox of Trust: Dependence Grows Stronger in Crises

A peculiar paradox exists in the modern financial system. The more crises occur, even when those crises originate in the US, global capital flock to US Treasury Bonds. The 2008 financial crisis began in the US housing market, yet investors worldwide sold European stocks and emerging market bonds to buy US Treasury Bonds. Even when the global economy stalled due to the COVID-19 pandemic, demand to buy dollars and US Treasury Bonds surged.

In other words, the system’s biggest problem simultaneously becomes its strongest supporting force. However, this paradox cannot last forever. All of this is based on the absolute belief that “even if everything else collapses, the US government will not fail.” However, as the US national debt grows to unimaginable levels, a new kind of risk is emerging.

Part 3: The River of No Return and the Search for New Collateral

3.1. Structural Cracks: The US Debt Trajectory

It’s time to look at the grim reality that threatens the very concept of a ‘risk-free asset’: the US fiscal situation. The US national debt has already surpassed $36 trillion, a figure far exceeding 120% of the US’s total economic output (GDP).

| Year | Debt-to-GDP Ratio (%) | Key Events |

|---|---|---|

| 1946 | 106.1 | Peak after World War II |

| 1981 | 31.8 | Low point before the Reagan administration |

| 2007 | 35.0 | Pre-global financial crisis |

| 2020 | 126.3 | Response to COVID-19 pandemic |

| 2024 (Current) | Approx. 123.0 | Continuous increase |

| 2034 (Projection) | 116.0 | CBO Projection |

| 2054 (Projection) | 172.0 | CBO Long-term Projection |

The more serious problem is that this debt increase is not due to temporary economic downturns, but is a structural problem caused by fixed expenditures like pensions and healthcare, and snowballing interest payments. The US is now trapped in a vicious cycle of borrowing new money to repay the interest on existing debt.

As the scale of debt grows, the nature of a ‘risk-free asset’ fundamentally changes. The real risk is no longer ‘credit risk’ of not receiving promised money, but the ‘risk of losing purchasing power (inflation)’ where the value of the promised money is drastically diminished, even if received. US Treasury Bonds are, frankly, only ‘risk-free’ in name.

3.2. Seeking Alternatives: Conditions for an Ideal Collateral Asset

With the structural problems of the US Treasury Bond-centric system becoming evident, we naturally arrive at the question, “Well then, what is the alternative?” If we were to design an ideal collateral asset for the future global financial system from a blank slate, what conditions would it need to meet?

- Political Neutrality: It should not be subject to the political or economic situations of any specific country.

- Absolute Scarcity: Its supply should be fixed, meaning it cannot be arbitrarily printed.

- Not ‘Debt’: The asset itself should not be someone else’s liability. (Completely eliminating the risk of default)

- Digital Age Compatibility: It should be transmissible and divisible quickly and easily across borders.

- Transparency and Verifiability: Its ownership and authenticity should be verifiable without third-party institutions.

Existing assets do not meet all these conditions. Gold is scarce and neutral, but it’s heavy and difficult to handle, making it inconvenient in the digital age. Treasury bonds of other countries carry the risks of those countries, so they cannot be alternatives.

3.3. The Essence of Bitcoin: Potential as ‘Collateral’

It is at this point that Bitcoin begins to be discussed as an alternative. Many people misunderstand Bitcoin as merely a volatile speculative asset, but its essence is different.

Bitcoin is not a company or organization, but a massive public ledger (blockchain) maintained by computers worldwide, and the rules (protocol) governing it. Bitcoin’s true innovation lies in the ability to ‘directly own (Self-custody)’ digital assets entirely through a private key that only you know, without intermediaries like banks or securities firms.

This is like keeping physical gold bars in your own basement (’the asset itself’), rather than entrusting gold to a bank (which is a ‘claim’ on the bank). If modern finance is a chain of numerous ‘claims’, Bitcoin, owned directly, can break that chain and become a pure ‘asset’ in itself, not owing anyone.

3.4. Experiment: Decentralized, Trust-Minimized Collateral

Understanding the essence of Bitcoin, let’s compare it with the conditions for an ideal collateral asset defined earlier. As Professor Tae-min Oh argues, Bitcoin is the first experiment to shift the subject of trust from governments and banks to the immutable ‘code’.

| Characteristic | US Treasury Bond | Bitcoin |

|---|---|---|

| Issuer | US Government (Centralized) | None (Decentralized network) |

| Trust Model | Belief in the US government’s ability to repay | Belief in mathematical and cryptographic code |

| Supply | Can be issued indefinitely | Fixed permanently at 21 million coins |

| Essence of Asset | Someone else’s ‘debt’ (risk of default) | ‘Asset’ that is no one’s debt (no risk) |

| Payment Method | Requires intermediaries, takes days | No intermediaries needed, near-instant P2P payments |

| Political Neutrality | Low (Can be weaponized based on US interests) | High (Belongs to no country) |

Bitcoin’s true disruptive power lies not in replacing dollars for buying coffee at a store, but in challenging the exclusive position US Treasury Bonds have held as the ultimate, neutral collateral asset for the global financial system over the past 50 years. Bitcoin has combined the properties of gold (scarcity, neutrality) with the properties of digital assets (mobility, divisibility) for the first time in history. Therefore, Bitcoin’s emergence is the first meaningful competitor to the role of ‘ultimate collateral asset’ that US Treasury Bonds have monopolized for the last 50 years.

3.5. From Theory to Reality: Bitcoin Beginning to be Used as Collateral

This discussion is no longer confined to theory. This is important. In reality, world-renowned investment banks like Goldman Sachs have entered the Bitcoin collateralized lending market, and a Bitcoin collateralized lending market worth billions of dollars has already been formed within the crypto asset industry.

Companies are leveraging their Bitcoin holdings as collateral to borrow cash for business expansion or personal needs like real estate purchases, without selling their Bitcoin. This is a crucial example showing that Bitcoin can function as a useful collateral supporting productive economic activities, beyond being a mere speculative asset. The fact that sophisticated financial players are building infrastructure to treat Bitcoin as valid collateral is the first step towards the possibility of Bitcoin being used as a core collateral to generate liquidity in the repo market, much like treasury bonds.

Part 4: Conclusion - A New Strategic Asset and the Future of Finance

The escalating US debt problem and the recurring political clashes over raising the debt ceiling are steadily eroding the existing trust in dollars and treasury bonds.

Remarkably, beyond some analysts, even politicians have begun to mention Bitcoin as one of the solutions to the national debt problem. Proposals are being made for the US to stockpile Bitcoin as a ‘strategic reserve asset’ for the nation, similar to how it holds gold. This is seen as a strategic card to support the value of the dollar and counter the ‘de-dollarization’ movements of competing nations like China and Russia. The fact that discussions once considered science fiction ten years ago are now taking place in real politics underscores how severe the instability of the current debt-based system is.

This article has been a journey that began with US Treasury Bonds, considered the solid foundation of global finance, and explored the deep cracks hidden beneath that foundation. The 2019 repo market crisis and the ever-increasing debt are clear signals that this system can no longer function as it once did.

The global financial system stands at the precipice of a massive paradigm shift. The 50-year monetary experiment based on the ‘debt’ of a specific nation is now hitting its logical limits. The effort to find new forms of collateral assets that are politically neutral, have a limited supply, and are not anyone’s debt is no longer just the imagination of a few, but has become a historical inevitability.

Considering these conditions comprehensively, Bitcoin, with its absolute scarcity, political neutrality, and suitability for the digital age, is the most promising, perhaps the only, candidate capable of fulfilling this role at present. Therefore, as the title of Professor Tae-min Oh’s book suggests, imagining a future financial system without considering Bitcoin is… well… becoming increasingly difficult.

References

- No Future Without Bitcoin _ Tae-min Oh

- Relationship Between Civilization and Trust _ YES24 Book Introduction

- The Status of US Treasury Bonds as a Risk-Free Asset _ SisaIN

- US Treasury Bonds as a Safe Haven Asset _ Naver Pay

- The Triffin Dilemma and Dollar Hegemony _ Aladdin Book Introduction

- Definition and Function of Repo (Repo) Transactions _ Mirae Asset Securities

- The Role of the Repo Market and US Treasury Bonds _ EBC

- Types and Methods of Repo Transactions _ Korea Capital Market Institute

- Composition of the Repo Market _ Shinhan Investment & Securities

- LIBOR Collusion Scandal _ Yonhap Infomax

- Impact of LIBOR Rate Manipulation _ Anti-Corruption and Civil Rights Commission

- Analysis of the September 2019 Repo Rate Spike _ Woori Financial Management Research Institute

- Definition and Introduction Background of SOFR _ Woori Financial Management Research Institute

- Analysis of Causes of the 2019 Repo Rate Spike _ Economy21

- SOFR Interest Rate Trends _ TradingEconomics

- US National Debt Outlook _ Wikipedia

- US National Debt Status _ TradingEconomics

- US Debt-to-GDP Ratio _ Korea International Trade Association

- CBO Long-Term Budget Outlook (2020) _ The Korea Times

- CBO 10-Year Outlook (2024) _ CBO

- US Treasury Bond Issuance and Interest Burden _ KB Asset Management

- Goldman Sachs’ Entry into the Bitcoin Collateralized Lending Market _ Korea Economic Daily

- Coinbase’s Bitcoin Collateralized Lending Program _ Digital Today

- Examples of Expansion in Bitcoin Collateralized Lending Facilities _ Investing.com

- Case Study of Bitcoin Collateral for Real Estate Purchase _ Korea Economic Daily

- Structure of Bitcoin Collateralized Loans _ Digital Today

- Definition of Auto Loan _ NICE Information Service

- Securitization of Automobile Installment Financing Receivables _ Law Firm (LLC) Taepyeong

- Case of Asset-Backed Securities (ABS) Issuance for Automobile Installment Financing _ Mae Il Business Newspaper

- Auto Loan Securitization Structure _ Korea Ratings

- Definition of Asset-Backed Securities (ABS) _ Wikipedia

- Types of Asset-Backed Securities (ABS) _ Korea Investment & Securities

- Credit Enhancement of Asset-Backed Securities _ Korea Investor Protection Foundation

- Eligible Collateral for Fed Repo Operations _ Federal Reserve Bank of New York

- Tri-Party Repo and Non-Government Securities Collateral _ ICMA

- US Debt Limit Negotiations and Market Uncertainty _ Investing.com

- Debt Limit Negotiations and Bitcoin Price Volatility _ Sisa Journal e

- Sino-Korean Debt Limit Negotiations and Bitcoin Emerging as a Hedge _ Choice Economy

- Former President Trump’s Proposal for Bitcoin Utilization _ Industry News

- Scenario for US Strategic Asset Stockpiling of Bitcoin _ YouTube Channel (Intellectual Explanation)

- Possibility of Bitcoin Price Rally as Debt Limit is Raised _ News1

- Relationship Between US Government Function and Bitcoin Demand _ ATFX

- Bitcoin as a Strategic Asset for BRICS Countermeasures _ Investing.com