Introduction: An Unstable Foundation for Global Finance

August 15, 1971. Do you know what happened on this day? U.S. President Richard Nixon made a shocking declaration… he simply severed the last link between the US dollar and gold.¹ Known as the ‘Nixon Shock,’ this measure, while a response to necessity, didn’t actually solve the fundamental problems of global finance. Frankly, it was just a ‘postponement.’ This marked the beginning of an era of fiat currency hegemony built on a profoundly structural paradox for the world. This event is the starting point for our journey to explore how unstable the foundation of a global system relying on a single national currency truly is.

The core concept we will delve into throughout this article is ’neutral money.’ Hmm… does that sound a bit complicated? Simply put, it refers to a global asset that is free from the political logic or economic influence of any specific nation. After the collapse of the gold standard, this became a kind of ‘holy grail’ that the international financial community only dared to whisper about. As we will continue to explore, our current dependence on the US dollar, which we take for granted, is, in retrospect, a precarious and risky situation, almost an ’exception.’

Therefore, in this article, we will follow two parallel paths. One is the history of attempts to create institutional solutions like the Bretton Woods system or Special Drawing Rights (SDRs) that ultimately failed. The other is the history of innovations that spontaneously emerged from the market, such as the Eurodollar market and the current Bitcoin and stablecoin ecosystems.

Ah, to give you a slight hint of the conclusion beforehand, these digital assets didn’t just appear out of thin air. In my view, they are the technological culmination of decades-long pursuit for a truly global, apolitical financial architecture.

Part 1: The Hegemon’s Paradox: Why the Dollar-Centric World Sputtered from the Start

In this chapter, we will dissect the inherent flaws hidden within the 20th-century monetary system. A centrally planned design orchestrated by a nation? Frankly, it was destined for failure from the outset.

1.1. The Genesis of All Problems: Triffin’s Prophecy and the Dollar’s Dilemma

The Bretton Woods System in 1944.¹ The structure was simple: the US dollar was pegged to gold, and all other currencies were pegged to the dollar. But here’s the thing. In 1960, an economist named Robert Triffin made a truly ominous prophecy. This is the famous ‘Triffin Dilemma.’

This dilemma is truly mind-boggling. It traps the issuer of the reserve currency (obviously the US) in an impossible choice.

- To protect the dollar’s value (and global trust)? It must tighten its money supply. But what happens then? The liquidity needed for the global economy to trade and grow dries up.

- Conversely, to pump plenty of money into the global economy? It must continue to run current account deficits and print dollars. But what’s the result? Dollars flood the market, eroding trust and eventually debasing its value.

It’s a lose-lose situation. A perfect dilemma, indeed.

Case Study: The Collapse of the 1960s and the Nixon Shock

And this prophecy… oh, it was chillingly accurate in history. As the U.S. printed money indiscriminately for the Vietnam War and the ‘Great Society’ programs, the amount of dollars circulating abroad began to far exceed its gold reserves.² Then, countries like France, led by President Charles de Gaulle, started demanding, “Give us gold for our dollars, as promised!” exposing the system’s insolvency.

The culmination of this pressure was the Nixon Shock in 1971. This unilateral decision to suspend convertibility to gold effectively reneged on the core promise of the Bretton Woods Agreement. This moment is forever remembered by the infamous words of then-Treasury Secretary John Connally to the European side:

“The dollar is our currency, but it’s your problem.”

Wow, truly remarkable, isn’t it? It was a blatant admission of the system’s coercive nature.

Table 1: US Gold Reserves vs. Foreign Held Dollars (1960-1971)

| Year | US Gold Reserves (Billions USD) | Foreign Held US Dollar Liabilities (Billions USD) | Deficit (Foreign Dollars - Gold Reserves) |

|---|---|---|---|

| 1960 | 17.8 | 18.7 | 0.9 |

| 1965 | 13.8 | 27.9 | 14.1 |

| 1970 | 11.1 | 43.3 | 32.2 |

| 1971 (Aug) | 10.2 | 50.0+ | 39.8+ |

Note: Data is reconstructed from various historical sources and clearly shows the exponential widening of the gap in the 1960s.

Looking at the U.S. current account balance data (Source: U.S. Bureau of Economic Analysis, FRED), we can visually confirm that after the Nixon Shock, the U.S. continuously recorded massive current account deficits to supply dollar liquidity to the world.

People often think the Triffin Dilemma ended with the historical event of 1971. Not at all. The data tells us it simply changed its form. The world still needs dollars for trade and reserves. And to supply these dollars, the U.S. must run deficits. It exports dollars in exchange for real goods and services. This is the reality of the ’exorbitant privilege’ that de Gaulle spoke of, allowing the U.S. to finance its domestic consumption and government spending with cheaply printed money. So, the dilemma hasn’t disappeared; it has become the very core engine of modern U.S. economic policy.

1.2. The Committee-Created Artificial Currency: The Glorious Birth and… Humble Reality of SDRs

Seeing these cracks in the dollar hegemony system, the International Monetary Fund (IMF) couldn’t stand idly by. In 1969, they created the Special Drawing Rights (SDR). A potential future neutral reserve asset to complement dollars and gold! They harbored a grand dream of it being a kind of ‘paper gold.’

But reality was different.

Folks, the SDR is not a ‘currency’ in the true sense. It’s merely a ‘claim on’ a basket of major currencies, an ‘accounting unit’ used only between the IMF and member central banks. I or you cannot use it to settle trade or make investments.

Why did SDRs fail to replace the dollar? There are several decisive reasons:

- Inflexible Supply: Its supply is controlled by political consensus within the IMF, not by market demand.

- Derived Value: The value of SDRs ultimately comes from the national currencies they are meant to complement – dollars, euros, yen, etc. Therefore, they can only be a follower, never a leader.

- Lack of Ecosystem: There is virtually no global market for bonds denominated in SDRs, nor for trade settlements or loans.

Table 2: Changes in the IMF SDR Basket Currency Composition Ratio

| Period | USD | DEM/EUR | JPY | GBP | CNY |

|---|---|---|---|---|---|

| 1981–1985 | 42% | 19% (DEM) | 13% | 13% | - |

| 2001–2005 | 45% | 29% (EUR) | 15% | 11% | - |

| 2016–2022 | 41.73% | 30.93% (EUR) | 8.33% | 8.09% | 10.92% |

| 2022–Present | 43.38% | 29.31% (EUR) | 7.59% | 7.44% | 12.28% |

Source: IMF.¹⁸

Look at this SDR basket composition. Is it purely determined by economic indicators? Absolutely not. It’s the product of fierce geopolitical negotiations. The inclusion of the Chinese Yuan (CNY) in 2016¹⁶ was less about the Yuan’s free usability at the time and more of a ‘political gesture’ to symbolically acknowledge China’s rising economic power.

Therefore, SDRs don’t transcend the power dynamics of national currencies; they actually formalize them. It’s closer to a political tool disguised as a neutral economic instrument.

The lesson from the failure of SDRs is truly, truly painful. Can a committee of nations with conflicting agendas create a ’truly neutral asset’ that can challenge the power of the most powerful member (the U.S.)? Well… it was impossible from the start.

Part 2: Borderless Order: The Rise of Deterritorialized Money

So, while the institutional players were fumbling, was the market idle? Not at all. The market ingeniously found solutions to these rigidities and regulations. I’m talking about massive, stateless currency systems that operate beyond the direct control of any single government.

2.1. Accidental Revolution: The Eurodollar Market

US dollars deposited in banks outside the United States. This is what we call Eurodollars. This market wasn’t intentionally created with a “Let’s build it!” mentality. It was an organic phenomenon born from a unique environment of geopolitics and regulation. From my experience, great innovations often start with ‘accident.’

Its origins trace back to the Cold War era. At that time, the Soviet Union and other Eastern Bloc countries feared that the U.S. would freeze their dollar deposits held in U.S. banks.²³ So, they transferred these dollars to European banks.

However, what brought explosive growth to this nascent market… or rather, what poured fuel on the fire was the U.S.’s troublesome domestic banking regulation known as ‘Regulation Q.’ This was a law that put a cap on the interest rates U.S. banks could offer on deposits. As U.S. inflation rose, these meager interest rates, bound by the cap, lost their appeal. Meanwhile, European banks, not subject to Regulation Q, could offer much higher interest rates on dollar deposits.

Where would you put your money? Naturally, there was a massive incentive for corporate and individual dollars to move offshore.

This ‘regulatory arbitrage’ is the key. Thanks to this, a deep, liquid, and efficient international dollar market emerged, operating outside the direct oversight of the U.S. Federal Reserve.

The Eurodollar market was effectively a ‘permissionless’ global liquidity pool for the U.S. dollar. Because this market was less regulated (no reserve requirements, no interest rate caps), it could operate with greater efficiency and yields than the U.S. domestic market.²⁴ It became a major engine of international finance, driving financial innovation and credit creation worldwide.

Does this sound familiar? A more efficient, global, and less regulated version of the existing financial system. Yes, that’s right. This is the precise conceptual blueprint and original model for what is now called ‘Decentralized Finance (DeFi).’

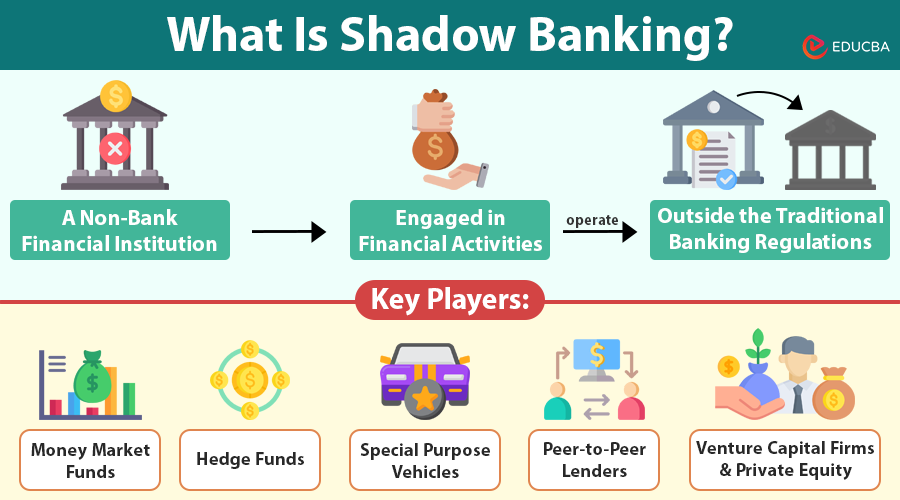

2.2. Finance in the Shadows: The Engine of Unseen Global Liquidity

The ‘Shadow Banking’ system is the modern successor that carries forward the spirit of the Eurodollar market, operating outside traditional regulatory boundaries. While the name might sound a bit ominous, it refers to a network of financial intermediaries – such as money market funds (MMFs), hedge funds, and special purpose vehicles (SPVs) – that perform bank-like functions such as credit creation and maturity transformation without being subject to traditional banking regulations.

Case Study: The 2008 Global Financial Crisis

Ah, 2008. It was truly terrible. We often think of the 2008 crisis as solely a failure of the traditional banking system, but no, to be precise, it was a crisis that originated and amplified within the shadow banking system. Institutions like Lehman Brothers relied heavily on short-term funding from this system (e.g., the repo market). When trust evaporated, this funding dried up, triggering catastrophic chain defaults.

This event starkly demonstrated the immense power of this ‘parallel financial system’ and, at the same time, its inherent vulnerabilities when the lender-of-last-resort function of central banks or deposit insurance mechanisms are absent.

Whether it’s the Eurodollar market or the shadow banking system, the essence is the same. They arose to circumvent costly and inefficient regulations. This dynamic is cyclical and unstoppable. The pursuit of a ’neutral,’ efficient, and unregulated financial space. This is a fundamental market force. And it perfectly sets the stage for the emergence of technological solutions that achieve this not by finding loopholes in existing laws, but by accomplishing it through design itself.

Part 3: Neutrality by Design: The Technological Ascent of Digital Assets

So, we’ve finally arrived here. In this chapter, I will argue that Bitcoin and stablecoins are the logical and technological outcomes of the historical trends identified in Part 1 (institutional failures) and Part 2 (organic market innovation). They represent a deliberate attempt to engineer the attributes of ‘neutral money’ that the market has always sought.

3.1. Bitcoin: A Trust Protocol in a Trustless World

To view Bitcoin merely as a speculative asset is to miss its essence. It must be analyzed as a technological innovation that solved the notoriously difficult ‘Byzantine Generals’ Problem’ in computer science: a system capable of achieving consensus and transferring value across a network without a central authority or trusted third party. ³⁶

Absolute scarcity (a fixed supply of 21 million), censorship resistance (no single entity can block transactions), and decentralized settlement. These core attributes make Bitcoin a unique candidate for a neutral global monetary asset.⁴

Bitcoin as a Geopolitical Asset

Beyond the analogy of ‘digital gold,’ Bitcoin is positioning itself as a strategic geopolitical asset for individuals and nations seeking to escape from hegemonic currency systems.

- Case Study 1: Russia-Ukraine Conflict This conflict became the ‘first cryptocurrency war.’ Ukraine successfully raised tens of millions of dollars in donations by bypassing slow and potentially blockable traditional banking channels through direct crypto donations. Simultaneously, concerns arose that Russia might use cryptocurrencies to evade international sanctions. This dual use case demonstrates the powerful strength of Bitcoin’s core essence as a neutral technology, independent of user intent.

- Case Study 2: The El Salvador Experiment In 2021, El Salvador became the first country to adopt Bitcoin as legal tender. This ongoing experiment has seen successes such as attracting tourism and technology investment, and providing some citizens with their first access to financial services. However, challenges such as low public understanding of technology, volatility in everyday transactions, and an overall low adoption rate are also significant. Regardless of its ultimate outcome, this experiment is a historic attempt by a sovereign nation to build a parallel financial system on a neutral, open-source protocol.

The international financial system requires a final settlement asset free from counterparty risk, a ‘base money.’ Simply put, an asset that is settled in and of itself, no questions asked. Bitcoin, with its finality of settlement and absence of a central issuer, is the first digital asset with these ‘base money’ characteristics.

3.2. Digital Eurodollars: The Proliferation and Power of Stablecoins

If Bitcoin is the new neutral ‘reserve asset,’ then stablecoins are the new ’transaction layer.’ Stablecoins are digital tokens that aim to maintain a stable value relative to fiat currencies, particularly the U.S. dollar.

This is a truly ingenious concept, combining the advantages of digital assets (speed, global reach, programmability) with the price stability of fiat currencies.

The main types of stablecoins can be categorized as follows:

- Fiat-Collateralized (e.g., USDT, USDC): This is the dominant model in the market. The issuer holds actual dollars or dollar-equivalent assets in bank accounts and issues tokens.

- Crypto-Collateralized (e.g., DAI): Issued with over-collateralization of other crypto assets held in smart contracts. More decentralized, but carries the risk of volatility of the underlying collateral.

- Algorithmic (e.g., the former UST): …This attempted to regulate supply through algorithms without real collateral.

Data (Sources: The Block, DefiLlama) shows a surge in the total supply of stablecoins, with fiat-collateralized USDT and USDC overwhelmingly dominating the market.

Case Study: The Terra/Luna Collapse - A Lesson in Monetary Physics

In May 2022, the dramatic collapse of the algorithmic stablecoin TerraUSD (UST) and its sister token Luna (LUNA) was a truly unforgettable turning point. As UST lost its $1 peg under market pressure ('de-pegging'), the algorithm designed to stabilize it fell into a 'death spiral.' In the process, over $40 billion in value simply evaporated within days.

The Terra/Luna experiment was an attempt to create a stable currency ex nihilo (out of nothing). Its collapse… cruelly proved once again… the fundamental law of monetary history: ‘currency without sound collateral is inherently fragile and exposed to bank runs.’

The subsequent ‘flight to quality’ in the crypto market naturally solidified the market share of fully collateralized stablecoins like USDC and USDT.

3.3. A New Balance of Power: The Future of Hybrid Finance

The world is now shifting from a unipolar dollar hegemony system to a multipolar hybrid model. In this new model, sovereign currencies will coexist with, or more accurately, fiercely compete with, stateless digital assets.

The future financial architecture I envision could consist of this two-layer system:

- Layer 1 (Reserve and Settlement): Bitcoin serves as a neutral global reserve asset, a sort of ‘digital gold standard 2.0.’ Nations and large institutions will hold Bitcoin as a hedge against fiat currency devaluation and geopolitical risk.

- Layer 2 (Transaction and Credit): Stablecoins (primarily dollar-pegged) will function as the primary medium of exchange for global trade, remittances, and that hotbed of decentralized finance (DeFi).

This new balance will fundamentally redefine financial power. It will reduce the ’exorbitant privilege’ of the U.S. and introduce a new form of monetary discipline through the fixed supply of a reserve asset (Bitcoin). And it will empower individuals and small nations with direct access to a global, censorship-resistant financial system.

Conclusion: The End of Hegemony, the Dawn of a Hybrid System

Shall we summarize this lengthy article? My conclusion is that the 20th-century model, where a single nation’s currency (the dollar) served as the foundation of global finance, was, frankly, a highly unstable historical anomaly. Institutional solutions consistently failed, and organic market order continuously innovated and found its way. And finally, the path for a technological paradigm shift has opened.

The future of money will not be a singular form where one system completely replaces another. It will be a competitive, complex, and hybrid ecosystem.

The journey to find ‘neutral money,’ which began with the collapse of the Bretton Woods system… that journey is now leading us to a system that places trust not in institutions or governments, but in mathematics, cryptography, and open-source code visible to all.

This transition will, of course, be volatile and contentious. It will be noisy and chaotic.

But, but you see. This fundamental demand for a more neutral, more efficient, and more open global financial system… this is a tremendous force that truly cannot be stopped. The very principles that drove the creation of the Eurodollar market have now found their ultimate expression in the architecture of digital assets, heralding what is truly… the most significant evolution in the nature of money over the past century.

References

- What is the ‘Triffin Dilemma’ plaguing the U.S.? | [Hangaram News Plus]

- Nixon Shock | [Namuwiki]

- The Foundation for Entering the World’s Top 5 Economic Powers | [KDI School of Public Policy and Management Economic Education & Information Center]

- There is no future without Bitcoin | [Taemin Oh, Hye-min Sohn, Yu-jeong Kim]

- The Fall of the Bretton Woods System… Exploring Future Currencies Amidst the Humiliation of the Dollar | [JoongAng Sunday]

- Nixon Shock | [Wikipedia]

- Triffin Dilemma | The Structural Contradiction of the Reserve Currency Dollar | [TREND.M]

- Triffin Dilemma | [Namuwiki]

- [US High-Intensity Tightening] Barrons “Fed Rate Hikes… Focus on Side Effects of Dollar Strength” | [Yonhap Infomax]

- U.S. Current-Account Balance | [Bureau of Economic Analysis]

- U.S. Current-Account Balance (Quarterly) | [Bureau of Economic Analysis]

- Current Account Balance: Total Trade of Goods for the United States (DISCONTINUED) (BPBLTD01USA636S) | [FRED]

- Current Account Balance: Total Trade of Goods for the United States (DISCONTINUED) (BPBLTD01USA636N) | [FRED]

- Balance on current account (IEABC) | [FRED]

- Balance on Current Account, NIPA’s/Gross Domestic Product | [FRED]

- Special Drawing Rights (SDR) | [Danbi News]

- Special Drawing Rights | [Wikipedia]

- What are Special Drawing Rights (SDRs)? - Meaning & Definition | [KB’s Thoughts]

- [Jibung’s Glossary] Special Drawing Rights (SDR) / Google Tax / Pitch Market / Zombie Company | [Maeil Business Newspaper]

- SDR (Special Drawing Rights) | [Glossary of Current Economic Terms (Ministry of Economy and Finance)]

- IMF, SDR Yuan Weighting Raised from 10.92% to 12.28% | [Korea Economic Daily]

- Hankyoreh Ilbo Economic Terminology (Special Drawing Rights) | [Bank of Korea]

- Eurodollar | [Glossary of Current Economic Terms (Ministry of Economy and Finance)]

- Eurodollar | [Wikipedia]

- THE EURO-DOLLAR MARKET: AN INTERPRETATION | [International Economics Section (Princeton)]

- The Effects of Removing Regulation Q— A Theoretical Analysis | [Federal Reserve Bank of Kansas City]

- The Euro-Dollar Market: Some First Principles | [Chicago Booth]

- Near-money premiums, monetary policy, and the integration of money markets | [Bank for International Settlements (BIS)]

- The Driving Force of Dollar Hegemony, ‘Eurodollar’ | [Hankook Ilbo]

- Shadow Banking | [Namuwiki]

- Shadow Banking – Meaning, Functions, Advantages, and Disadvantages | [Management Study Guide]

- Shadow Banking System | [Wikipedia]

- Shadow Banking | [Hankyung Glossary]

- International Discussions on Shadow Banking and the Domestic Situation | [Insurance Research Institute]

- The Economic Role of Shadow Banking | [Korea Capital Market Institute]

- Terra (UST) Collapse and Lessons Learned: Mainnet and Bridge Security | [Decipher Media (Medium)]

- The End of the US Dollar Hegemony: This Is What Will Happen to Bitcoin (by Taemin Oh / Part 3) | [YouTube]

- The First Crypto War? Russia’s Invasion of Ukraine Over One Year Later | [TRM Labs]

- The Role of ‘Cryptocurrencies’ in the War | [JoongAng Sunday]

- The Power of Coins Proven by War… Attempting Transformation into Gold | [Chosun Ilbo]

- War Broke Out… Why Didn’t Bitcoin Fall? | Author Taemin Oh [Taemin Oh’s Crypto Insight Episode 5] | [YouTube]

- Bitcoin Stable Amid Geopolitical Crisis… BTC Trends Through Past War Cases | [Digital Today]

- El Salvador President Evaluates Bitcoin Experiment as Great Success, but What Are the Challenges? | [Global Economics]

- El Salvador, 4 Years After Adopting Bitcoin as Legal Tender… Controversy Remains | [Digital Today]

- El Salvador’s Bitcoin Experiment: Success or Failure… | [Digital Today]

- El Salvador’s Bitcoin Experiment Ultimately Fails… | [Global Economics]

- What is the Result of El Salvador’s Bitcoin Legal Tender Experiment? | Min-ju Choi’s ‘Coin Focus’ | [YouTube]

- USDT Vs. USDC Vs. DAI: The Best Stablecoins of 2025 | [Cryptomus]

- Dollar Stablecoins Shake Up Global Financial Markets | [KPMG International]

- What is the Relationship Between Stablecoins and Ethereum? | [Naver Premium]

- What is the Difference Between These Two? (USDT vs USDC) | [Cryptomus]

- How Do Stablecoins Make Money? | [Xangle]

- Stablecoin Market Exceeds $294.7 Billion… USDT Market Share 59% | [Digital Today]

- Total Stablecoin Supply | [The Block]

- Growth of the Stablecoin Market and Korea’s Response Measures | [Four Pillars]

- Stablecoins and Trust in Central Banks | [Deloitte]

- The Block: Bitcoin, Ethereum & Crypto News | [The Block]

- The Great LUNA Collapse of 2022 | [Namuwiki]

- Why Did Luna and UST Crash… A Complete Timeline of the ‘Terra Incident’ | [Hankyoreh]

- [Blockchain Column] Lessons from the Terra (UST) / Luna (LUNA) Incident <Part 1> | [Electronic Times]

- Why Did the Unprecedented ‘Coin Collapse’ Occur… Terra Incident A to Z [Geeks] | [Korea Economic Daily]