Hello! Today, I want to share an in-depth discussion about a fascinating and crucial topic: the ‘semiconductor super cycle.’

Here in 2025, we are witnessing the global semiconductor industry pass through the peak of a historic boom, the so-called ‘super cycle.’ However, the truly important point here is that this colossal wave we’re facing is fundamentally different from those we’ve experienced in the past.

Let’s look back. The early 2000s were driven by laptop demand, the early 2010s by the proliferation of mobile devices, and the mid-to-late 2010s by smartphone replacement cycles or the cryptocurrency mining boom. These cycles were inherently based on ‘consumer-driven (B2C)’ demand from PCs and mobile devices.

In contrast, the 2025 cycle is powered by entirely different engines. The widespread adoption of generative AI like ChatGPT, the advancement of autonomous driving technology, and the full-scale emergence of the robotics industry are the key drivers. Consequently, explosive ‘infrastructure-driven (B2B)’ investment by corporations (B2B) and cloud service providers (CSPs) to build AI data centers has become the core momentum. Simply put, the demand to build ‘digital power plants’ to run the massive ‘brain’ of AI is leading the market.

Another intriguing characteristic of this super cycle is the simultaneous, and powerfully interdependent, explosion of AI accelerators (GPUs) and High Bandwidth Memory (HBM). This also marks a historic beginning where the two giant pillars of the semiconductor industry, system semiconductors (foundry manufacturing) and memory semiconductors, are converging into a single ecosystem.

This transformation is fundamentally altering the economic model of the semiconductor industry. While past B2C cycles were driven by the ‘volume’ of ‘general-purpose’ products like DDR and LPDDR and were sensitive to price fluctuations, the current B2B cycle is defined by the ‘value’ and ‘performance’ of ‘specialized’ products like HBM.

Why is this? The success of AI services depends on GPU performance, and that GPU performance depends on the data transfer speed (bandwidth) of HBM. Leading companies in the AI market exhibit ‘inelastic’ demand, meaning they are relatively less sensitive to price when seeking the best services. The sky-high Average Selling Price (ASP) of HBM has clearly demonstrated its impact in the record-breaking Q3 2025 earnings of SK Hynix and Samsung Electronics. This strongly suggests that the semiconductor industry is shifting its focus from ’economies of scale’ to ’economies of technology.’

Now, let’s explore this massive wave of change together. We will revisit the history of past ‘chicken games,’ analyze the structural changes in the current memory market sparked by AI, and diagnose the foundry hegemony war, another key axis of the market. Finally, based on all this analysis, we will predict future risks and opportunities.

1. Echoes of the Past: The History of Chicken Games and Lessons for Winners

If I had to summarize the history of the semiconductor industry in one phrase, I would say ‘periodicity’ and ‘survival competition.’ Amidst the cycle of extreme booms (Super Cycles) and harsh downturns (Winters), ruthless survival battles, or ‘Chicken Games,’ have unfolded.

1.1. The 1980s: US-Japan Semiconductor Friction and the Creation of ‘Opportunity’

As you know, a ‘chicken game’ is a game theory concept where two competitors charge at each other, engaging in a battle of attrition until one swerves and concedes. The DRAM market of the 1980s was the first grand experimental ground for this game theory.

At that time, the DRAM market was a ‘geopolitical chicken game’ between the inventor, the US, and the emerging dominator, Japan. In the late 1980s, as Japanese companies like NEC and Hitachi, through aggressive investment, captured over 90% of the DRAM market, the US, sensing a crisis, began strong trade pressure to protect its domestic industry.

As a result, the ‘US-Japan Semiconductor Agreement’ was signed twice, in 1986 and 1991. The core of this agreement was shocking: it mandated an increase in the market share of US-made semiconductors within Japan from the then 10% to 20%, and it forcibly stopped Japanese companies from dumping DRAMs through exports.

This agreement became a decisive factor in the decline of the Japanese semiconductor industry. The US sought to curb the monopoly of a specific country (Japan) in memory, and the artificial price controls and stifled investment gradually eroded the competitiveness of Japanese companies.

Ironically, the biggest beneficiary of the ‘supply gap’ created by this massive geopolitical conflict was Korea’s Samsung Electronics. In 1987, despite being in a desperate crisis with cumulative semiconductor business losses of 200 billion won, Samsung Electronics made an incredible contrarian investment by commencing construction of the ‘Line 3 factory’ in anticipation of the PC market boom the following year. While Japanese companies hesitated to invest due to US regulations, Samsung accurately captured this ‘god of opportunity (Kairos).’ Ultimately, it monopolized the benefits of the DRAM shortage and emerged brilliantly as a leading player in the market.

1.2. The 2000s: The DRAM ‘Chicken Game’ and Market Realignment

If the 1980s was a ‘geopolitical game,’ the 2000s were a ‘capital game.’ In the late 2000s, the DRAM market again suffered from severe oversupply. Particularly in 2007, the reckless expansion competition led by Taiwanese DRAM firms triggered a life-or-death ‘chicken game’ where products were sold below cost.

The outcome of this brutal price war was predetermined: the domino collapse of companies unable to bear the losses.

- The Fall of the Losers: Germany’s Qimonda, the world’s 5th-largest DRAM manufacturer, filed for bankruptcy in January 2009, unable to withstand the price crash due to oversupply and the recession. Elpida, the last hope of Japan born from the integration of NEC’s and Hitachi’s DRAM businesses, also went bankrupt after accumulating massive losses in the second chicken game of the 2010s. These companies critically lacked ‘cost competitiveness,’ ‘abundant financial resources,’ and the ‘strong will’ to endure crises.

- The Winner, Samsung Electronics’ ‘Super Gap’ Strategy: The ultimate winner of this chicken game was undoubtedly Samsung Electronics. Samsung’s winning formula was ‘counter-cyclical investment.’ This was evident again during the memory price drop in 2022. While competitors like SK Hynix and Micron all announced production cuts and investment reductions to survive, Samsung Electronics alone declared, “There will be no artificial production cuts,” and pursued a ‘super gap’ strategy by maintaining or increasing investment to widen the technology gap and lower costs.

This strategy accelerated the bankruptcy of competitors and led to the establishment of the current DRAM industry structure, where the ‘Big 3’—Samsung Electronics, SK Hynix, and Micron—monopolize the market after enduring immense losses.

The history of the past serves as a crucial compass for understanding the present in 2025. The 1980s were a ‘geopolitical game’ (US vs. Japan), and Samsung was the ‘beneficiary.’ The 2000s were a ‘capital game’ (Samsung vs. everyone), and Samsung was the ’leader.’

And in 2025, we stand on a far more complex battlefield where both games are unfolding simultaneously. A fierce ‘capital/technology game’ is playing out in the HBM market, while a ‘geopolitical game’ involving the US government is re-emerging in the foundry market.

2. The Present Storm: The 2025 Memory Revolution Sparked by AI

While past cycles were about creating a winner-take-all structure through ‘chicken games,’ the 2025 cycle is a process of ‘paradigm shift’ where the colossal wave of AI is fundamentally transforming the industry’s structure.

2.1. HBM: Memory as the New ‘Oil’ and the ‘Tilting Effect’

The heart of the AI revolution lies in building AI data centers and AI servers, which naturally leads to an explosive demand for high-performance AI accelerators (GPUs). However, for GPUs to perform at their best, they need a partner capable of processing vast amounts of data at immense speeds. That partner is High Bandwidth Memory (HBM). Consequently, HBM demand is soaring structurally.

This HBM is creating a very interesting phenomenon in the overall DRAM market called the ‘Tilting Effect.’ What this means is that because HBM offers overwhelmingly higher profitability compared to general DRAM, memory companies like Samsung Electronics and SK Hynix are concentrating all their limited production capacity (CAPA) and core personnel on HBM production.

This resource tilt has created a chain reaction of effects:

First, as resources are concentrated on HBM production, the output of general DRAMs like DDR5 for PCs and mobile devices has relatively decreased. As a result, the price of DDR5 16Gb, a mainstream DRAM product, surged by 42.6% in just one month by October 2025, leading to a phenomenon where not only HBM but also general DRAM prices are rising together.

Second, as memory companies rapidly transition to advanced processes requiring higher technological capabilities, the supply constraints for ’legacy (older)’ products like DDR4 and LPDDR4X have been further exacerbated. This has resulted in an unusual situation, rarely seen before, where prices for these older products are sharply increasing in the second half of 2025.

2.2. 2025 Market Status: Record Earnings for Winners and Divergent Statuses

The AI super cycle has brought unprecedented prosperity to all three memory companies. The Q3 2025 earnings vividly illustrate this situation.

- SK Hynix: Reached the ‘peak of the super cycle,’ achieving a phenomenal quarterly operating profit of 11.3834 trillion won in Q3 2025, the first in its history.

- Samsung Electronics: Achieved its highest-ever quarterly memory revenue with increased sales of HBM3E and server SSDs, recording an operating profit of 7 trillion won in its DS division, marking a complete turnaround.

- Micron: Raised its Q4 2025 (fiscal year basis) financial outlook thanks to improved DRAM prices and strong market demand.

However, behind this tremendous boom lies the divergent status of the two Korean companies vying for HBM leadership. In Q3 2025, SK Hynix’s operating profit (11.3 trillion won) overwhelmingly surpassed that of Samsung Electronics’ DS division (7 trillion won), marking a historic event where the established ‘ranking’ of the semiconductor market over the past two decades has been overturned.

This ‘profitability reversal’ phenomenon suggests that the game rules of the AI cycle have completely changed from the past. Samsung’s past winning formula was ’economies of scale’ and ‘cost competitiveness.’ However, the AI cycle is a game of ‘speed of technology’ and ‘strategic partnerships’ centered on ‘who supplies the highest-performance HBM to Nvidia first.’

- SK Hynix: As the ‘First Mover’ in the HBM market, it led the market by virtually monopolizing the supply of HBM3/3E to Nvidia and secured the top position in the DRAM market in Q3 2025.

- Samsung Electronics: Due to delays in Nvidia’s quality testing (qual test) for HBM3E, Samsung Electronics was a step behind in responding to the HBM market, failing to become the ‘first mover’ despite being the ‘King of Volume.’

Therefore, Samsung Electronics is making all-out efforts, engaging in “close discussions” with Nvidia to preempt the next-generation HBM4 market beyond the HBM3E market. It has significantly expanded its HBM production plans for 2026 and has already secured demand from key clients. The counterattack in HBM4 is not just about regaining market share for Samsung; it is a critical mission to reclaim its lost ’technological leadership.’

2.3. Next-Generation Technology Competition: The Future of HBM4 and Packaging

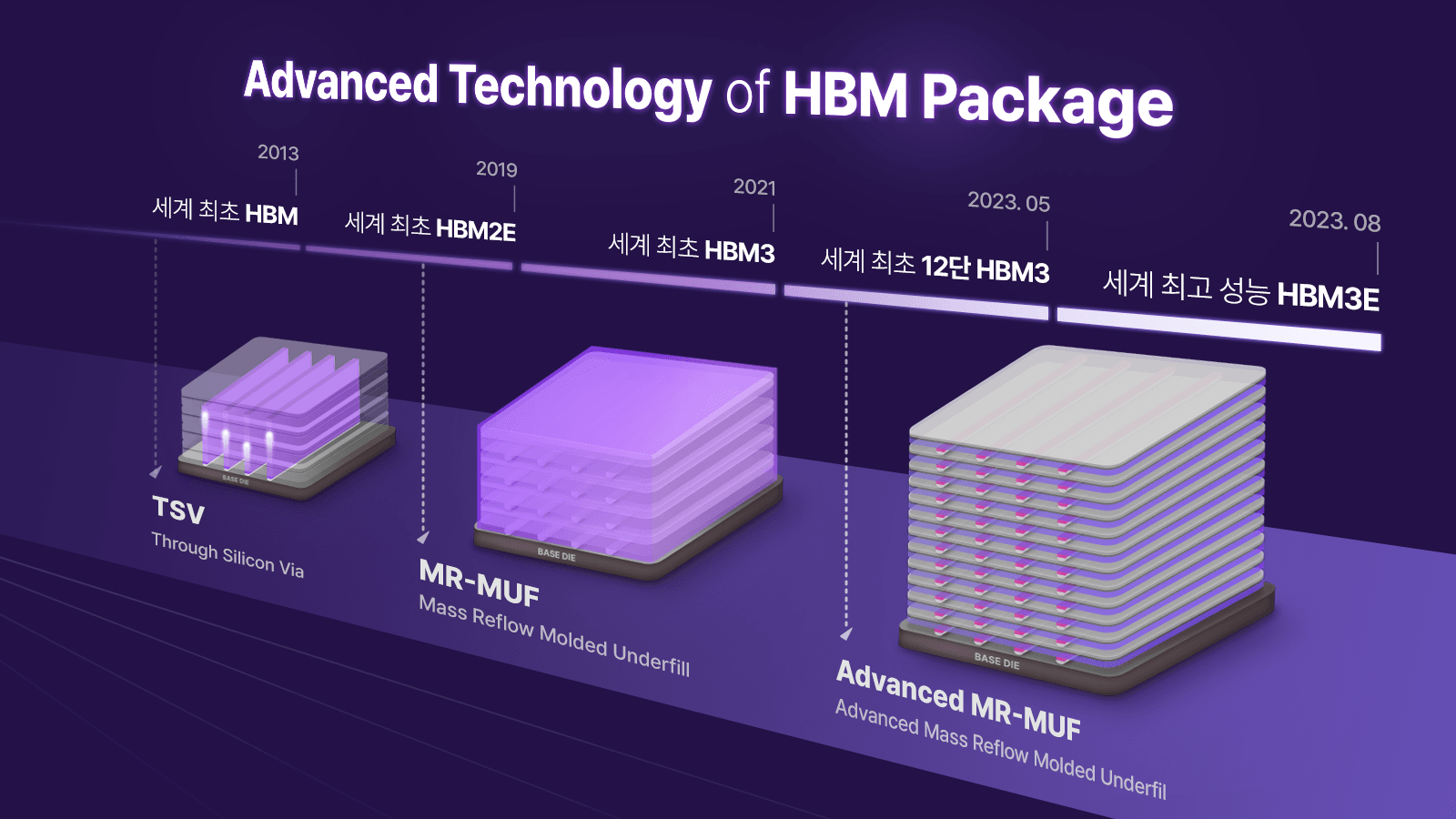

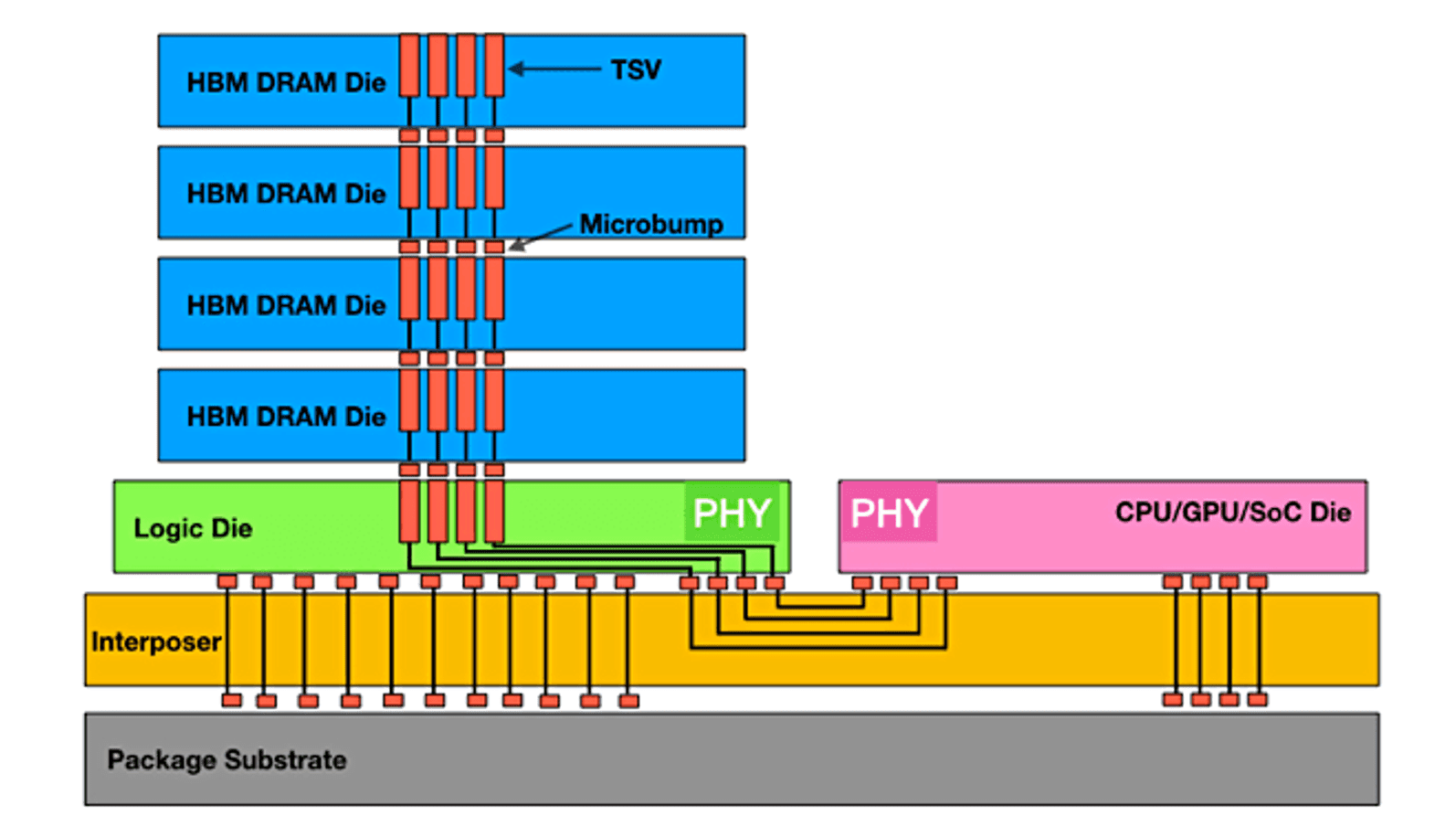

The core of the HBM competition lies in the ‘packaging’ technology, which vertically stacks DRAM chips like apartments.

For HBM3E and below, the technical approaches vary slightly by manufacturer:

- SK Hynix uses the ‘MR-MUF (Mass Re-flow Molded Underfill)’ method. This involves injecting a liquid protective material (EMC) between chips and curing it all at once. The process is relatively simple, advantageous for heat dissipation (about twice as effective as the competitor’s TC-NCF), and offers high yields, playing a crucial role in securing the HBM market lead.

- In contrast, Samsung Electronics and Micron use the ‘TC-NCF (Thermal Compression with Non-Conductive Film)’ method. This involves inserting a thin film-type material (NCF) each time chips are stacked, and the process is known to be more complex than MR-MUF.

Comparsion of Stacking Method

However, for future needs requiring higher stacking, such as HBM4 (16 layers) or HBM5 (20 layers), the existing ‘micro-bump’ method connecting chips will hit physical limitations. The ‘game-changer’ technology to overcome this limitation is ‘Hybrid Bonding.’

Hybrid bonding is a truly innovative technology. It completely eliminates the ‘bumps’ that connected chips and directly bonds the chips in the wafer state using copper (Cu) (Wafer-to-Wafer). This technology drastically reduces chip thickness, allowing for more chips to be stacked, increases data transfer speeds, and improves heat dissipation.

Another significant change brought by HBM4 is the importance of the ‘Base Die.’ In HBM4, the ‘Base Die’ (or logic die) located at the bottom layer of the memory chip stack will serve as the core ‘brain.’ This base die is not just a support but will include ‘customized’ logic circuits tailored to the requirements of AI customers (like Nvidia).

Here’s the crucial point: This logic die, acting as the ‘brain,’ requires advanced foundry processes of 5nm (nanometer) or below, not memory processes.

This means HBM4 represents a ‘Singularity’ where the two biggest pillars of the semiconductor industry, ‘memory’ and ‘foundry,’ converge into an inseparable product.

This **‘forced convergence’** is fundamentally reshaping the market landscape.

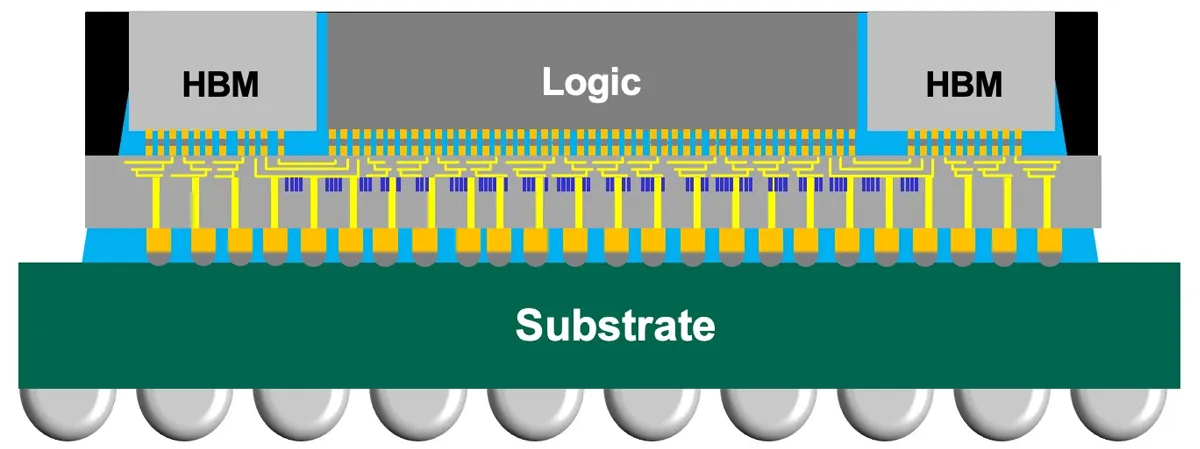

SK Hynix, possessing only memory processes, has formed an ‘alliance’ with foundry leader TSMC. TSMC plans to manufacture the base die using its advanced processes and then stack SK Hynix’s memory dies using hybrid bonding technology, effectively seizing control of HBM stacking (order management).

This presents both the ‘greatest crisis’ and the ‘greatest opportunity’ for Samsung Electronics. Samsung is the only company in the world that possesses both advanced memory and advanced foundry capabilities. If Samsung’s memory and foundry divisions can collaborate perfectly to offer a ‘One-Stop’ HBM4 solution, it holds immense potential to outperform the SK-TSMC alliance.

3. Another Battlefield: The Foundry Hegemony War

While the HBM revolution is driving ‘convergence’ in the memory market, a grand war for ‘hegemony’ is unfolding in the foundry (semiconductor contract manufacturing) market, the other major axis of the market.

3.1. The 2025 Foundry Landscape: TSMC’s Unbreachable Fortress and ‘Foundry 2.0’

The 2025 foundry market can be accurately described as TSMC’s ‘reign.’ As of Q2 2025, TSMC’s market share reached an all-time high of 70.2% to 71%. In contrast, second-place Samsung Electronics’ share declined to the 7.3% to 8% range, widening the gap between the two companies to a staggering 63 percentage points.

The reason for TSMC’s dominance is clear: it monopolistically manufactures most of the current AI chips, including Nvidia’s ‘Blackwell’ GPU and Apple’s M-series. Its advanced process revenues (3nm, 5nm) exceeded 60% of its total, acting like a black hole for AI demand.

TSMC’s true strength, its ‘moat,’ isn’t just about having a few nanometer (nm) processes. It lies in its ecosystem for ‘Advanced Packaging’ (e.g., CoWoS), which combines GPUs and HBM. AI chips are not single chips but complex ‘systems’ integrating HBM, logic dies, and more. For customers (like Nvidia and Apple), going to TSMC means their ‘chip manufacturing + packaging’ needs can be met all at once, making it incredibly convenient.

The ‘Foundry 2.0’ concept presented by market research firm Counterpoint Research clearly illustrates this situation. Under this new standard, which includes the entire semiconductor ecosystem—not just chip manufacturing (Foundry 1.0) but also IDMs (Integrated Device Manufacturers like Intel and Samsung), OSATs (Outsourced Semiconductor Assembly and Test companies), and mask makers—TSMC (38%) remains number one. However, Samsung (4%) drops to sixth place, trailing packaging companies (ASE) and other IDMs (TI). This signifies Samsung’s lag in this ‘integrated solution’ competition and aligns precisely with TSMC’s strategy to dominate the platform business in the upcoming HBM4 era.

| Rank | Company | Q2 2025 Market Share | Q2 2024 Market Share | Notes |

|---|---|---|---|---|

| 1 | TSMC (Taiwan) | 71% (or 70.2%) | 65% | All-time high due to exclusive AI chip demand |

| 2 | Samsung Electronics (South Korea) | 8% (or 7.3%) | 10% | Market share decline, 63%p gap with TSMC |

| 3 | SMIC (China) | 5% | 6% | Market share maintained with Chinese government subsidies |

| 4 | UMC (Taiwan) | 5% | 6% | - |

| 5 | GlobalFoundries (USA) | 4% | 5% | - |

Note: Based on data from Counterpoint Research and TrendForce

3.2. The 2nm (2nm) War: The Crucial Battleground for the Future

While the current gap is overwhelming, hegemony is not eternal. The next battleground will be decided in the 2nm (nanometer) process.

TSMC (The King): Announced plans for 2nm mass production in the second half of 2025, aiming to solidify its market leadership. It is reportedly already secured orders from major clients like Apple and Qualcomm. However, a severe security breach in August 2025 involving the leak of key 2nm technologies has increased risks.

Samsung Electronics (The Challenger): Introduced the next-generation GAA (Gate-All-Around) technology ahead of TSMC for 3nm, but unfortunately struggled with yield (defect-free product ratio) issues. It plans to start mass production of its 2nm (SF2) process in 2025, with goals to expand to HPC (High-Performance Computing) in 2026 and automotive semiconductors in 2027. Fortunately, it achieved its ‘highest quarterly order performance’ in Q3 2025, and securing orders for Tesla’s next-generation AI chips (AI5, AI6) from its Taylor fab in the US is a significant counterattack signal for Samsung Foundry.

Intel (The State-Backed Disruptor): Declared its re-entry into the foundry market in 2021 with an ambitious goal of becoming the ‘2nd largest market player by 2030.’ In October 2025, it surprised the industry by announcing the official mass production of the ‘world’s first 2nm-class (1.8A)’ semiconductor, faster than Samsung and TSMC. Intel is adopting its unique ‘RibbonFET’ technology, similar to Samsung’s GAA, along with its secret weapon, ‘PowerVia,’ a technology for supplying power from the back of the chip.

Intel’s revival is not merely a technological achievement. It is part of a ’national strategy,’ fueled by the US government’s ‘Make America Great Again (MAGA)’ political agenda and substantial subsidies and support under the ‘CHIPS Act.’

3.3. Geopolitics and Supply Chains: The US ‘Chip Alliance’ Strategy

Beneath the surface of the 2nm technology competition lies a cold ‘geopolitical’ rivalry between the US and China for AI technology hegemony. As of 2025, the global AI ecosystem is rapidly reorganizing into two major blocs centered around the US and China.

The US, through the ‘CHIPS Act,’ aims to attract semiconductor manufacturing domestically (On-shoring) and restructure supply chains. Samsung (Taylor fab), SK Hynix (Indiana fab), and TSMC (Arizona fab) have all responded to this subsidy policy by deciding to make massive investments worth tens of trillions of won in the US.

However, these investments are at risk of becoming a ‘Strategic Trap.’

First, the CHIPS Act subsidies include excessively stringent conditions, such as ‘sharing of excess profits.’

Second, in February 2025, the (hypothetical) Trump administration’s suggestion of a ‘comprehensive review’ of the Semiconductor Act and the possibility of imposing up to ‘100% tariffs’ placed Korean and Taiwanese companies, which have promised massive investments in the US, at risk of becoming political ‘hostages.’

The US has attracted investments from Samsung and TSMC under the guise of supply chain restructuring with ‘allies’ (Friend-Shoring), but at the same time, it is reviving its domestic company ‘Intel’ as a symbol of ‘MAGA politics’ by providing substantial subsidies. This ironically resembles the history of the 1980s when the US, through agreements, suppressed the semiconductor industry of its ally, Japan.

Ultimately, Korean and Taiwanese companies find themselves facing not only a pure ’technology’ competition but also a second front of unpredictable ‘geopolitical risk.’

4. Future Predictions: When and How Will the Next Cycle Arrive?

The current hot super cycle cannot last forever. Market predictions for the direction after 2026 are divided between optimism (Bull View) and pessimism (Bear View).

4.1. 2026 Outlook (Bull View): “An Era of Supply Shortage Led by HBM4”

Optimists, including Samsung Electronics, predict that memory market conditions will remain very strong in 2026. Samsung Electronics analyzed in its Q3 2025 earnings announcement that even considering its increased capital expenditure (CAPEX) and maximum production, “customer demand will exceed this level.”

The basis for this optimism is clear:

1. Full-scale HBM4 adoption: 2026 marks the full opening of the high-performance HBM4 market. HBM4 can command prices more than 30% higher than HBM3E, driving overall market growth.

2. Persistence of the ‘Tilting Effect’: With supply concentrated on HBM and high-capacity server DRAMs, the ‘supply shortage’ for mobile, PC memory, and legacy products (like DDR4) will intensify.

3. NAND Market: Demand for high-capacity QLC SSDs for AI remains strong, and industry inventory levels are expected to reach bottom faster than anticipated.

4.2. Risk Scenario (Bear View): “Winter Looms?”

On the other hand, there are voices warning of a rapid overheating of the market.

In September 2024, investment bank Morgan Stanley dramatically reversed its ‘AI Super Cycle’ forecast from just three months prior in June, releasing a report titled “Winter Looms,” sending shockwaves through the market.

Morgan Stanley’s pessimistic view was based on the following grounds:

1. Excessive Inventory: It presented data showing that inventory levels for general DRAM (62 weeks) and NAND (67 weeks), excluding HBM, were at ‘all-time highs.’ (Although the industry at the time strongly refuted this as “absurd analysis,” it was enough to stir market anxiety.)

2. HBM Oversupply Concerns: With a giant competitor like Samsung Electronics fully entering the HBM market and expanding its production facilities, concerns about HBM oversupply were raised.

In October 2025, iM Securities also forecast that the DRAM and NAND markets in 2026 would enter a phase of ‘gradual slowdown,’ and the HBM market would see a ‘slowdown in explosive growth’ due to intensified competition.

4.3. Overall Conclusion: A New Era Dominated by ‘Technological Integration’ and ‘Geopolitics’

So, what will the market look like in 2026? The opposing forecasts (Bull vs. Bear) paradoxically could both be true. In my opinion, the 2026 market will be a ‘Fragmented’ market where ‘boom’ and ‘bust’ coexist. In other words, it will become difficult to explain the entire market with a single term like ‘super cycle.’

-

Samsung’s ‘optimism’ is focused on the ‘High-End’ markets such as HBM4 and server DRAM, where a clear demand surplus is expected.

-

Conversely, Morgan Stanley’s ‘pessimism’ and iM Securities’ ‘slowdown theory’ focus on the ‘Mid-End’ market below HBM3E and the ‘Low-End’ market of general DRAM/NAND.

- As all three companies ramp up production for HBM3E/4, certain products like HBM3E may experience price normalization (slowed growth) due to intensified competition in 2026.

Therefore, the winner of the future will not be simply the company producing HBM, but the one that preempts ‘HBM4’ and ‘Hybrid Bonding,’ which require the highest technological capabilities.

In conclusion, the semiconductor industry is entering a completely new era.

While the past industry was a ‘capitalistic chicken game’ focused on ‘who can produce more cheaply with more capital,’ the current one is a ’technological game’ focused on ‘who can create higher-performing AI chips.’

And the future will be an era dominated by ’technological convergence,’ where memory and foundry become one, and ‘geopolitical risks’ as the US and China clash.

The winner of this new game will be ’the company that provides an ‘integrated solution’ encompassing ‘memory + foundry + packaging’ (Samsung Electronics’ potential vs. the SK-TSMC alliance). Simultaneously, we must navigate the formidable variable of ‘Intel,’ backed by robust support from the US government, and the dense fog of US political ‘uncertainty.’

Korean companies may have to abandon the myth of the ‘chicken game,’ their past success formula. They are now required to make sophisticated strategic choices to survive on these complex, multi-front battlefields (technology, politics, convergence).