Part 1: The Dollar as a Complex Adaptive System: A History of Crises and Mutations

Chapter 1: The Golden Cage and Its Inherent Flaws

We often think of the global monetary system as a well-oiled machine, operating predictably according to set rules. But frankly, that’s a huge misconception. History shows us sudden crises erupting and unforeseen innovations appearing out of nowhere. To truly understand the monetary system, we need to view it not as a machine, but as a living ecosystem: a ‘Complex Adaptive System (CAS)’.

Complexity economics, originating from the Santa Fe Institute, views the economy not as a balanced machine, but as an organism where the choices of countless individuals converge to create unpredictable, vast currents. Much like the butterfly effect, a small event can shake the entire system, and certain policies can lead to entirely unintended consequences. This is why societies suddenly hit ’tipping points’ of crisis or recovery.

Core Analytical Framework

Therefore, this report will use three core lenses to thoroughly dissect the history of the dollar:

Complex Adaptive System (Macro Lens): We will view the entire dollar system as an ecosystem, examining how it adapts and evolves (sometimes mutating) to external shocks, and how small cracks can lead to the collapse of the entire system.

Hyman Minsky’s Financial Instability Hypothesis (Internal Dynamics Model): This is our lens for looking inside the system. It explains the paradoxical mechanism where prolonged booms and stability lead people to become bolder, increasing debt, and how that very stability sows the seeds of crisis – meaning, “stability begets instability.”

Daniel Kahneman’s Behavioral Economics (Micro Drivers): Finally, we will peer into the minds of the humans participating in the system. We will analyze how policymakers, investors, and the general public fall prey to ‘unwarranted optimism’ or overconfidence, thereby creating the very financial cycles Minsky described.

Combined, these three perspectives reveal that the history of the dollar is not a simple progression, but a continuous evolutionary drama where periods of stability breed crises, these crises trigger ‘mutations’ that fundamentally alter the system, and these mutations then bring about new periods of stability.

The fatal flaw was the ‘Triffin Dilemma.’ The global economy required more dollars to grow. But the more the U.S. printed dollars, the less credible its promise to redeem them for gold on demand became. In essence, the very action the system took to succeed (supplying dollars) became the cause of its downfall (eroding confidence in gold) – a truly self-destructive structure.

As this structural contradiction deepened, the dollar quietly began to reveal another facet: its potential as a geopolitical weapon. The 1956 Suez Crisis was the signal. When Britain and France invaded Egypt, the pound came under speculative attack. At that time, the U.S. Eisenhower administration, which opposed military intervention, used Britain’s financial vulnerability as a ‘perfect lever.’ They pressured Britain by refusing any financial support until it withdrew its troops. Once Britain capitulated, the U.S. miraculously approved a massive $1.3 billion bailout through the IMF. It was a truly ruthless move.

[Window of Analysis: Applying Three Theories]

-

Complexity: The Bretton Woods system, with its rigid gold standard rules, was an artificial system that ran towards its own collapse by failing to adapt to environmental changes. The Triffin Dilemma exemplifies the typical inherent contradiction in complex systems, where success leads to self-destruction.

-

Minsky: The post-war long period of stability was a grand ‘hedging finance’ phase where all participants trusted the rules. However, within that stability, the U.S.’s foreign dollar debt continued to accumulate, becoming a ticking time bomb that amplified future instability.

-

Behavioral Economics: In the Suez Crisis, the U.S. calculated its national interest with rigorous rationality. Conversely, Britain and France, caught in overconfidence from past imperial glories and loss aversion regarding nationalization, made the critical error of completely misjudging U.S. intentions.

Chapter 2: The Great Mutation: The Nixon Shock of 1971

On August 15, 1971, President Nixon’s announcement that the dollar would no longer be convertible to gold is often assessed as a policy failure. However, from a complex systems perspective, this was not a failure but an inevitable and radical evolution – a ‘great mutation’ – undertaken by the system to survive a mortal crisis.

By the late 1960s, the Bretton Woods system was already on the verge of collapse. Due to the massive printing of dollars for the Vietnam War and welfare programs, over $40 billion had been unleashed abroad, while the U.S. only had about $10 billion worth of gold to back it. It was a situation ripe for a ‘bank run’ at any moment.

The fateful decision was made on August 13, 1971, when Nixon secretly summoned economic advisors to Camp David. Following the strong advocacy of Treasury Secretary Connally, Nixon resolved to take the drastic step of suspending gold convertibility. Then, on the evening of August 15, he announced this measure in a televised address, framing it as a great victory that had “protected the U.S. dollar from international speculators.”

The Nixon Shock was an extreme act of self-preservation for the system. It shattered the rules it had created 25 years prior and escaped the ‘golden cage.’ This event declared a new principle to the world: ‘dollar sovereignty.’ It starkly demonstrated that the international monetary system was not a level playing field, but a brutal hierarchy where the center (the U.S.) could change the rules of the game at any time for its survival, and the periphery (the rest of the world) could only adapt to the new reality.

[Window of Analysis: Applying Three Theories]

-

Complexity: The Nixon Shock is a perfect example of a ‘phase transition’ where a system, unable to withstand pressure, suddenly shifts to a different state. The old gold standard collapsed, and a new order emerged: a global fiat currency system, for the first time in human history, untethered from any real asset. This was a radical mutation for survival itself.

-

Minsky: The ‘Minsky Moment’ for the Bretton Woods system had arrived. It was the moment when the foreign dollar debt accumulated during periods of stability crossed a critical threshold, undermining the system’s foundation.

-

Behavioral Economics: The Nixon administration masterfully framed this immense event not as a ‘failure’ but as a ‘victory over speculators’ to gain public support. This is a classic strategy to reduce the psychological shock of a negative event by transforming it into a positive narrative. Furthermore, choosing national interest over international consensus under extreme pressure demonstrates a strong loss aversion tendency.

Chapter 3: A New Symbiosis: The Petrodollar System and the Geopolitics of Debt

Following the Nixon Shock of 1971, the dollar lost its solid anchor in gold and was adrift on the vast ocean. But why continue using this paper money, which couldn’t even be exchanged for gold? Just as everyone was asking this question, the dollar demonstrated yet another remarkable adaptability: it found a new anchor in the world’s most crucial commodity – oil.

The opportunity arose with the 1973 oil shock from the Fourth Arab-Israeli War. As oil prices skyrocketed, Saudi Arabia, earning immense ‘petrodollars,’ needed a safe place to invest this money. Meanwhile, the U.S. desperately needed a new source of demand for the dollar. In July 1974, U.S. Treasury Secretary William Simon flew to Saudi Arabia and proposed a historic deal.

The terms of the agreement were astonishingly simple yet powerful, like a scene from a movie:

- U.S. Provides: Military protection and support for the Saudi royal family.

- Saudi Arabia Provides: All oil sales revenue in dollars only. And then, it would use these earnings (petrodollars) to buy U.S. Treasury bonds.

There was a crucial secret clause: “Saudi Arabia will never disclose its purchase of U.S. Treasury bonds to the public.” The U.S. accepted this condition and maintained this secret for over 40 years.

[Window of Analysis: Applying Three Theories]

-

Complexity: This is a typical adaptation process where a system seeks new stability in response to environmental changes (loss of gold anchor). The dollar utilized a key element of its environment, oil, to create a favorable new symbiotic relationship and a powerful feedback loop.

-

Minsky: This system allowed the U.S. to avoid bankruptcy despite running massive trade deficits. However, in the long run, it laid the groundwork for further system instability by continuously increasing U.S. debt.

-

Behavioral Economics: This transaction cleverly exploited each party’s incentives. The U.S. gained monetary hegemony, and Saudi Arabia secured the safety of its regime. The secrecy clause regarding bond purchases was a strategic decision deeply informed by human psychology, considering the social pressure from public opinion in the Arab world.

Chapter 4: Learning to Manage Fiat Money: The Volcker Shock and the Plaza Accord

The dawn of the pure fiat money era, operating solely on credit without any anchor, led the dollar system into an entirely new experimental ground. The first complete boom-bust cycle, demonstrating how an untethered system operates, unfolded across the 1970s and 1980s. This period vividly illustrated how Minsky’s hypothesis manifested terrifyingly in reality, and how powerful and painful interventions were needed to control this system.

The ‘Great Inflation’ of the 1970s was a catastrophe born from the confluence of the new fiat money system and the oil shocks. As expectations of continuously rising prices spread, the system slipped from Minsky’s ‘speculative’ stage into the ‘Ponzi’ finance stage. The system’s ‘Minsky Moment’ to quell this speculative frenzy began in 1979 with the appointment of Paul Volcker as Federal Reserve Chairman. He prescribed a drastic measure, raising the benchmark interest rate to nearly 20% to break the back of inflation. It was a harsh surgery, intentionally inducing a severe recession to deflate the system’s bubble.

The pain inflicted by Volcker’s high-interest rate policy directly impacted the lives of ordinary Americans. Farmers and construction workers were hit particularly hard. Farmers unable to bear the soaring interest rates drove their tractors to Washington D.C., surrounding the Federal Reserve building and expressing their despair. Homebuilders sent lumber that wouldn’t sell to Volcker’s office in protest. These scenes vividly illustrated the immense social cost incurred to restore stability to the fiat money system.

While Volcker’s shock therapy succeeded in curbing inflation, it created another problem. America’s brutal high-interest rates acted like a black hole, sucking in global capital, and the dollar’s value soared uncontrollably. The strong dollar dealt a fatal blow to U.S. export companies and manufacturers, leading to calls for protectionism in Congress to immediately block imports. To resolve this international dilemma, on September 22, 1985, the finance ministers of the G5 (the U.S., West Germany, France, the UK, and Japan) gathered at the Plaza Hotel in New York. They announced the ‘Plaza Accord,’ an agreement to jointly intervene in foreign exchange markets to artificially lower the dollar’s value. The day after the announcement, the dollar’s value in foreign exchange markets immediately plummeted by 4%.

The Volcker Shock and the Plaza Accord. These two events laid the foundation for today’s fiat money management system. They proved that in a system without automatic anchors like gold, two elements are essential for maintaining stability: First, for domestic stability, a strong and independent manager willing to bear immense political and social costs to control prices – a central bank, an ‘anchor of trust.’ Second, for international stability, active political cooperation among key countries – an ‘anchor of cooperation.’

The period from 1979 to 1985 was a process of maturation for the fiat money system, where it learned that it wasn’t a self-regulating entity but one that constantly required active management.

[Window of Analysis: Applying Three Theories]

-

Complexity: The inflation of the 1970s was a process of the system losing stability and descending into chaos. The Volcker Shock was a powerful external intervention to return the system to a stable state. The Plaza Accord was another form of adaptive strategy where major players in the system cooperated to artificially adjust the system’s equilibrium.

-

Minsky: The 1970s were an era of ‘speculative/Ponzi finance’ where inflation expectations fueled debt. Volcker’s tightening was a ‘Minsky Moment’ that forcibly burst this bubble, and the subsequent recession was a painful process of debt liquidation.

-

Behavioral Economics: Volcker used shock therapy to break the collective psychology of ‘inflation expectations.’ This was an attempt to shatter psychological anchoring effects, which are difficult to explain with rational economic models. The Plaza Accord is a prime example of maximizing the ‘announcement effect,’ altering market expectations solely through its announcement.

Chapter 5: The Pinnacle of the Minsky-Kahneman Cycle: The 2008 Global Financial Crisis

The 2008 Global Financial Crisis is a textbook example of how the modern Minsky-Kahneman cycle operates. It was a perfect storm created by the confluence of systemic vulnerabilities and human psychology. The long period of low inflation and stable growth that followed the Volcker Shock in the 1980s, the so-called ‘Great Moderation,’ paradoxically nurtured the seeds of crisis. As Minsky put it, this tedious stability eroded people’s vigilance, leading them to take on increasingly greater risks. And that madness perfectly manifested the three stages of finance described by Minsky in the U.S. housing market before exploding.

- Hedge Finance: Ordinary 30-year fixed-rate mortgages, where both principal and interest could be repaid.

- Speculative Finance: Loans where only interest could be barely paid. These borrowers bet that housing prices would continue to rise, allowing them to refinance into better terms later.

- Ponzi Finance: Or, to be precise, this wasn’t even finance. Subprime, adjustable-rate mortgages were issued indiscriminately to individuals with no income, no job, and no assets (NINJA). They relied solely on the skyrocketing housing prices to avoid default – essentially a game of hot potato.

Fueling this insane race was the human cognitive bias explained by Daniel Kahneman. Homebuyers, lending banks, and credit rating agencies all fell prey to a widespread overconfidence and delusional optimism: “U.S. housing prices will never fall!” The greed for immediate profits completely numbed any rational fear of loss.

The climax of the crisis arrived on the fateful weekend before the Lehman Brothers bankruptcy in September 2008. Treasury Secretary Henry Paulson urgently summoned Wall Street CEOs to the Federal Reserve Bank of New York. Paulson threatened, “There is not a penny of government money available!” But ultimately, no one was willing to save Lehman, and on Monday morning, Lehman filed for bankruptcy.

The 2008 financial crisis exposed how complex the modern financial system is, and how its complexity far exceeded the understanding of regulators and market participants. Derivatives with complex names like CDOs and CDS had so cleverly spread risk worldwide that, until the ‘Minsky Moment’ struck, no one knew where or how much of the bomb was hidden. The zero interest rates and quantitative easing poured in to prevent a collapse prevented immediate devastation but left deep scars of massive government debt and a breakdown of trust. And these scars directly led to the U.S. resorting to radical strategies in 2025.

[Window of Analysis: Applying Three Theories]

-

Complexity: When the single point of failure, Lehman Brothers, collapsed, the entire system, following countless interconnected links that were previously unseen, began to collapse sequentially – a ‘phase transition.’ Financial innovation had made the system excessively complex and interconnected, paradoxically making the whole more fragile.

-

Minsky: This is a perfect example of how the ‘Great Moderation’ fueled ‘speculative/Ponzi finance.’ Lehman’s bankruptcy was a clear ‘Minsky Moment,’ signaling that the accumulated debt in the system could no longer be sustained.

-

Behavioral Economics: The collective belief that “housing prices will never fall” was the crystallization of ‘delusional optimism’ and ‘overconfidence.’ Credit rating agencies, succumbing to ‘confirmation bias’ by favoring information that aligned with their interests, willfully ignored warning signs, acting as a psychological engine accelerating the crisis.

Chapter 6: The First Cracks in the Consensus: The 2015 AIIB Incident

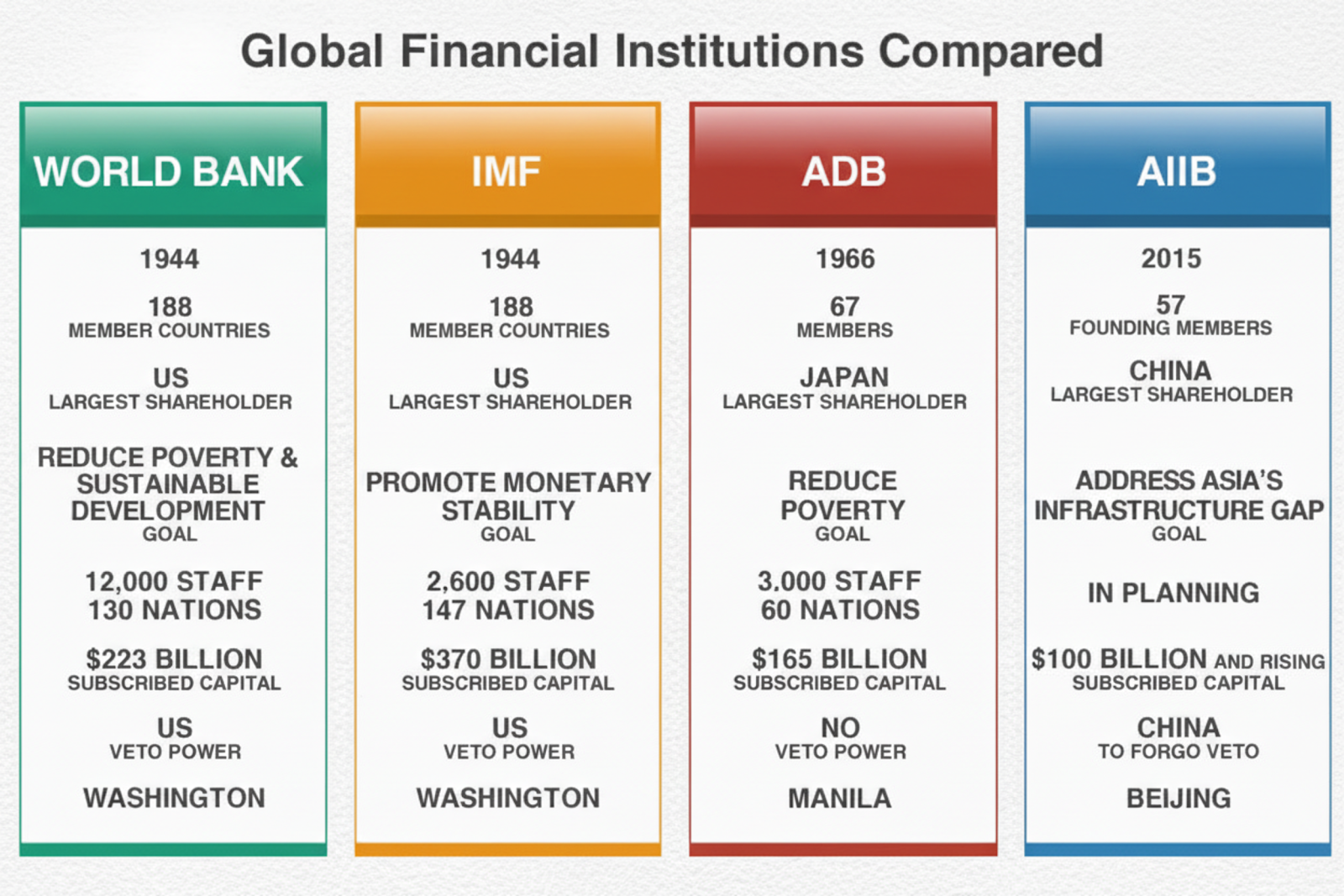

Following the 2008 crisis, the dollar system began to face a different kind of pressure. The geopolitical consensus that had solidly supported the system started to show invisible cracks. The era of U.S. ‘sole superpower’ status in the 1990s waned, and with the rise of new powers like China, the gravitational map of the global economy was shifting. These new powerhouses were no longer satisfied with the U.S.-led order of the IMF and World Bank and began creating their own parallel universes.

The 2015 Asian Infrastructure Investment Bank (AIIB) incident was a symbolic event showcasing this change. The Obama administration strongly pressured its allies not to participate in the establishment of the AIIB, led by China. However, in March 2015, Britain, the U.S.’s closest ally, betrayed Washington by declaring its participation as a founding member of the AIIB – a bombshell announcement.

This event was recorded as a significant diplomatic defeat for the United States. Former Treasury Secretary Larry Summers even commented that it “might be remembered as the moment the United States lost its role as the guarantor of the global economic system.” The AIIB incident demonstrated that even the U.S.’s key allies were beginning to prioritize long-term economic interests over geopolitical loyalty. You’ve probably had similar experiences – moments when new opportunities feel more important than relationships with old friends.

It signaled a fundamental shift in the cost-benefit calculation that had sustained the dollar-centric system for the past 70 years. Allies were now choosing ‘geopolitical hedging,’ not putting all their eggs in the U.S. basket but diversifying some into the newly emerging Chinese basket. Therefore, this incident was not simply about the creation of a new bank. It was a clear sign that the solid consensus underpinning dollar hegemony was slowly melting away, and it provides a crucial background for understanding why the U.S. would later be compelled to resort to coercive measures rather than consensus-based diplomacy – the ‘Turnberry System.’

[Window of Analysis: Applying Three Theories]

-

Complexity: The emergence of China as a powerful new ‘species’ in the dollar system ecosystem is fundamentally altering its structure. U.S. allies are exhibiting adaptive behavior, increasing their chances of survival by engaging with multiple centers of power rather than relying solely on one.

-

Minsky: This reflects not a financial cycle but a crack in geopolitical stability. As the value of the public good – ‘security and prosperity’ – provided by the U.S. diminished, the geopolitical order that depended on that stability began to falter.

-

Behavioral Economics: Britain’s decision can be seen as a highly rational calculation that overcame the status quo bias of geopolitical loyalty, giving greater weight to the opportunity cost and regret aversion of not participating in China-led growth.

Part 2: Adaptation in 2025: A New Grand Strategy for Dollar Hegemony

Introduction: The End of an Era and the Dawn of a New Strategy

And now, in 2025, the U.S. dollar’s status as the reserve currency faces challenges from all sides. This is not merely an economic cycle issue; it’s a fundamental signal that the global order is changing. The massive U.S. trade deficits accumulated over decades have become a ticking time bomb, and China’s grand ambitions, such as ‘Made in China 2025,’ represent the most potent challenge to U.S. hegemony. Furthermore, the emergence of financial technologies like CBDCs and stablecoins is shaking the foundations of the existing monetary order.

In the face of such complex crises, the U.S. has essentially torn up the rules of free trade and multilateralism it created after World War II and unveiled a grand strategy based on two entirely new pillars. This is not a series of fragmented policies. It is a consistent, bold, yet simultaneously incredibly risky national grand strategy aimed at re-establishing U.S. economic dominance.

The first pillar is the ‘Managed Trade’ regime. This involves using tariffs as a key weapon to reshape the trade patterns of allies and competitors according to U.S. preferences. The second pillar is the ‘Digital Currency Hegemony’ strategy. Instead of the government directly creating digital currency, it aims to secure the dollar’s influence in the digital age by bringing dollar-linked stablecoins issued by private companies into the regulatory framework.

These two strategies do not operate independently. They form a perfectly complementary and reinforcing system. The aggressive tariff policy, known as the ‘Turnberry System,’ directly targets the dollar system’s long-standing weakness – the trade deficit – aiming to bring key industries back to the U.S. However, such protectionism inevitably entails massive government spending and debt. This is where the stablecoin strategy plays a crucial role.

The ‘GENIUS Act,’ enacted in 2025, mandates that stablecoin companies must hold U.S. Treasury bonds as reserves. This creates a new global demand source to absorb the burgeoning U.S. government debt. In other words, the stablecoin policy acts as a financial buffer, mitigating the fiscal instability that the tariff policy might cause. It forms a closed loop that upgrades the dollar’s financial infrastructure for the digital age while simultaneously securing the funding for the new protectionist era. This is the moment when trade policy and financial policy perfectly merge into a single geopolitical weapon.

Chapter 7: The ‘Turnberry System’ – Trade as a Geopolitical Tool

7.1 The Philosophy of Reciprocity and Protectionism: The End of the Bretton Woods System

In 2025, U.S. trade policy underwent a fundamental philosophical shift. It abandoned multilateralism governed by international organizations like the WTO and returned to a bilateral, transactional approach that uses tariffs as a tool for negotiation, pressure, and even revenue generation. The emergence of this new trade doctrine is symbolized by the ‘Turnberry System,’ named after the golf resort in Scotland where U.S.-EU trade negotiations were concluded in July 2025. The U.S. Trade Representative’s office openly declared this system as the beginning of a new international order that would replace the Bretton Woods system.

The core idea of the Turnberry System is ‘fair and balanced trade.’ This is essentially a declaration that the U.S. can no longer tolerate its chronic trade deficit. To resolve this, any means, including tariff barriers, can be used, disregarding WTO rules. The other pillar is a return to the ‘production economy.’ Moving beyond a consumption-based economy, it aims to revive manufacturing and create good jobs to rebuild the American middle class. Ultimately, the Turnberry System is a stark expression of economic realism that prioritizes the logic of power between nations and the maximization of national interest over the beautiful ideals of free trade.

7.2 Analysis of Bilateral Trade Negotiations

The Turnberry System clearly divides trading partners into allies, competitors, and outsiders, approaching them differentially.

- U.S.-EU Agreement: Managed Partnership The negotiations between the U.S. and the EU were the result of accumulated grievances on both sides. The U.S. was burdened by a massive trade deficit, while the EU had many complaints about U.S. Big Tech companies. The core of the agreement, concluded in July 2025, is ‘managed trade,’ establishing upper limits on tariffs. The U.S. agreed to a comprehensive 15% tariff cap on most EU imports. In return, the EU presented ’targets’ to purchase substantial amounts of U.S. energy and AI chips by 2028 and invest in U.S. strategic industries. But the most crucial point is this: the U.S. reserved the right to unilaterally impose additional tariffs if the EU failed to meet its commitments to the U.S.’s satisfaction. This wasn’t free trade; it was the institutionalization of predictable protectionism based on U.S. power.

- U.S.-Japan Strategic Alliance: Investment for Market Access Negotiations with Japan began after President Trump threatened to impose a 25% tariff on Japanese cars. The core of the agreement is that Japan will invest $550 billion in key U.S. strategic sectors like semiconductors and pharmaceuticals by 2029, in exchange for the U.S. lowering tariffs on Japanese imports to 15%. This is less a trade negotiation and more a new form of economic alliance, or perhaps even economic tribute, drawing the capital of an ally into U.S. industrial policy.

- Korea-U.S. Framework: A Late Compromise South Korea missed the negotiation timing due to domestic political issues in the first half of 2025, facing severe consequences such as a sharp decline in automotive exports to the U.S. After a full-fledged effort, a compromise was finally reached on July 30, agreeing to lower mutual tariffs to 15%. This agreement was reached amidst a complex backdrop where the U.S. largely eliminated green subsidies from the IRA in exchange for increased advanced manufacturing tax credits for Korean semiconductor companies investing in the U.S. The simultaneous use of the ‘stick’ of tariffs and the ‘carrot’ of subsidies for specific industries clearly indicates the intention to reshape the industrial structure of allies in favor of the U.S.

- U.S.-China Confrontation: All-Out Economic War U.S.-China relations escalated into an all-out economic war in late 2025 when China announced large-scale export controls. The U.S. immediately retaliated by imposing an additional 100% tariff on all Chinese products starting November 1. This measure is virtually equivalent to an import ban, with some items facing tariffs as high as 145%. This marked the reality of strategic decoupling between the two economies and signaled the full-scale launch of ‘fragmented globalization,’ where the world economy is splitting into U.S.-centric and China-centric supply chains.

- U.S.-India and U.S.-Brazil: Punitive Turn For countries like India and Brazil, which refuse to take sides, the Turnberry System functions as a pure tool of punishment. The U.S. imposed a 50% high tariff on India for continuing to import Russian crude oil and actively participating in BRICS activities. Brazil also faced a 50% tariff, with the U.S. citing its domestic political situation. These examples starkly illustrate how U.S. trade policy has become a weapon beyond economic logic, used to punish countries that defy it diplomatically and even intervene in their domestic affairs.

| Trading Partner | Base Tariff Rate | Key Sector Tariffs | Reciprocal Undertakings (Promises) | U.S. Strategic Objectives | Current Status and Outlook |

|---|---|---|---|---|---|

| European Union (EU) | 15% (Cap) | Automobiles: 15% (Cap) | Purchase of $750 billion in energy and $40 billion in AI chips, $600 billion in strategic investments (target) | Secure purchase commitments, counter digital tax/CBAM | Stable, but potential conflict points like digital tax remain |

| Japan | 15% | Automobiles: 15% | Investment of $550 billion in strategic sectors (semiconductors, critical minerals, etc.), increased purchase of agricultural products/energy | Attract strategic capital investment, realign supply chains | Stable, but uncertainty in the automotive sector due to IRA repeal |

| South Korea | 15% | Automobiles: 15% | Promise of strategic sector investment (specific terms under negotiation) | Attract investment in key industries like semiconductors, strengthen supply chain alliance | Basic agreement is stable, but friction continues over detailed investment terms |

| China | Over 100% | High tariffs across all categories | None (mutual retaliation) | Technical/economic decoupling, exclusion of China from supply chains | All-out economic war, escalating conflict |

| India | 50% | High tariffs across the board (punitive measure) | None | Punishment for diplomatic non-compliance, challenging strategic autonomy | Diplomatic/trade crisis, weakened strategic cooperation |

| Brazil | 50% | High tariffs across the board (including beef, coffee) (punitive measure) | None | Exert influence on Brazil’s domestic politics | Continued confrontation, acceleration of Brazil’s export diversification |

| Vietnam | 20% | Electronics: 20%, 40% if containing large amounts of Chinese components | Duty-free access and market access for U.S. products | Block China-alternative supply chains, resolve trade imbalance | Agreement reached, but uncertainty remains due to ambiguity in transshipment rules |

7.3 Comprehensive Analysis and Long-Term Impact of the Turnberry System

The Turnberry System is completely shaking global supply chains. Companies are rushing to India and Vietnam under the ‘China Plus One’ strategy to avoid geopolitical risks. Apple’s plan to move 25% of iPhone production to India and transfer other product manufacturing to Vietnam is a prime example. However, as the Vietnam case shows, new production bases can also be hit by U.S. tariffs at any time. This means companies are not just moving factories to cheaper locations, but are facing strong pressure to ‘friend-shore’ or ’near-shore’ to politically stable regions.

From a macroeconomic perspective, the U.S.’s new tariff policy is delivering a massive ’negative supply shock’ to the global economy. Import prices are rising, increasing inflationary pressure, while declining trade and rising uncertainty heighten the risk of recession – classic factors for stagflation. According to an analysis by the Wharton School at the University of Pennsylvania, such tariff policies could reduce U.S. GDP by 6% and wages by 5% in the long run.

The essence of the Turnberry System is ultimately a new global trade operating system based on the logic of power: managed bilateralism. It replaces the rule-of-law-based system like the WTO with a ‘hub and spoke’ model where the U.S. is the central axis and other countries are the spokes. In this model, market access is no longer a right but a privilege that must be earned by conforming to U.S. strategies and paying the price. This is the U.S.’s blatant response to the departure of its allies revealed in the AIIB incident. If persuasion doesn’t work, it will be enforced by power. Consequently, global trade is divided into three tiers: allies who pay and gain managed market access, outsiders facing punitive barriers, and competitors who become targets of economic warfare. This is the blueprint for the newly forming fragmented global economic order.

Chapter 8: The Digital Dollar Gambit – Stablecoins as Strategic Assets

8.1 The U.S. Approach: The GENIUS Act and the Rise of ‘Synthetic CBDCs’

The U.S. approach to the digital currency era is truly unique. Instead of the central bank directly creating its own digital currency, it has adopted a strategy of bringing privately issued stablecoins into the regulatory fold. The legal foundation for this strategy is the ‘U.S. Stablecoin Innovation Leadership and Establishment Act (GENIUS Act),’ enacted on July 18, 2025.

The core of the GENIUS Act is simple: Only authorized financial institutions can issue stablecoins, and they must hold 100% reserves equal to the value of the issued coins. Crucially, these reserves must be held solely in ultra-safe assets like U.S. dollar cash or short-term Treasury bonds. The strategic objective of this act is crystal clear: to force the reserves of the globally growing stablecoin market to be held in U.S. Treasury bonds, thereby creating a new global demand for purchasing U.S. government debt and strengthening the dollar’s reserve currency status. Furthermore, by mandating anti-money laundering obligations for all issuers and requiring them to have the technology to freeze or seize assets when necessary, it aims to extend U.S. financial sanctions capabilities into the digital world.

This approach is effectively creating ‘synthetic’ or ‘indirect’ CBDCs without direct government issuance. The private sector handles innovation, while the government controls the core of the system – the reserves. This is a solution perfectly suited to American capitalism, avoiding the various political and technical burdens of direct government CBDC issuance while still maintaining control. If you think about it, the logic is the same as the Petrodollar system in 1974, which outsourced dollar demand creation to OPEC. This time, it’s a ‘Digital Petrodollar 2.0’ strategy, outsourcing dollar demand creation to private tech companies. Truly a clever move.

8.2 China’s Counterattack: e-CNY and the Journey Towards Monetary Sovereignty

On the opposite side of the U.S. strategy, China is betting everything on the development of the digital yuan (e-CNY), issued directly by its central bank. The e-CNY operates on a ’two-tier’ structure, with the People’s Bank of China issuing it and commercial banks handling its distribution. It follows the principle of ‘anonymous for small amounts, traceable for large amounts.’

The true strategic goal of the e-CNY is the internationalization of the yuan. China is promoting the overseas use of e-CNY by collaborating with the Bank for International Settlements (BIS) and other central banks on the ‘mBridge project.’ mBridge is a multi-CBDC platform that allows direct exchange of CBDCs from various countries on a single platform. This is an attempt to create a new financial highway that bypasses SWIFT, the dollar-centric international payment network, and can be seen as a direct challenge to dollar hegemony.

8.3 Comparative Analysis: Why Stablecoins Instead of CBDC? U.S. Strategic Intentions

The U.S.’s choice of private stablecoins over a state-led CBDC, unlike China, is based on multiple layers of strategic calculation.

- Economic Intent: Weaponizing Reserve Demand This is the most crucial reason. Through the GENIUS Act, it has mandated that the reserves of the global stablecoin market be held in U.S. Treasury bonds. This means securing a powerful and permanent demand base for financing America’s enormous national debt at a low cost. In essence, it aims to protect dollar hegemony by creating a virtuous cycle where the growth of dollar-based digital assets increases demand for U.S. Treasury bonds.

- Political Intent: The ‘Privacy’ Gambit The U.S. government officially opposes the introduction of CBDC, citing concerns about privacy infringements due to the government’s ability to monitor all individual transactions. This is a politically very shrewd move. Through this framing, it can leverage private sector innovation while avoiding sensitive domestic debates. Simultaneously, it can frame China’s e-CNY as a ‘Big Brother’ system and gain an ideological advantage by positioning its own private-sector-led model as an alternative that respects freedom and privacy.

- Geopolitical Intent: A New Vector for Sanctions Enforcement A regulated stablecoin ecosystem grants the U.S. Treasury a far more powerful sanctions tool than before. The GENIUS Act mandates that stablecoin issuers have the technical capability to freeze, seize, or even burn (delete) assets from specific addresses upon court order. This means the U.S. can exert its financial power directly and with surgical precision on the blockchain, far more efficiently and powerfully than current SWIFT sanctions, which require going through multiple banks.

| Category | U.S. Regulated Stablecoin Ecosystem (GENIUS Act) | China’s CBDC (e-CNY) |

|---|---|---|

| Governance Model | Private-led, government regulated (Public-Private Partnership) | State-led, central bank direct issuance (State-Led) |

| Core Strategic Goal | Strengthen dollar hegemony (Create demand for U.S. Treasury bonds) | Internationalize the yuan (Bypass the dollar system) |

| Privacy Structure | Relies on issuer/exchange AML/KYC; government access when necessary | Managed anonymity (anonymous for small amounts, traceable for large amounts) |

| Technology Stack | Utilizes various public/private blockchains (Ethereum, Solana, etc.) | Centralized DLT system controlled by the People’s Bank of China |

| Cross-Border Strategy | Encourages global spread of private stablecoins | Direct country-to-country linkages through multi-CBDC platforms like mBridge |

| Sanctions Enforcement Mechanism | Asset freeze/seizure/burning through legal orders to issuers | Direct transaction control and freezing by the central bank |

| Private Sector Role | Leading role in technological innovation, issuance, circulation, wallet services, etc. | Acts as a second-tier partner to the central bank for distribution and service provision |

Part 3: The Future of a Divided World

Chapter 9: The Battle for Global Financial Plumbing

The emergence of the U.S. stablecoin ecosystem and China’s mBridge network poses an existential threat to SWIFT, which has monopolized the international payment market for decades. SWIFT, in fact, only transmits messages; actual money transfers require going through multiple banks, making it time-consuming and expensive. However, stablecoins and CBDCs have the potential to enable cross-border payments between individuals in near real-time and at low cost, without intermediate steps.

To counter this challenge, SWIFT is also attempting a self-disruptive innovation. It aims to become a neutral ‘bridge layer’ or ’transfer hub’ connecting various CBDCs and tokenized asset networks, without being tied to any specific technology or currency. The idea is to leverage its existing vast banking network and embrace the new digital asset era, thereby becoming a central part of the new ecosystem rather than becoming obsolete.

However, the larger trend is ‘financial balkanization.’ The world is moving towards an era where multiple systems compete, centered around geopolitical blocs, instead of a single global payment system. At least three blocs are visible: (1) The U.S. dollar-based stablecoin zone, (2) The e-CNY and mBridge zone based on the Chinese yuan, and (3) The digital euro zone promoted by Europe.

This financial fragmentation can lead to serious risks. If blocks are incompatible, trade and capital flow costs will increase, making them inefficient. The risk of financial crises spreading globally will also increase due to difficulties in inter-bloc cooperation during a crisis. Ultimately, the potential for global economic growth could be undermined as capital flows become confined within geopolitical borders. The U.S. ‘Turnberry-Stablecoin’ closed loop is a microcosm of this global trend. This fragmented globalization, where trade, technology, and finance are all confined within geopolitical boundaries, signifies the end of globalization as we knew it.

Conclusion: A Grand Experiment and Its Dangers

As analyzed above, in 2025, the U.S. is pushing forward with ‘Managed Trade’ under the ‘Turnberry System’ and the stablecoin strategy of the ‘Digital Dollar Gambit’ as two massive pillars to create a new U.S.-centric global economic order. These two pillars are incredibly ambitious attempts to control both the rules of physical commodity trade (tariffs) and the flow of digital finance (stablecoins). This is also the latest version of the cycle of crisis and adaptation that has endlessly repeated throughout the history of the dollar system.

As we reflect on this evolutionary trajectory, the debasement of currency in the Roman Empire, a powerful historical analogy, comes to mind. Rome continuously reduced the silver content in its coins to finance wars. The U.S., in a conceptual sense, has also undertaken a devaluation. In 1971, it severed its link to gold, and since 2008, it has printed money on an unprecedented scale through quantitative easing.

From the perspective of a complex adaptive system, the U.S.’s 2025 strategy is an attempt to artificially reintroduce a hierarchical, centrally controlled order, defying the natural flow of a multipolar and decentralized ecosystem.

History warns us that such attempts can often lead to unintended catastrophic consequences. The greatest danger is that America’s aggressive unilateralism will produce the opposite result: the U.S.’s pressure could drive competitors and non-aligned nations closer together, accelerating the formation of an opposing economic bloc led by China and Russia. This could irrevocably turn the very de-dollarization and global economic fragmentation that the U.S. sought to prevent into an irreversible reality.

In conclusion, 2025 is a critical turning point that will determine the future of dollar hegemony and the direction of the global economic order. The next decade will see the world become a stage for a grand experiment, observing whether this new art of national economic management will successfully rebuild U.S. hegemony or act as a catalyst for the advent of a multipolar world. Will this grand experiment succeed, or will it open Pandora’s Box?

References

- Santa Fe Institute. (2024). Complexity economics offers new tools for today’s global challenges.

- Mehrling, P. G. (2022). Minsky’s Financial Instability Hypothesis and Modern Economics. Boston University.

- International Monetary Fund. (2021). People in Economics: Daniel Kahneman. Finance & Development.

- U.S. Department of State, Office of the Historian. Nixon and the End of the Bretton Woods System, 1971–1973.

- Federal Reserve History. Nixon Ends Convertibility of U.S. Dollars to Gold and Announces Wage/Price Controls.

- International Monetary Fund. (2000). Nothwest of Suez: The 1956 Crisis and the IMF. WP/00/192.

- CounterPunch.org. (2016). The Petrodollar - The US-Saudi Deal that Ruined the World.

- The Economic Times. (2016). The untold story behind Saudi Arabia’s 41-year US debt secret.

- PBS. (2019). Column: Paul Volcker’s legacy, an independent Federal Reserve, is under threat.

- National Bureau of Economic Research (NBER). (2015). The Plaza Accord, 30 Years Later.

- Wharton School, University of Pennsylvania. (2018). Remembering ‘Lehman Weekend’: Where Are the Risks Now?

- American Economic Association. (2010). Risk Management Failures.

- The Guardian. (2015). US anger at Britain joining Chinese-led investment bank AIIB.

- The World Economic Forum. (2015). What does the AIIB mean for US global influence?

- United States Trade Representative (USTR). (2025). The President’s 2025 Trade Policy Agenda.

- Penn Wharton Budget Model. (2024). The Economic Effects of President Trump’s Tariffs.

- Peterson Institute for International Economics (PIIE). (2024). The global economic effects of Trump’s 2025 tariffs.

- The White House. (2025). Fact Sheet: President Donald J. Trump Signs GENIUS Act into Law.

- U.S. Department of the Treasury. (2023). Report on Stablecoins.

- Federal Reserve Board. (2022). Money and Payments: The U.S. Dollar in the Age of Digital Transformation.

- Bank for International Settlements (BIS). (2022). E-CNY: main objectives, guiding principles and inclusion considerations.

- Bank for International Settlements (BIS). (2024). Project mBridge reached minimum viable product stage.

- Atlantic Council. (2023). Not so fast: The case for a new SWIFT.

- SWIFT. (2024). Ground-breaking Swift innovation paves way for global use of CBDCs and tokenised assets.

- International Monetary Fund. (2023). Geopolitics and Fragmentation Emerge as Serious Financial Stability Threats.

- McKinsey & Company. (2022). Globalization in transition: The future of trade and value chains.

- CADTM (Committee for the Abolition of Illegitimate Debt). (2023). The BRICS and de-dollarisation.

- Center for a New American Security (CNAS). (2022). The Promises and Perils of Central Bank Digital Currencies.

- Investopedia. (2024). Understanding Currency Debasement: Definition and Historical Examples.

- Harvard Kennedy School. (2019). Rise of Economic Nationalism.