Unraveling the Secrets of My Mind Through Behavioral Economics

The Secret of Failed New Year’s Resolutions and Expensive Gym Memberships

As the saying goes, “Well begun is half done,” we always resolve to be better than we were yesterday. When the new year arrives, we set ambitious plans for quitting smoking, dieting, and learning foreign languages, yet somehow, these resolutions often end up as short-lived commitments. Especially, the gym memberships we invest in with great determination often end up gathering dust in a drawer, turning into ‘donation certificates’—a common experience for many.

Is it really because we lack willpower or are particularly lazy compared to others? Behavioral Economics shakes its head. This field questions the traditional economic assumption that humans always make rational and logical decisions. At the intersection of psychology and economics, it deeply explores how humans, whom we believe to be rational, actually make irrational and impulsive choices, and what the underlying ‘reasons’ for these behaviors are.

This article is a journey to find answers to that ‘why’. It’s like obtaining a user manual for my mind. The moment we understand ‘why we did that’, our next choices will surely change.

Chapter 1. The Battle Within: ‘Current Me’ vs. ‘Future Me’

The biggest reason our resolutions crumble time and again is the constant battle between ‘current me’ and ‘future me’. Behavioral economics explains this through the concepts of ‘Present Bias’ and ‘Hyperbolic Discounting’. Simply put, people tend to prefer small rewards in the present over larger rewards in the distant future. This powerful bias leads us to continually fail in achieving long-term goals.

1.1. Case Study: The Paradox of Gym Memberships

The experience of signing up for a gym with high hopes but only attending a few times is a classic example of present bias. It’s not merely a matter of laziness; it results from ‘overconfidence’, where the current self excessively believes that ‘future me will definitely exercise regularly!’

Looking at the famous gym study by Stanford’s DellaVigna and Malmendier, we can see how clearly this phenomenon manifests. According to the research, members who chose a monthly fee of over $70 visited the gym an average of 4.3 times a month. This translates to over $17 per visit. However, they had a much cheaper option of a ‘10-visit pass’ at $10 per visit. Yet, 80% of those who chose the monthly fee visited the same number of times but paid more, resulting in an average loss of **$600 (approximately 830,000 KRW)** over the membership period.

Interestingly, these members took an average of 2.31 months after their last gym visit to cancel their contracts. They not only believed that future me would exercise diligently but also overestimated their ability to cancel immediately if they stopped exercising. People paid a premium for the option of ‘flexibility’ but underestimated their ‘future inertia’, failing to act on that flexibility and wasting money in the process. This is not a matter of poor financial calculation but a systematic error stemming from a ‘failure of self-awareness’ in accurately predicting future emotions and behaviors.

Cost and Loss Analysis by Gym Contract Type

| Contract Type | Average Monthly Visits | Actual Cost per Visit |

|---|---|---|

| Monthly Fee Contract (> $70) | 4.3 visits | > $17 |

| 10-Visit Pass ($10/visit) | - | $10 |

Source: DellaVigna & Malmendier (2006)

1.2. Case Study: Common Enemy Hidden in Diabetes and Smartphone Addiction

Present bias is not limited to financial matters. It deeply affects various aspects of our lives, including healthcare and addiction.

A study conducted at Keimyung University’s Dong San Hospital on patients with Type 2 diabetes revealed fascinating insights. The study divided patients into two groups: those hospitalized due to poor blood sugar control (‘hospitalized group’) and those managed through outpatient care (‘outpatient group’) and conducted a ‘Delay Discounting Task’. This task measured how quickly participants devalued future rewards by asking them to choose between “a small amount of money now” and “a larger amount later (100,000 KRW)”.

The results were surprising. The hospitalized group significantly devalued future rewards compared to the outpatient group, indicating a notably high ‘delay discount rate’. A clear negative correlation emerged, showing that the higher the HbA1c level (a key indicator of blood sugar control), the lower the value placed on future rewards.

This decision-making pattern in the brain was similarly found in studies on adolescent smartphone addiction. Teens classified as at risk for smartphone addiction exhibited significantly higher delay discount rates than regular users, indicating greater impulsivity.

Though these two cases appear different on the surface, they operate under the same cognitive mechanism. The brain’s inability to resist the immediate temptation of sweet and fatty foods, leading to poor blood sugar management, is fundamentally the same as postponing important future tasks in favor of the immediate pleasure provided by smartphones. This shows that present bias is not just about individual financial choices but a fundamental ‘cognitive trait’ that determines health and well-being. Thus, simple advice like “exercise more” or “stop using your smartphone” often fails because the issue lies not in willpower or lack of information but in the fundamental workings of our brain in evaluating reward value.

Chapter 2. When We Can’t Rely Solely on Willpower: Designing Smart Systems for Success

If ‘current me’ struggles to overcome ‘future me’, what should we do? Behavioral economics advises us not to blame willpower alone but to design smart devices that ‘current me’ can set up to prevent ‘future me’ from succumbing to temptation. This is called a ‘Commitment Device’.

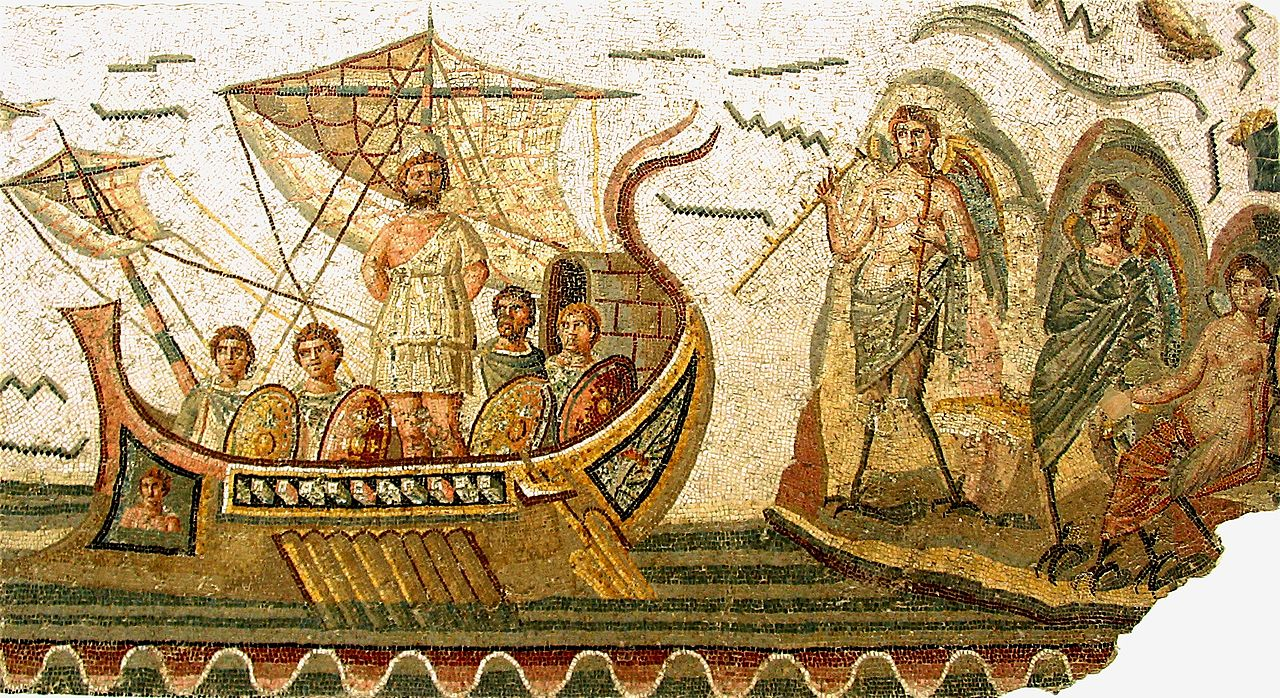

2.1. The Wisdom of Odysseus: Tie Yourself Up

In ancient Greek mythology, the hero Odysseus had to pass through the sea of the witch ‘Siren’, who lured sailors to their doom with her beautiful song. He wanted to hear the Siren’s song but did not want to be tempted and shipwrecked. So, what did Odysseus do? He ordered his men to tie him tightly to the mast and commanded them not to release him, no matter what he said, while leaving his ears unblocked with wax.

This is a perfect example of a commitment device, where ‘current me’ (the rational self) prevents ‘future me’ (the self enchanted by the Siren’s song) from engaging in irrational behavior. Like Odysseus, we can predict our susceptibility to temptation and apply smart systems that tie ourselves up in our lives.

2.2. Case Study: The Nobel Prize-Winning Savings Program, ‘Save More Tomorrow™’

The ‘Save More Tomorrow™ (SMarT)’ program, designed by behavioral economics expert and Nobel laureate Richard Thaler, is one of the most successful examples of a commitment device that turns human weaknesses into a driving force for success. This program dramatically increased savings rates by cleverly leveraging ’loss aversion’ and ‘status quo bias (laziness)’, which are reasons people struggle to save.

- Core Principle 1 (Using Loss Aversion): People tend to perceive a decrease in their monthly salary as a ’loss’, making them reluctant to increase their savings. To address this, the SMarT program cleverly linked the timing of increased savings to ‘future salary increases’. As a result, participants did not experience the painful experience of seeing their take-home pay decrease on their paychecks, significantly reducing their psychological resistance to saving.

- Core Principle 2 (Using Status Quo Bias): People tend to dislike changing something once it has been set. SMarT utilized this ‘inertia’. Once participants enrolled in the program, their savings rate was designed to ‘automatically’ increase with each salary increase. To stop saving, they had to go through the cumbersome action of ‘actively opting out’. Consequently, most people remained passive, and their laziness became a driving force for increased savings.

The results of this program were astonishing. The average savings rate of participants in the initial experiment soared from 3.5% to 13.6% in just 28 months—more than three times. Even more remarkably, 80% of participants maintained the program through four salary increases.

The genius of the SMarT program lies in its refusal to criticize or fix human ‘flaws’. Instead, it used these flaws as a stepping stone to success. This represents a paradigm shift from the perspective of self-improvement, which aims to ‘become a better human’, to the perspective of system design, which aims to ‘create better systems that acknowledge human nature’. This is the essence of the philosophy of ‘Libertarian Paternalism’, which respects individual freedom of choice while guiding toward better outcomes.

Changes in Savings Rates of SMarT Program Participants

| Group | Pre-Implementation Savings Rate | Post-Implementation Savings Rate |

|---|---|---|

| SMarT Participants (Mid-sized Manufacturing Company) | 3.5% | 13.6% |

Source: Thaler & Benartzi (2004)

2.3. Case Study: The Butterfly Effect of Small Savings Accounts in the Philippines

Commitment devices have the potential to change not only individual goal achievement but also social relationships and structures.

A research team led by Ashraf, Karlan, and Yin launched a special savings product called ‘SEED (Save, Earn, Enjoy Deposits)’ in collaboration with a bank in the Philippines. This product was a ‘commitment savings’ account that required participants to set a target amount or date when opening the account, preventing withdrawals until that time.

The results of the experiment were highly successful. The group offered this product increased their average savings by 81% after 12 months compared to the control group. Particularly interesting was that women who showed tendencies of present bias in pre-surveys were significantly more likely to enroll in this product. This indicates that those who struggle with self-control actively sought commitment devices to solve their problems.

However, the most surprising outcome was elsewhere. Women who enrolled in this savings product saw a noticeable improvement in their decision-making power within their households, leading to a practical change in the power dynamics at home, such as an increase in purchases of durable goods (e.g., appliances). This demonstrates that well-designed financial products can transcend being mere savings tools and become instruments of ‘Social Empowerment’.

2.4. Case Study: The Debate Over South Korea’s ‘Automatic Enrollment in National Pension for High School Seniors’ Policy

These principles of behavioral economics are now extending beyond individual lives to national policies. The recently discussed ‘Automatic Enrollment in National Pension for High School Seniors’ policy in South Korea is a prime example of a large-scale commitment device or ’nudge’ at the national level.

- Policy Details: This system automatically enrolls all youths turning 18 in the national pension scheme, with the government covering the first month’s insurance premium.

- Policy Goals: To address the coverage gap affecting 53.3% of the youth population aged 18-34 and to maximize the enrollment period to strengthen income security in old age.

- Behavioral Economics Principle: This is an attempt to overcome the ‘status quo bias’ of youths who delay enrollment due to lack of income or interest by setting a strong ‘default’ of ‘automatic enrollment’.

- Controversy: Concerns have been raised about the massive funding required and the potential weakening of a sense of responsibility regarding premium payments. This highlights the sharp tension between respecting individual freedom of choice and the ’nudge’ philosophy of gently intervening for better outcomes for the entire population.

Chapter 3. The Invisible Hand: What Manipulates My Choices

Our choices are manipulated not only by present bias but also by numerous invisible hands. Behavioral economics has uncovered various cognitive biases that distort our judgments. Let’s examine a few.

3.1. Case Study: Food Stamps and ‘Tagged Money’

Traditional economics assumes that ‘money is fungible’. A 10,000 KRW bill should have the same value whether received as salary or found on the street. However, our brains do not think this way. We unconsciously attach tags to money, such as ‘found money’, ‘salary’, ’emergency funds’, and ‘food expenses’, treating them differently. This is known as ‘Mental Accounting’.

Research on SNAP (formerly food stamps), a low-income grocery support program in the U.S., provides strong evidence of mental accounting. Logically, SNAP recipients should integrate the benefits (money) received at the beginning of the month into their monthly budget and use them steadily. However, actual behavior differed. They significantly increased grocery spending at the beginning of the month and reduced consumption as the month progressed, even experiencing extreme ‘consumption cycles’ that led to days of hunger.

The most decisive evidence is that even in households where total grocery spending exceeded SNAP benefits, meaning SNAP benefits could effectively be used like cash, people were much more likely to spend the money received from SNAP on groceries than on cash (marginal propensity to consume). They tagged SNAP benefits as ’this is for food’, leading to irrational choices of overspending on ‘food expenses’ at the beginning of the month and suffering at the end.

3.2. Behavioral Economics in Everyday Life: The Secrets of Popcorn Pricing and the Temptation of Sales

Our choices are also greatly influenced by the ‘frame’ of the information presented and the first ’number (anchor)’ we see.

- Anchoring Effect: When we see a price tag that says “Regular Price 20,000 KRW → Sale Price 18,000 KRW” at a store, we feel it’s a good deal. The initial number ‘20,000 KRW’ serves as an anchor, becoming a reference point for our judgment. In reality, no one knows if the price of 18,000 KRW is reasonable.

- Decoy Effect: Do you know the secret behind popcorn pricing at movie theaters? When small popcorn is 3,000 KRW and large popcorn is 7,000 KRW, we hesitate over which to buy. If the theater introduces a medium popcorn at 6,500 KRW as a ‘decoy’, what happens? Suddenly, the large popcorn seems like an incredible deal and sells like hotcakes. The medium popcorn exists not to be sold but to make the large popcorn appear more attractive, guiding our choices.

- Framing Effect: The statement “90% survival rate after surgery” and “10% mortality rate after surgery” convey the same statistical information. However, most patients feel much more reassured and decide to undergo surgery when they hear the former. The way the same content is framed can lead to a 180-degree shift in our evaluations and choices.

Conclusion: How to Regain Control of My Mind

Through this article, we have examined the principles of behavioral economics hidden in various aspects of our lives, from gym memberships to national pension policies. We are more irrational than we think, swayed by numerous biases, and repeat choices we regret.

However, the important thing is that our irrationality is not random but ‘predictable’. Understanding in what situations we are vulnerable to which biases is the most crucial first step toward making better choices.

Now, instead of blaming our lack of willpower, we can understand the ‘systems’ and ’environments’ that lead us to irrational choices and design them to our advantage. Like Odysseus, we can create commitment devices for ‘future me’ (set up automatic transfers for savings on payday), exploit mental accounting (divide accounts for different goals like travel, celebrations, and emergency funds), and recognize the traps of framing and anchoring cleverly set by marketers.

Behavioral economics does not teach us how to become perfectly rational humans. Instead, it provides the most scientific and realistic guide on how to make slightly more wise and happy choices while embracing our flawed, human selves. It’s time to regain control of the reins of my mind.

References

- [New Year’s Resolutions Crumble as the Alarm Goes Off | Korea Economic Daily | KDI Economic Education and Information Center.](https://eiec.kdi.re.kr/publish/columnView.do?cidx=11389&sel_year=2018&sel_month=01)

- [Behavioral Economics and UX] 1. Behavioral Economics: All About Human Psychology that Moves the Economy - pxd story.

- Minimal Behavioral Economics - Aladin.

- Minimal Behavioral Economics - Yes24.

- DellaVigna, S., & Malmendier, U. (2006). Paying Not to Go to the Gym. American Economic Review, 96(3), 694–719.

- The Relationship Between Intertemporal Choice and Blood Sugar Control in Type 2 Diabetes Patients.

- The Relationship Between Impulsivity and Smartphone Addiction in Adolescents: Exploring the Potential of Delay Discounting Tasks.

- Save More Tomorrow | Chicago Booth Review.

- Thaler, R. H., & Benartzi, S. (2004). Save More Tomorrow™: Using Behavioral Economics to Increase Employee Saving. Journal of Political Economy, 112(S1), S164–S187.

- Ashraf, N., Karlan, D., & Yin, W. (2006). Tying Odysseus to the Mast: Evidence from a Commitment Savings Product in the Philippines. The Quarterly Journal of Economics, 121(2), 635–672.

- Ashraf, N., Karlan, D. S., & Yin, W. (2010). Female Empowerment: Impact of a Commitment Savings Product in the Philippines. World Development, 38(3), 333–344.

- ‘Automatic Enrollment in National Pension for High School Seniors’ Policy Gains Momentum in National Assembly… Lee’s Promise - Munhwa Ilbo.

- Will the Government Cover the Insurance Premiums for High School Seniors?… Expectations for ‘Automatic Enrollment at 18’ in Lee’s Promise.

- Hastings, J., & Shapiro, J. M. (2017). How Are SNAP Benefits Spent? Evidence from a Retail Panel. NBER Working Paper No. 23112.

- Wilde, P., & Ranney, C. (2000). The Monthly Food Stamp Cycle: Shopping Frequency and Food Intake Decisions in an Endogenous Switching Regression Framework. American Journal of Agricultural Economics, 82(1), 200-213.