The society we live in actually runs on an invisible web called ’trust’. A piece of paper money has value because the state guarantees it, and the law works because we have collectively agreed to trust it as ‘justice’. Everything was designed based on trust in third-party guarantors like banks, courts, and states.

But in 2008 — remember? The Lehman Brothers collapse. The world saw firsthand how brittle this human-centered trust system could be.

The ledger is the revolution: entrusting trust to code

The 2008 collapse was not merely a bubble bursting. It was… a collapse of a massive “trust pyramid” composed of complex derivatives, opaque ledgers, and trust institutions that either ignored or encouraged risk.

In the middle of this catastrophic failure, on October 31, 2008, like something out of a movie, an anonymous person (or group) known as Satoshi Nakamoto published a nine-page paper titled “Bitcoin: A Peer-to-Peer Electronic Cash System.” It was the most fundamental answer to the financial crisis.

Think about it: the essence of money is not gold or paper. It’s the ledger — the belief that something is recorded, guaranteed, and exchangeable.

Satoshi’s revolution changed the owner of that ledger. Instead of a central ledger controlled by states or banks, Bitcoin created a “distributed ledger” spread across the world. If traditional ledgers were guaranteed by the “authority” of banks, Bitcoin proves the ledger’s honesty through cryptography and Proof-of-Work, mathematical and physical laws that no one can cheat.

This was a massive paradigm shift that changed the subject of trust from ‘human promises’ to ‘mathematical code’.

Why this is not just a technical innovation but a political manifesto is clear from the message embedded in Bitcoin’s first block, the “Genesis Block”: “The Times 03/Jan/2009 Chancellor on brink of second bailout for banks.” It was almost a declaration of war — like saying, ‘You (the existing financial system) betrayed trust, so I was born.’

Bitcoin introduced a paradoxical concept called ’trustless trust’: you don’t need to trust counterparties or intermediaries; you only need to trust the system’s rules (the code) itself.

- Fixed supply: 21 million. Period. Inflation caused by arbitrary printing like a central bank is impossible.

- Predictable issuance: New coins are issued roughly every 10 minutes as block rewards, halving approximately every four years.

- Censorship resistance: No one can block or reverse a valid transaction. It’s the ultimate protection of property rights.

It was the moment when the old definition “money is a promise of the state” was replaced by a new definition: “money is trust guaranteed by code.”

Programming contracts: Ethereum and new institutions

If Bitcoin created a static order like “immutable digital gold,” Ethereum added a dynamic wing called “programming.” If Bitcoin is digital gold, Ethereum aimed to be a “world computer” where contracts and institutions themselves could be coded.

In 2013, the prodigy Vitalik Buterin proposed the idea of ‘smart contracts’ — literally “smart contracts” that program “If condition A is met, automatically execute B.”

Where traditional contracts required expensive and slow human interventions like lawyers and courts, this is handled by code. If conditions are met — boom! — it executes. And it can’t be reversed.

Thanks to Ethereum, blockchains evolved from simple ledgers into platforms for creating new institutions and organizations.

Blockchain 3.0 and the unsolved puzzle ’the Trilemma’

The ecosystem Ethereum created, especially decentralized finance (DeFi), showed tremendous potential. But it also ran into a major technical challenge: the famous ‘Blockchain Trilemma’.

Blockchains aim to achieve three things simultaneously, but it’s extremely hard to have all three perfectly:

- Decentralization: A fair network not controlled by a few actors. (Measured sometimes by the Nakamoto coefficient — how many actors must collude to cripple the network.)

- Security: How safe it is from hacks.

- Scalability: How fast and cheap (TPS, fees) it can process transactions.

Bitcoin prioritized decentralization and security at the expense of scalability (speed). Ethereum faced similar scaling challenges. To solve this, so-called ‘Blockchain 3.0’ projects like Solana, Avalanche, and Polkadot proposed various solutions.

I analyzed major platforms as of Q3 2025; here’s a table.

Table 1: Comparison of major blockchain platforms (estimated as of Q3 2025)

| Blockchain | Consensus Mechanism | Nakamoto Coefficient (Estimated) | Average TPS (Estimated) | Average Transaction Fee (USD, Estimated) | Key Features |

|---|---|---|---|---|---|

| Bitcoin | PoW | 7 | 3 - 7 | $1 - $5 | Highest security, decentralization, store of value |

| Ethereum | PoS | 2 (Lido+Coinbase) | 15 - 30 | $0.5 - $3 (L2s are cheaper) | Smart contracts, large ecosystem |

| Solana | PoH + PoS | 19 - 21 | 2,000 - 4,000 | $0.00025 | High TPS, low fees, decentralization concerns |

| Avalanche | PoS | ~30 | ~4,500 (subnets) | $0.01 - $0.1 | Subnets, fast finality |

| Polkadot | NPoS | ~90 | ~1,000 (parachains) | $0.01 - $0.1 | Interoperability (IBC), shared security |

| Cardano | PoS | ~24 | ~250 | $0.05 - $0.15 | EUTXO model, academic approach |

| BNB Chain | PoSA | ~20 | ~300 - 500 | $0.01 - $0.05 | Low fees, Binance ecosystem |

Note: These figures are estimates and can vary depending on network conditions, measurement methods, and timing.

This table makes it clear: there is no “best blockchain.” There are only blockchains optimized for specific purposes.

However, this programmability is also the largest source of risk. As code grows complex, bugs and vulnerabilities inevitably appear, and hackers exploit them. Because of this tension, additional trust infrastructure (like insurance or oracles) became necessary to cover code weaknesses.

A marketplace for buying and selling trust: DeFi, insurance, and oracles

The grand experiment enabled by smart contracts is precisely Decentralized Finance (DeFi) — trying to replace traditional financial intermediaries like banks and brokerages with transparent, automated code.

1. Insuring code risk: Nexus Mutual

The biggest Achilles’ heel of smart contracts is ‘code bugs’. To cover this risk emerged decentralized insurance like Nexus Mutual.

Think of it not as a joint-stock company but as a modern mutual aid association.

- Participants pay premiums to create a pooled capital fund.

- If a hack occurs, whether to pay claimants is not decided by a central underwriter but by other members who have staked tokens (NXM) acting as ‘risk assessors’ and voting.

- Honest voting (majority decision) gets rewarded; dishonest voting can forfeit staked tokens. These economic incentives encourage fair adjudication.

If traditional insurance relies on institutions, this is a new model that trusts transparent code and participants’ economic incentives.

2. Connecting to the real world: Chainlink

Smart contracts can run perfectly within the blockchain, but they have a fatal limitation: they cannot natively access real-world data outside the chain.

For example, a smart contract can’t answer, “What’s the current market price of ETH?” This is called the Oracle Problem. If you fetch data from a single centralized server, that server could be hacked or lie, collapsing the system.

This is where Chainlink comes in — a leading decentralized ‘oracle network.’

- It pulls data from multiple paid data providers,

- Many independent node operators worldwide fetch the data,

- The data is aggregated (e.g., averaged) on-chain to deliver a single “trusted value” to smart contracts.

Chainlink is effectively the arterial system of the DeFi ecosystem. Its importance is evident in the metric ‘Total Value Secured (TVS),’ which measures the total value of assets protected by smart contracts that Chainlink secures.

As TVS grows, it implies DeFi has become a substantial system — and here lies an irony. While DeFi champions decentralization, the real-world connection has become heavily dependent on a single standard like Chainlink. Even decentralized systems can exhibit new forms of centralization due to efficiency and network effects.

In the end, ’trust’ is becoming not an abstract belief but a tangible ‘product’ priced by markets and assessed for risk.

A world where everything is connected and tokenized

Now this innovation is expanding beyond blockchains into real-world assets. Two major trends are driving this:

- Multichain: Technologies that enable multiple blockchains to communicate.

- Tokenization: Bringing physical assets like real estate, artwork, and bonds onto blockchains as digital tokens (Real-World Assets, RWAs).

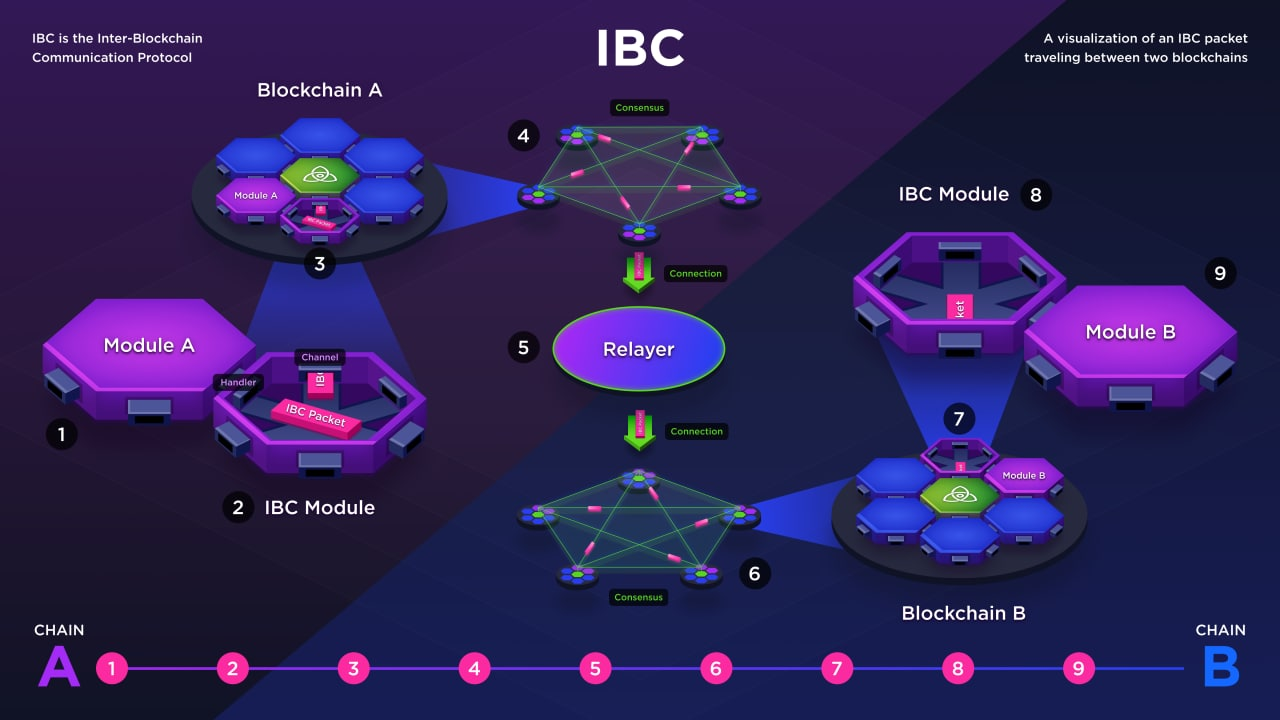

Contrary to ‘Bitcoin maximalism’ (the view that Bitcoin is supreme), the reality is moving toward a multichain world where many blockchains coexist. The core technology enabling this is “the internet of blockchains,” such as Cosmos’ IBC (Inter-Blockchain Communication).

Tokenization tears down the wall between the real world and blockchains. Assets that were hard to divide and sell—like real estate—can be fractioned (tokenized) and traded 24/7 in small units.

This has great potential to unlock ‘dead capital’ in developing countries, where assets exist but lack formal title and can’t be used as collateral. Recording ownership on a blockchain can prove property rights. (Of course, this could also lead to ’elite capture’ or ‘digital colonialism’ if mishandled, so caution is necessary.)

The symbol of traditional finance: BlackRock’s entry

A decisive event showing that tokenization is no longer a distant future was the launch of BlackRock’s BUIDL Fund. The heart of traditional finance began embracing this technology.

Examining the fund’s structure reveals the future.

Table 2: Structure analysis of BlackRock’s BUIDL Fund

| Component | Responsible Party | Role & Technology |

|---|---|---|

| Asset Manager | BlackRock | Fund management and operation |

| Tokenization Platform | Securitize | Issuance of permissioned tokens (BUIDL) on Ethereum |

| Asset Custody | BNY Mellon | Custody of underlying assets (cash, U.S. Treasuries, etc.) |

| Underlying Assets | Cash, short-term U.S. Treasuries, repos | Provide stable collateral for token value |

| Blockchain Network | Ethereum | Token issuance and transaction recording (public blockchain) |

| Core Tech | Permissioned smart contracts | Only approved (KYC-completed) investors allowed to trade |

| Primary Trading Asset | BUIDL (ERC-20 based token) | Digital security representing fund shares |

I believe this clearly demonstrates that the future will likely be a hybrid of traditional finance and decentralized technology, not a pure decentralist revolution. BlackRock takes blockchain efficiency while using permissioned smart contracts to maintain regulatory compliance. That’s the reality.

At the center of all this change are dollar-pegged stablecoins. Interestingly, as private issuers’ dollar stablecoins spread worldwide and these issuers buy U.S. Treasuries as reserves, the dollar’s hegemonic position is actually being reinforced within this new technology.

Conclusion: Why Bitcoin, again?

So, within this complex programmable money ecosystem, what role will the original Bitcoin play?

Paradoxically, Bitcoin’s true value lies in its simplicity and unchanging steadfastness—it does nothing fancy and is obstinately simple.

Bitcoin is not an app in this new digital economy; it is the bedrock that supports everything — the final ’trust anchor.’

The stability of the financial system ultimately depends on ‘pristine collateral.’ In traditional finance, that role is played by U.S. Treasuries. In the digital asset world, the only candidate that can fill that role is Bitcoin.

- Sovereign independence: A neutral asset not owned by any state or company. This trait becomes more valuable amid geopolitical tension.

- Absolute scarcity: Fixed at 21 million. It protects value from unpredictable inflation.

- Top-tier security: Protected by an enormous global hash rate, effectively impossible to attack.

As this programmable money ecosystem grows into the trillions, it will demand the safest, most neutral collateral asset. Bitcoin will become that ultimate guarantee and settlement asset.

A common mistake is to judge Bitcoin only by the limitations of the ‘Bitcoin network’ (slow TPS). That misunderstands Bitcoin’s role. Bitcoin is not a highway; it is the solid ‘bedrock’ beneath everything.

We must distinguish between the ‘Bitcoin network’ and the ‘Bitcoin ecosystem.’

- Bitcoin network: The P2P network that records Bitcoin transactions (slow and limited).

- Bitcoin ecosystem: The sum of all systems that use Bitcoin (BTC) as collateral or store of value (e.g., Lightning Network, WBTC on Ethereum, Bitcoin ETFs, etc.).

From this perspective, the bigger DeFi and tokenization grow, the more demand there will be for the safest and most neutral collateral asset — the primordial ‘base money’ that is Bitcoin.

The success of other blockchains is not Bitcoin’s failure; rather, it strengthens Bitcoin’s value. Bitcoin’s slow, conservative protocol upgrade process is not a flaw; it’s an advantage for being a trust anchor. Foundations must not be flexible; they must be solid and predictable. This extreme minimalism is what makes Bitcoin the eternal reference point and center of order in the ever-changing world of programmable money.

One step further 1 | The blockchain trilemma and each project’s choice

I want to add a bit more on the trilemma because it reflects each blockchain’s philosophy. Since you can’t have (decentralization, security, scalability) all at once, each project made strategic choices.

- Bitcoin’s choice (Security + Decentralization): To become ‘digital gold,’ Bitcoin prioritized security and decentralization over scalability (speed). It’s optimized to store and ultimately settle enormous value.

- Ethereum’s choice (Balanced approach): To be a ‘world computer,’ Ethereum keeps decentralization and security high while trying to solve scalability with layered approaches like layer-2 rollups.

- Solana’s choice (Scalability + Security): Prioritizes massive scalability for high-performance apps. This requires validators with high hardware specs, which sacrifices some decentralization.

In the end, the future is likely not dominated by a single chain. Bitcoin (payments/collateral), Ethereum (general-purpose contracts), and Solana (high-performance apps) may each play distinct roles and interact in a multi-layered ecosystem.

One step further 2 | The philosophy of simplicity: Why does Bitcoin look ‘crude’ but remain robust?

This is a philosophical difference I consider crucial. A system’s nature is revealed by how it responds to crises — especially catastrophic hacks. The 2016 ‘The DAO hack’ showed everything.

That incident brought two core blockchain ideas into direct conflict.

- ‘Code is Law’: Principled. The code recorded on the blockchain is absolute law — even bugs. Humans must not intervene. (Immutability above all.)

- ‘Social Consensus’: Pragmatic. Code is a tool; if a code bug leads to clearly unjust outcomes, the community should correct it by consensus. (Protect majority interests.)

In 2016, The DAO, a large fund on Ethereum, was hacked due to a smart contract vulnerability and a massive amount of funds was drained.

The controversy was that the hacker did not violate Ethereum network rules but simply followed the rules written in The DAO’s code (a bug). Under ‘Code is Law,’ the hacker’s actions could be seen as ’legitimate.’

Ethereum’s community faced a choice:

- Option 1 (Code is Law): Treat the hack as an expensive lesson and preserve immutability.

- Option 2 (Social Consensus): It’s theft; perform a hard fork to revert transactions.

After intense debate, the Ethereum mainstream, including Vitalik Buterin, chose ‘social consensus.’ They performed a hard fork to effectively erase the hack transactions.

That decision created the Ethereum (ETH) we know today.

A minority who insisted “code is law” refused the fork and continued the original chain, becoming ‘Ethereum Classic (ETC).’

Here, Bitcoin’s philosophy stands in contrast. Bitcoin was designed to minimize possibilities for such social interventions. Its protocol is extremely simple, and because it lacks complex smart contract functionality like The DAO, there’s less surface for catastrophic app bugs.

This extreme simplicity and resistance to change — what looks like functional ‘crudeness’ — paradoxically makes Bitcoin a system resilient to social and political pressure.

If Ethereum chose flexibility and adaptability via ‘social consensus,’ Bitcoin chose near ‘Code is Law’ — absolute predictability and immutability.

I believe that uncompromising simplicity and stability are precisely why Bitcoin can serve as the ultimate trust foundation and an unwavering standard of value for the entire programmable money ecosystem.

References

- O Taemin, “There Is No Future Without Bitcoin”

- O Taemin, “Bitcoin and the Geopolitics of the Dollar”

- ASSESSING THE POTENTIAL OF DECENTRALISED FINANCE AND BLOCKCHAIN TECHNOLOGY IN INSURANCE (The Geneva Association)

- Utility at a cost: Assessing the risks of blockchain oracles (S&P Global)

- Unlocking the Dead Capital (World Bank)

- The DAO Attack - Infographic (Deloitte Ireland)

- What Is Blockchain? (IBM)

- Bitcoin and Blockchain: Revolutionizing Industries Beyond Finance - Canada (Leyton)

- Smart Contracts Real Estate (Hedera)

- Smart Contracts in Real Estate 2024: Ultimate Guide Benefits & Future (Rapid Innovation)

- Smart Contract Examples: How Businesses Use Blockchain in the Real World (ilink)

- Blockchain Trilemma. (ResearchGate)

- What is the Blockchain Trilemma and How to Solve It? (MoonPay)

- The Blockchain Trilemma: A Formal Proof of the Inherent Trade-Offs… (MDPI)

- Blockchain Trilemma: What Is It? (Trakx)

- Nakamoto Coefficient: A Key Metric for Measuring Blockchain Decentralization (Gate.com)

- Nakamoto Coefficient Explained: How Decentralized Are Blockchain Networks (CCN.com)

- Fastest Blockchains by TPS [2025] (Chainspect)

- Most Decentralized Blockchains by Nakamoto Coefficient [2025] (Chainspect)

- Which Blockchain Has the Lowest Fees in 2025? Full Comparison (Bleap)

- DeFi in Insurance: Revolutionary Guide to Decentralized Coverage (Rapid Innovation)

- Decentralized insurance in DEX development explained (Nadcab Labs)

- Create a DeFi Insurance Protocol Like Nexus Mutual (Blockchain App Factory)

- The Oracle Problem and Chainlink (Medium)

- The Blockchain Oracle Problem (Chainlink)

- How the Chainlink Oracle Network is Revolutionizing DeFi… (OKX)

- What is Blockchain Oracle Problem and how Chainlink solves it? (Rejolut)

- What Is an Oracle in Blockchain? » Explained (Chainlink)

- Chainlink’s total value secured has surpassed $100 billion (Mitrade)

- Chainlink Reaches an All-time High in Total Value Secured (TVS), Securing $100B in DeFi (Cryptoninjase)

- Chainlink hits new all-time high of $100b in Total Value Secured (Bitget News)

- What is IBC? (Cosmos Developer Portal)

- Deep Dive into Cosmos Inter Blockchain Communication Protocol - IBC (Bcas Blog)

- What is IBC? — Interchain Stack Highlights (The Interchain Foundation, Medium)

- Inter-Blockchain Communication (IBC) protocol, explained (Cointelegraph)

- The Benefits, Risks, and Technology Stack in Tokenizing Real-World Assets (Mike Vitez, Medium)

- Real-World Assets (RWAs) Explained (Chainlink)

- Tokenization of Real-World Assets: Opportunities, Challenges and the Path Ahead (Katten)

- Tokenized Natural Capital Investments in Developing Economies … (PRISM)

- What Is BlackRock’s BUIDL Fund? A Beginner’s Guide To Tokenized Money Markets (CCN.com)

- What is BlackRock’s BUIDL? Everything you need to know… (Slobodzeanb, Satoshi Club, Medium)

- In-Depth Analysis of BlackRock’s BUIDL Fund and Its Impact… (Binance)

- ETC Proof of Work Course: 26. POS Social Consensus vs POW Code Is Law (Ethereum Classic)

- Code, Law, and the Nature of Consensus (Build Blockchain Tech)

- The DAO (Wikipedia)

- What Was the DAO Hack? (Gemini)

- A History of ‘The DAO’ Hack (CoinMarketCap)

- Reentrancy Attacks and The DAO Hack Explained (Chainlink Blog)

- The DAO Hack Provides Lessons for Companies Using Blockchain… (Crowell & Moring LLP)

- O Taemin professor: “Bitcoin will change the dollar order… In the middle of a bull market, premature investment is dangerous” (Mobile Hankyung)

- O Taemin CEO: “All finance will be tokenized… Competition to accumulate Bitcoin could begin in earnest” [Herald Money Festa 2025] (Daum)

- O Taemin | Business & Economics Author - Yes24