We spend money every day. From a cup of coffee in the morning, transportation costs on the way to work, lunch, to grocery shopping in the evening. Money is like the air we breathe, present in almost every moment of our lives. But how much do we really know about this familiar concept of money? What if one morning, the coffee that cost 5,000 won yesterday suddenly costs 10,000 won, and the next day it costs 20,000 won? And yet, our salary remains the same. This is the work of ‘inflation’, a thief that quietly steals the value of the money in our wallets.

This article is a long journey exploring the grand history surrounding money, from its birth to the emergence of the monster called inflation, and the new currency wars of the digital age. Through fascinating stories and examples, we delve into the essence of money and the history of its betrayal, from the tricks of ancient Roman emperors to Zimbabwe’s 100 trillion dollar bill. By the end of this journey, you will see the paper and numbers in your wallet in a completely different light.

Part I: How Did Money Come to Be?

Have you ever imagined a world without money? Would everything be simpler and more romantic than it is now? Absolutely not. It would likely be a much more tiring and inefficient world. Money is one of humanity’s greatest inventions. To understand why, we must take a time travel back to the world before money was born.

1.1. Barter: The Exhausting Start of Trade

Once upon a time, there was a very diligent farmer. He took a cherished cow to the market. His goal was modest: to exchange it for a few loaves of bread, a handful of salt, and a new pair of shoes to replace his old ones. However, the market did not operate as he had hoped. The baker said, “One cow is too much. I only need a chicken…” The salt merchant replied, “I can give you salt, but I need firewood right now.” The shoemaker exclaimed, “What a fine cow! But my wife wants fish,” shaking his head.

The farmer let out a deep sigh. This was the biggest problem of the barter era, known as the ‘double coincidence of wants’. For a trade to occur, the person who has what I want must also want what I have, a very tricky condition. Eventually, the farmer embarked on a challenging journey. First, he sold the cow to someone who wanted firewood and obtained firewood. With that firewood, he went to the salt merchant to get salt, and after finding another person to trade the remaining firewood for fish, he finally went to the shoemaker to get shoes. The farmer, who wandered the market all day, was utterly exhausted. This process clearly illustrates other issues with barter.

- Indivisibility: You cannot cut a living cow into pieces worth just a loaf of bread.

- Lack of a Standard Value: How much is one cow worth in terms of bread? Each time a trade occurred, this standard had to be negotiated anew.

- Portability and Storage Issues: The farmer had to drag a heavy cow around, uncertain if a trade would even happen, and if the baker suddenly accepted the cow, he would have had trouble storing it without a barn.

Thus, barter was incredibly tiring and inefficient. Humanity had to find a better way to solve this inconvenience.

1.2. If Everything Could Be Money

Amid the inconveniences of barter, humanity found the first solution: using a ‘universally desired item’ as an intermediary for exchange. This marked the beginning of ‘commodity money’. Throughout history, a variety of items have served as money. In agricultural societies, grains like rice or wheat, or livestock played this role. As the story goes, Roman soldiers were sometimes paid in salt (salary), which was also a great currency due to its durability and necessity.

Among these, the most successful commodity money was ‘shells’. Due to their rarity, durability, and small size, they were widely used in various civilizations, including ancient China. The Chinese character for money or wealth, ‘貝’, is modeled after the shape of these shells, indicating how deeply commodity money is embedded in our history.

The emergence of commodity money allows us to naturally understand the three core functions that money must fulfill:

- Medium of Exchange: Acts as an intermediary that eliminates the inconveniences of barter.

- Unit of Account: A standard for expressing the value of all items. For example, “This cow is worth 10 bags of rice.”

- Store of Value: The ability to hold value over time.

However, commodity money was not perfect either. Grains could rot, livestock could get sick and die, and salt could dissolve in water. The thirst for better money continued.

1.3. The Allure of Shiny Things: The Rise of Metal Money

To overcome the limitations of commodity money, metals like gold, silver, copper, and iron emerged. Metals solved almost all the shortcomings of commodity money.

- Durability: They do not rot or change, allowing for permanent storage of value.

- Divisibility: They could be melted down and divided into smaller units without losing value.

- Portability: They could hold high value with small volume and weight.

- Homogeneity: Any gold of the same purity had the same value, regardless of its origin.

The early metal money was ‘weight-based currency’, meaning money was used based on weight. During transactions, a metal piece was placed on a scale to measure its weight and calculate its value. Examples include the knife-shaped ‘mingdao qian’ and the plow-shaped ‘pu qian’ used in ancient China. Such Chinese currency has also been found in the ancient sites of Korea, indicating that there was active trade between the Korean Peninsula and China long ago. In Korea, records show that during the Gaya period, iron ingots were used like currency.

1.4. The Token of Trust: The Invention of Coins

As weighing each transaction became cumbersome, humanity made the most innovative invention in the history of money: ‘coins’. Around 650 BC, the Kingdom of Lydia, located in present-day Turkey, is said to have minted the world’s first coins from a natural alloy of gold and silver called ’electrum’. The key to these coins was not merely the shaping of the metal but the ‘royal seal’ stamped on them.

This seal was a promise from the state that guaranteed the weight and purity of the coin. People no longer needed to carry scales; they only had to count the number of coins. The speed and trust in transactions increased exponentially, and commerce flourished. However, at this point, humanity opened Pandora’s box. The moment the state guaranteed the value of money, it gained the powerful ability to deceive that value. The royal seal became a symbol of trust, but it also became a tool that would later give birth to the monster called ‘inflation’. The history of money is a record of both building trust and how that trust has been betrayed and exploited. The evolution of money is a process of gradually outsourcing trust from personal relationships to external authorities. In barter, trust was needed only between the two parties involved in the transaction, but commodity money required society as a whole to believe in the value of a specific item. The advent of coins concentrated that trust in a single entity: the state. This ‘outsourcing of trust’ enabled the emergence of a massive economy but also harbored a fatal weakness: when the state betrays that trust, society as a whole can collapse.

Summary of the History of Money

| Era | Form of Money | Key Features |

|---|---|---|

| Prehistoric | Barter | Requires double coincidence of wants, transaction inefficiency |

| ~B.C. 3000 | Commodity Money | Shells, grains, etc. Issues of decay and storage |

| ~B.C. 1000 | Metallic Money | Chinese dao qian/pu qian, used by weight |

| ~B.C. 650 | First Coins | Kingdom of Lydia, state guarantees weight and purity |

| ~11th Century | First Paper Money | Song Dynasty in China, derived from metal storage certificates |

| 17th Century | First Banknotes in Europe | Issued in Sweden, solving the inconveniences of metallic money |

| 1971 | End of the Gold Standard (Fiat Era) | Nixon Shock, the era of credit money disconnected from gold |

| 2009 | Birth of Bitcoin | The first digital currency operating without government |

| 2020s | Stablecoins & CBDC | New evolution of digital currency: value stabilization, digitalization of central banks |

***

Part II: The Birth of the Monster Called Inflation

The invention of coins advanced commerce but also opened a dangerous door of temptation for rulers. When they needed funds for war or wanted to build lavish palaces, raising taxes would provoke fierce backlash from the populace. However, secretly increasing the amount of cheap metal mixed into coins was a much easier and more discreet method. This marked the beginning of state-led inflation, or ’the betrayal of money’.

2.1. The Copper-Nosed Roman Emperors

Our first case begins in the vast commercial empire of Rome. In 64 AD, a terrible fire devastated Rome, turning much of the city to ashes, and Emperor Nero devised a grand plan for the reconstruction of Rome. However, he lacked the funds to cover the enormous reconstruction costs and his own lavish lifestyle.

At this point, Nero came up with a cunning scheme: ‘debasement of currency’. He secretly ordered the mint to reduce the silver content in the silver coin ‘denarius’ and to mix in more cheap copper. Thus, coins were born that looked similar on the outside but had diminished actual value. Legally, they still held the same value as the old silver coins. Nero paid his soldiers with this ‘fake money’ and settled the costs of the reconstruction project. He effectively printed more money with the same amount of silver.

This news quickly spread through the market. Clever Roman citizens began to hide the old high-purity silver coins deep in their cupboards and hurriedly used only the new coins with diminished value. This phenomenon, where only poor-quality money flooded the market while good money disappeared, is famously known as “bad money drives out good”, or ‘Gresham’s Law’.

Nero’s trick was just the beginning. Many Roman emperors followed this method whenever they faced financial difficulties. Over time, the silver content of the denarius continued to decline, and by the mid-3rd century, it had fallen to less than 5% silver content, effectively becoming a copper coin merely coated with silver.

The consequences were dire. As the value of currency continued to plummet, prices skyrocketed. A murderous inflation engulfed the Roman economy. People no longer trusted coins, and taxes began to be paid in goods like grain or cloth instead of coins. The monetary economy collapsed, regressing back to the barter system. In 301 AD, Emperor Diocletian issued the ‘Edict on Maximum Prices’, setting price ceilings for all goods and services, but the result was even worse. Merchants preferred to hide goods rather than sell at a loss, and the black market thrived. Ultimately, this policy failed, and the distrust in the monetary system and economic chaos became one of the many causes of the fall of the Western Roman Empire.

2.2. The King’s Debt, The Kingdom’s Pain: Henry VIII’s ‘Great Debasement’

Now, let’s leap forward to 16th-century England. Famous for his six wives and the establishment of the Church of England, Henry VIII frequently waged wars against France and Scotland and was always short on money to maintain his lavish court life. He dissolved monasteries to seize their wealth, but it was still not enough.

Ultimately, Henry VIII chose the same method as the Roman emperors. Starting in 1544, he initiated a massive currency debasement policy known as ‘The Great Debasement’. He reduced the silver content of coins from 92.5% to just 25%.

The coins produced during this time earned Henry VIII the infamous nickname ‘Old Coppernose’. The new coins were made of copper and only thinly coated with silver, and as the coins wore down, the first part to wear off was the silver on the king’s portrait, revealing the copper underneath. The populace had to witness the diminishing value of their currency every day as they looked at the king’s copper nose on the coins they held.

The results were the same as in Rome. Prices skyrocketed, the economy fell into chaos, and the credibility of English currency plummeted across the European continent. Merchants had to weigh English coins each time they conducted transactions.

However, there is a hopeful twist in this story. When Henry VIII’s daughter, Elizabeth I, ascended to the throne, she prioritized restoring the collapsed currency system. In 1560, Elizabeth I launched a major currency reform, recalling all the inferior coins in circulation and issuing new high-purity silver coins. This difficult decision, which incurred enormous costs, restored trust in English currency and laid a solid foundation for England’s future growth as an economic power. This case illustrates that restoring trust in a collapsed currency goes beyond mere economic policy; it is a political decision that can determine the fate of a nation. When a ruler shows the will to restore trust, the economy can finally regain stability.

2.3. Overflowing Silver, Exploding Prices: The Price Revolution of the 16th Century

So far, we have seen examples of rulers creating ‘bad money’ to induce inflation. But could inflation also occur if ‘good money’ suddenly became too abundant? The 16th century in Europe was a massive laboratory for this phenomenon. After Columbus’s discovery of the Americas at the end of the 15th century, Spanish conquistadors discovered massive mines like the Potosí silver mine in Bolivia and began transporting enormous amounts of gold and silver to Europe. These precious metals spread throughout Europe via Spain, leading to an explosive increase in the money supply.

As a result, 16th-century Europe experienced a ‘Price Revolution’, where prices continuously rose for about 150 years. In some regions, prices soared sixfold. For people at the time, this was a bizarre phenomenon they had never encountered before, as prices had remained relatively stable for centuries. This historical event teaches us another important cause of inflation: the basic principle of the ‘Quantity Theory of Money’. Simply put, “If the amount of money (M) circulating in the market increases much faster than the amount of goods and services (T) that can be purchased, prices (P) will inevitably rise.” In 16th-century Europe, the influx of silver from the Americas rapidly increased the money supply, but agricultural productivity and the production of manufactured goods could not keep pace. Ultimately, the situation of overflowing money chasing limited goods led to rising prices across the board.

Thus, inflation can arise not only from the intentional deceit of rulers but also from imbalances between the money supply and production in the entire economic system. While the cases of Rome and Henry VIII were artificially induced inflation due to ‘financial needs’ like war, the Price Revolution reaffirms the historical pattern that the needs of states to fund wars can also lead to inflation. Wars demand enormous costs, raising taxes is politically risky, and lowering the quality of money seems to be the easiest solution for rulers. The phenomenon of Roman soldiers losing the value of their wages and English merchants’ currency being distrusted abroad is a recurring tragedy that occurs when states transfer their financial crises onto the savings of their citizens, transcending time and place.

***

Part III: The Age of Paper: Promises, Problems, and Chaos

Metal money was heavy and inconvenient. Especially for large transactions, one had to transport coins in carts. This inconvenience led to yet another revolution in the history of money: the birth of ‘paper money’. This light and convenient invention advanced commerce to a new level but also unleashed the monster of inflation on an unprecedented scale.

3.1. The Invention of ‘Flying Money’

The birthplace of paper money is surprisingly not Europe but 11th-century China during the Song Dynasty. At that time, merchants in the Sichuan region faced significant difficulties trading heavy iron coins in bulk. To buy a single silk roll, they had to pay with 130 jin (about 80 kg) of iron coins.

To solve this problem, merchants began to entrust their iron coins to a trustworthy guild and received paper receipts as proof. These receipts became the world’s first banknotes, known as ‘jiaozi’. People traded using the lightweight jiaozi instead of heavy iron coins, and whenever they needed, they could exchange the jiaozi for iron coins. In other words, the value of jiaozi was based on the ‘promise that it could always be exchanged for metal money’. This is the core principle of ‘convertible currency’.

This convenient invention was soon adopted as official currency by the government and later shocked and amazed Westerners like Marco Polo during the Yuan Dynasty. In Europe, a similar need led to the first appearance of banknotes in Sweden in the 17th century, much later than in China.

3.2. The Hell of Hyperinflation

The era of convertible currency was peaceful as long as the ‘promise’ was kept. But what happens when the government breaks that promise and starts printing far more paper money than the gold or silver it holds? Hell opens up. This leads to ‘hyperinflation’, where prices skyrocket uncontrollably. History vividly shows us horrific examples of this.

Case Study 1: The Tears of the Weimar Republic (1921-1923)

After losing World War I, Germany’s Weimar Republic had to pay astronomical reparations to the victorious nations. To make matters worse, when France and Belgium occupied the Ruhr region, Germany’s industrial heartland, citing delays in reparations, the German government instructed workers to engage in ‘passive resistance’, or strikes, and promised to pay their wages.

With tax revenues cut off and expenditures rising, the only option left for the German government was to turn on the printing presses and print money. This was the ‘monetization of debt’, paying off debts with newly printed money.

The result was recorded as one of the worst economic disasters in human history.

- Unimaginable Price Increases: The price of a newspaper that cost 0.3 marks in 1921 skyrocketed to 70 million marks by November 1922, an increase of over 200 million times.

- Value of Money Vanished: People received their wages twice a day and rushed to stores to hoard goods, as money would turn into worthless paper within hours. People transported bundles of cash in carts, and banknotes became cheaper than wallpaper or firewood, leading to their actual use as such.

- Collapse of the Middle Class: The savings and pensions accumulated over a lifetime became worthless overnight, completely collapsing Germany’s middle class. The despair and anger of these individuals drove society to extremes, ultimately creating fertile ground for Hitler and the Nazi Party to rise.

This hellish chaos finally ceased in November 1923 with the introduction of a new currency called the ‘Rentenmark’. Lacking gold, Germany issued Rentenmarks backed by all state land and industrial assets while completely halting the printing of money. This dramatic case illustrates that the value of currency ultimately lies in ’trust’, known as the ‘miracle of the Rentenmark’.

Case Study 2: The Worst Inflations in History

The tragedy of the Weimar Republic was not an isolated case. History has recorded even more horrific instances.

- Hungary (1946): After World War II, Hungary experienced the fastest hyperinflation in history. Prices doubled every 15 hours, and the government even issued banknotes with 20 zeros attached. The causes were similar to those of Weimar: destruction from war, enormous reparations, and the government’s reckless printing of money. Hungary also introduced a new currency called the ‘forint’ and stabilized the economy through a return to the gold standard.

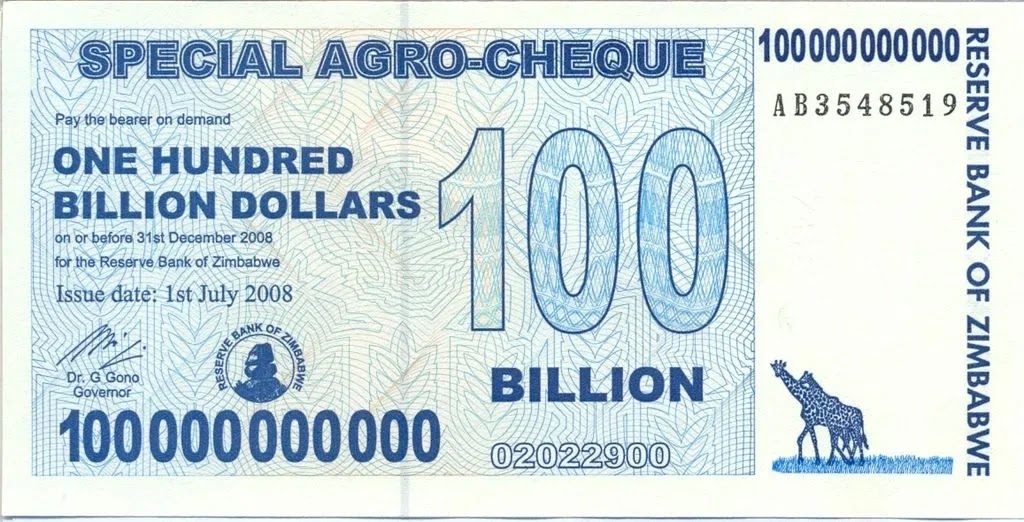

- Zimbabwe (2000s): The most recent tragic example. Due to the dictatorship of President Robert Mugabe and failed land reform policies, agricultural production collapsed, and the government printed money to cover the budget deficit. As a result, the 100 trillion Zimbabwe dollar bill emerged, but this money could barely buy a few eggs. Bus fares varied between morning and evening, and people abandoned their national currency in favor of the US dollar. Ultimately, in 2009, the Zimbabwean government declared the abandonment of its currency and accepted the US dollar as its official currency.

Case Study 3: The Lesson from Joseon, the Dongbaekjeon (1866)

These lessons do not need to be sought far away. In 19th-century Joseon, Heungseon Daewongun pushed for the massive project of rebuilding Gyeongbokgung Palace, which had burned down during the Imjin War. To cover the enormous costs, he issued a new currency called ‘Dongbaekjeon’. As the name suggests, it was a high-denomination currency worth 100 times the existing Sangpyeong Tongbo. However, the actual copper content was only about 5-6 times.

The results were as expected. People hid the high-value Sangpyeong Tongbo and only used the low-value Dongbaekjeon (Gresham’s Law), and as money flooded the market, prices skyrocketed. Within just two years of issuing Dongbaekjeon, the price of rice soared sixfold. Faced with extreme chaos and public outrage, the Daewongun ultimately had to ban the circulation of Dongbaekjeon within six months.

Comparison of Hyperinflation

| Category | Weimar Republic (Germany) | Hungary | Zimbabwe |

|---|---|---|---|

| Period | 1921-1923 | 1945-1946 | 2007-2009 |

| Monthly Peak Inflation Rate | 29,500% | 4.19 x 10¹⁶% | 7.96 x 10¹⁰% |

| Time to Double Prices | 3.7 days | 15 hours | 24.7 hours |

| Highest Denomination | 100 trillion marks | 1 he (10²⁰) pengő | 100 trillion dollars |

| Main Causes | War reparations, fiscal deficit | War damage, reparations | Political failure, fiscal deficit |

Hyperinflation is not merely an economic phenomenon of rising prices. It is a disaster that destroys the entire trust system of society. When money becomes worthless, people abandon savings, become unable to plan for the future, and society begins to distrust one another. In Hungary, people returned to bartering, bringing coats or boots to the countryside to exchange for wheat. There were even absurd situations where the basket itself was more expensive than the money inside it, leading robbers to steal only the basket while leaving the money behind. This painful lesson illustrates how primitive society can regress when the state, which should guarantee the value of money, completely betrays that promise.

***

Part IV: The Maze of the Modern Financial System

After experiencing two world wars and horrific hyperinflation, the world craved a more stable monetary system. The result was the birth of the complex modern financial system we live in today. However, this system is also not free from the long-standing problem of inflation. Through a complete separation from gold, and new challenges like stagflation and pandemics, the history of money is entering another phase.

4.1. The Separation from Gold: The Nixon Shock and the Era of Credit Money

In 1944, after World War II, representatives of the Allied nations gathered in Bretton Woods, New Hampshire, to discuss a new world economic order. The core of this system was to peg the US dollar to gold (1 ounce of gold = 35 dollars) and have other countries’ currencies pegged to the US dollar. In other words, the world was indirectly tied to the gold standard through the dollar.

This system seemed to work well for a while. However, in the 1960s, as the US printed far more dollars than it had gold reserves to back, doubts about the dollar’s value began to arise. Countries like France and the UK started demanding to exchange their dollars for gold, quickly depleting the US’s gold reserves.

Ultimately, on August 15, 1971, President Richard Nixon made a bombshell announcement: the US would no longer exchange dollars for gold. This was the ‘Nixon Shock’. With this declaration, the link between the dollar and gold was severed, leading to the collapse of the Bretton Woods system.

This event marked one of the most significant turning points in the history of money. Humanity’s currency was completely freed from the shackles of physical assets like gold, relying solely on the ’trust’ and ‘promises’ of the issuing government. This moment marked the official beginning of the ‘fiat money’ era, or the era of credit money. All the money we use today is this credit money. Its value does not reside in the paper or numbers themselves but depends on our ‘belief’ that the government and central banks will maintain that value stably. When that belief is shattered, we have already seen that the tragedy of the Weimar Republic can be repeated at any time.

4.2. Stagnant Growth, Soaring Prices: Stagflation of the 1970s

With the severing of ties to gold in the 1970s, the world economy faced a new type of crisis never experienced before. The worst combination of stagnant growth, soaring unemployment, and rising prices emerged, known as ‘stagflation’. This phenomenon was difficult to explain with mainstream economic theories of the time.

The primary cause was an external shock, namely a ‘supply shock’. In 1973, when the Fourth Middle Eastern War broke out, the Organization of the Petroleum Exporting Countries (OPEC) weaponized oil, quadrupling oil prices and reducing exports. As the price of oil, the lifeblood of global industry, skyrocketed, production costs in factories and transportation costs for trucks surged. This triggered ‘cost-push inflation’, forcing companies to raise product prices.

This was fundamentally different from ‘demand-pull inflation’, where prices rise due to excess demand, as seen in the Price Revolution. If the government tried to inject money to stimulate the economy, prices would soar even higher, and if it tightened the money supply to control prices, the economy would freeze further, creating a no-win situation.

The person who ended this long nightmare was Paul Volcker, who became the Chairman of the Federal Reserve in 1979. He determined that the ’expectations of inflation’ had to be broken and took the drastic step of raising the interest rate to a staggering 20%. This was the ‘Volcker Shock’. This shock plunged the US economy into a deep recession and caused a surge in unemployment, but it ultimately succeeded in taming the persistent flames of inflation. Volcker’s decision was a historical event that demonstrated that the most crucial mission of central banks in the era of credit money is to maintain ’trust in price stability’, and that sometimes, enormous costs must be paid to uphold that trust.

4.3. Aftermath of the Pandemic: The Inflation Debate of 2021-2023

Most recently, we all experienced the inflation brought on by the pandemic. It was like a giant economic mystery drama. Who was the culprit?

- Suspect #1: Supply Chain Chaos. In 2020, when COVID-19 swept the globe, factories shut down and ports were closed. This paralyzed the global supply chain for producing and transporting goods. As it became harder to obtain items, prices began to rise. The 2022 invasion of Ukraine by Russia further exacerbated this by driving up energy and grain prices.

- Suspect #2: The Tsunami of Money. To revive the economy that had come to a halt due to the pandemic, governments around the world unleashed massive amounts of money. The US distributed disaster relief payments to all citizens, and central banks lowered interest rates to near zero, flooding the market with liquidity. This influx of money flowed into consumers’ pockets, creating strong demand.

Who is the culprit? Intense debates erupted among economists. The ’transitory inflation’ camp argued that once the supply chain issues were resolved, prices would stabilize on their own, while the ‘permanent inflation’ camp contended that the problem stemmed from the government injecting too much money, necessitating strong tightening measures.

In conclusion, there was not just one culprit. It was a ‘complex crime’ where strong demand (the tsunami of money) overwhelmed a paralyzed supply chain. The money injected during the 2008 financial crisis remained in the banking system, inflating asset prices like stocks or real estate, creating ‘asset inflation’. However, the money released during the pandemic directly entered people’s pockets, triggering ‘consumer price inflation’ that pushed up the prices of goods and services we buy daily, highlighting a fundamental difference. This experience once again demonstrated how complex and unpredictable the modern financial system can be.

***

Part V: Where Is Your Wallet Going?

From the Roman denarius to the digital codes of the 21st century, money has continuously evolved. Now, we stand at a significant turning point where the era of government and central bank monopoly over currency issuance is waning, and new technologies challenge that dominance. The rebellion of cryptocurrencies, the counterattack of central banks, and the new threats of inflation we will face. What will the future of money look like? And where will our wallets head?

5.1. The Rebellion of the Digital Age: Cryptocurrencies

In 2008, the global financial crisis led to deep distrust in the existing financial system. Amid this chaos, an anonymous programmer named Satoshi Nakamoto introduced Bitcoin to the world. Bitcoin was the first decentralized digital currency that operated solely on cryptographic technology without central administrators like governments or central banks. This signaled the emergence of a new monetary system based on the ‘proof’ of code rather than the ’trust’ of the state.

Could It Be a Refuge from Inflation?

Bitcoin supporters argue that Bitcoin, with a fixed total supply of 21 million coins, could serve as an alternative to fiat currencies that can be printed infinitely, essentially becoming ‘digital gold’. They hope that when the value of currency declines due to government mismanagement, Bitcoin can protect their assets.

However, the reality is complex. Due to extreme price volatility, Bitcoin is still insufficient as a stable store of value or medium of exchange. It is difficult to use a currency that might allow you to buy a car today but only a bicycle tomorrow in everyday life.

Lessons from Real Cases

- El Salvador’s Experiment: In 2021, El Salvador embarked on a bold experiment by becoming the first country to adopt Bitcoin as legal tender. However, the results were not entirely positive. The majority of the population was unfamiliar with using Bitcoin, and due to technical issues, distrust in the government, and extreme price volatility, actual usage rates remained very low. For the impoverished, Bitcoin, which could lose half its value overnight, was too risky to receive as a salary.

- Choices in Argentina and Turkey: In contrast, in Argentina and Turkey, where national currencies are collapsing under severe inflation, the situation is different. Citizens in these countries are desperately turning to cryptocurrencies to protect their assets. Particularly, they are opting for ‘stablecoins’ like USDT or USDC, which are pegged to the US dollar, as a means of escaping their depreciating national currencies. This phenomenon represents a modern version of Gresham’s Law unfolding in the digital realm.

5.2. The Counterattack of Central Banks: The Emergence of CBDCs

Faced with the challenge of cryptocurrencies, governments and central banks are not sitting idly by. Their response is the ‘Central Bank Digital Currency (CBDC)’. CBDC is essentially a digital form of legal tender issued directly by central banks.

Advantages and Concerns

CBDCs can reduce the costs of issuing and managing cash, make payment systems more efficient, and provide easier access to the financial system for unbanked individuals.

However, there are significant concerns that CBDCs could grant unprecedented power to central banks. For example, the government could directly deposit disaster relief payments into every citizen’s CBDC account, and during economic downturns, it could impose ’negative interest rates’ on people’s savings to force them to spend. Additionally, since all transaction records would be stored on central bank servers, serious privacy issues arise, as the state could monitor all individuals’ economic activities.

5.3. New Challenges of the 21st Century

Future inflation will be influenced not only by technological changes like cryptocurrencies or CBDCs but also by larger structural changes.

- Deglobalization: For decades, we enjoyed low prices thanks to cheap goods produced in places like China. However, through the US-China conflict and the pandemic, the trend of ‘deglobalization’ or ‘slowbalization’ that prioritizes security over efficiency is gaining strength. As production bases return to home countries or neighboring nations, production costs rise, which can exert long-term upward pressure on prices.

- Greenflation: The ‘green transition’ to combat climate change can also become a new inflation factor. The demand for essential minerals like lithium and nickel for electric vehicle batteries, or copper for renewable energy facilities, is surging, but supply cannot keep up, leading to skyrocketing prices. The costs incurred in the transition to a green economy manifest as rising prices.

- Demographic Changes: Aging populations also impact inflation. The labor force participating in production decreases (wage pressure), while the elderly population spending their savings increases (demand for consumption). This can lead to both labor shortages and increased demand, pushing prices up in the long term.

***

Conclusion: Ultimately, It’s All About Trust

From shells to metal coins, through paper currency to invisible digital codes, the form of money has constantly changed. However, one core value has remained unchanged throughout this long journey: ’trust’.

We believed in the intrinsic value of goods, in the royal seal, and in the government’s promise to exchange for gold. Today, we navigate our economic lives based solely on the invisible belief that the government and central banks will maintain the value of currency stably.

Inflation is the most evident symptom that arises when that trust is shaken or broken. In the face of rulers’ greed, the madness of war, political incompetence, or unpredictable disasters, money has always been ready to betray us. History constantly reminds us that the value of money is never eternal or absolute.

Now, we stand on the threshold of another significant transition. Bitcoin calls for trust in algorithms instead of states, while CBDCs claim to solidify that trust in the digital realm. Deglobalization, climate change, and demographic aging are shaking the economic laws we once knew.

In this chaotic era, where is your wallet heading? And what or who will you trust? That choice will determine your future wealth.

Sources

- [Barter (r83 edition) - Namu Wiki](https://namu.wiki/w/%EB%AC%BC%EB%AC%BC%EA%B5%90%ED%99%98?rev=83)

- Barter: From Barter to Modern Money: The Evolution of Exchange Medium - FasterCapital

- Please Pay with This! | Click Economic Education | KDI Economic Education and Information Center

- Barter - Namu Wiki

- From Barter to Bitcoin: The History and Future of Money - Mobile Hankyung

- The Background of the Transition from Metallic Money to Paper Money - Weekly Chosun

- The History of Money - YouTube

- The History of Money - Brunch

- While Playing with History: The Role of Money in Economic Activity - Our History Net

- From Stones, Salt, and Gold Coins to Electronic Money… Money Transforms - Sgsg

- History of Money - Wikipedia

- KEEP!T History: The Characteristics of Money through the Emergence of Coinage - Steemit

- Ancient Metallic Currency - Our History Net

- The History of Our Currency - Seongju Newspaper

- How Does the Economy Work? - The Role of Money

- [Economic Review in History] Roman Currency Reform, Inflation, and Decline

- The Meeting of Humanities and Economics 114: The Cause of the Fall of the Roman Empire is China

- Atlas News

- Gresham’s Law - Namu Wiki

- Ancient Roman Currency - Wikipedia

- One of Diocletian’s largest failures is thought to be the Edict of Prices. - Reddit

- Document 7.1: Diocletian’s Edict on Maximum Prices and Wages

- Edict of Diocletian on Maximum Prices from 301 CE - IMPERIUM ROMANUM

- The Great Debasement - Wikipedia

- ‘Old Coppernose’: Henry VIII and the Great Debasement - History Hit

- Debasement - TudorHistory.org

- The Inexorable Lessons of Currency Debasement - Institute of Economic Affairs

- Hong Seung-yong’s Maritime Strategy… (19) Queen Elizabeth I, Who Made Europe the Strongest Country with Maritime Power - Weekly Hankyung

- Naughty money: clippers and coiners in 16th-century England | University of Cambridge

- Elizabeth I and the Great Debasement

- Elizabeth I 1558 - 1603 - Coincraft.com

- Elizabeth I - Namu Wiki

- s-space.snu.ac.kr

- Inflation⑤…The Disaster of Gold and Silver from the New World - Atlas News

- Can the Price Revolution of the 16th Century Be Viewed as Inflation? | Click Economic Education

- Professor No Taek-seon’s Historical Economics Price Revolution 2… The Price Revolution and the Industrial Revolution are Inevitable - Sgsg

- Economic Principles Walkthrough Early Paper Money Widely Used in Exchange for Gold - Sgsg

- [Learning History with Curiosity] The History of Money (4) - VOA Korean

- ko.wikipedia.org

- 100 Years Ago Today: The End of German Hyperinflation | Mises Institute

- Hyperinflation Weimar – AGI - American-German Institute

- The 1920s: What Hyperinflation Left Behind in Germany | Click Economic Education | KDI Economic …

- [Inflation Economics] Hyperinflation of the Weimar Republic [Comic View of Mankiw’s Economics] - YouTube

- Class e - The History of Inflation by Shin Hwan-jong - Lecture 8: Germany and Hyperinflation - YouTube

- [News Behind History] Is the Ghost of Hyperinflation Reviving?

- Pengő - Namu Wiki

- Modern Inflation②…The Disgrace of the Hungarian Pengő - Atlas News

- THE HUNGARIAN HYPERINFLATION – A LOOK INTO THE PRODUCTION SIDE - Krieger Web Services

- Hyperinflation in Hungary: 1945-1946 - SimTrade blog

- Shop like a billionaire: Hyperinflation in Hungary and Germany - Financial Pipeline

- The Collapse of Zimbabwe’s Currency Due to Mugabe’s Iron-Fisted Rule - Atlas News

- [#Naked World History] The Value of the Zimbabwe Dollar 100 Trillion is Less than a Cup of Coffee?! Ultimately, the Shocking Decision of the Zimbabwean Government - YouTube

- An Item That Cost 100 Won Rose to 2.3 Billion Won?! The Absurd Inflation in Zimbabwe - Naked World History EP.119 - YouTube

- Zimbabwe Dollar - Wikipedia

- The Minting of Dongbaekjeon and the Import of Chinese Coins - Our History Net

- Hidden Economic Stories in History: The Reconstruction of Gyeongbokgung Palace and Dongbaekjeon and Inflation

- [Economic History] The Inflation Created by Dongbaekjeon in the Joseon Dynasty [Comic View of Mankiw’s Economics] - YouTube

- Inflation⑤…The Daewongun’s Failed Currency Expansion Measures - Atlas News

- Hyperinflation (r358 edition) - Namu Wiki

- Nixon Shock - Namu Wiki

- Nixon Shock - Wikipedia

- The Nixon Shock, which declared the end of the gold-dollar convertibility… - ZZNZ

- Writing the History of Global Economic Crises through Movies (9) ‘The Post’ - The Distrusted Dollar - Econotelling

- Investment After the Abandonment of the Gold Standard

- The Oil Shock, Stagflation, and the Direction of Real Estate Assets - Brunch

- The Energy Crisis of the 1970s - Wikipedia

- Soaring Prices Amid Economic Recession: Is It the Beginning of Stagflation? | Reading the World through Economics

- The Economic History of the Oil Crisis and Price Increases… - Teen Daily Economic

- Economic Concepts | KDI Economic Education and Information Center

- Public Enemy, Inflation

- Following Economic Stories (High School Students) _16. Prices and Inflation | Bank of Korea

- Demand-Pull Inflation - Wikipedia

- The Volcker Shock in the USA - The Curious Economist

- Paul Volcker - Wikipedia

- The Incredible Volcker Disinflation - Boston University

- A Visual Guide to Inflation From 2020 Through 2023 - Congressional Budget Office

- 2021–2023 Inflation Surge - Wikipedia

- The Ukraine War Blew Up the World’s Energy Economy | Columbia Business School

- Russia’s War on Ukraine – Topics - IEA

- What Caused the High Inflation During the COVID-19 Period? - Bureau of Labor Statistics

- Fiscal Policy and the Pandemic-Era Surge in US Inflation: Lessons for the Future | Harvard Kennedy School

- The Fiscal Origin of the COVID-19 Price Surge | St. Louis Fed

- In 2021, Larry Summers Won the Inflation Debate. But His Victory Was Transitory. - Jacobin

- Inflation Wasn’t Transitory - City Journal

- The Drivers of Post-Pandemic Inflation - CEPR

- Price Inflation: What It Is and How to Measure

- www.cmcmarkets.com

- Why Bitcoin Cannot Replace the US Dollar [Investing.com] - Korea Economic

- [2021. 11. 16] The Relationship Between Coins and Inflation: news

- Inflation Era and Coins, Are Coins Really Safe? - (Society for Economic and Social Research)

- How Will Inflation Affect the Cryptocurrency Market? - Crypto.com

- [Expert Opinion] El Salvador’s Adoption of Bitcoin as Legal Tender and Its Prospects

- What Were the Results of El Salvador’s Adoption of Bitcoin as Legal Tender? | Choi Min-joo’s ‘Coin Focus’ - YouTube

- [In El Salvador, the Country of Bitcoin, People Say “I Can’t Trust It” Correspondent …

- In Argentina, Where National Currency is Collapsing Under Severe Inflation, Residents Are Also Investing in Bitcoin - Yonhap News

- Stablecoin Payments in Argentina: Fighting Inflation with USDC and USDT - TransFi

- Stablecoins Now Used in Credit Cards, Putting Bank Deposits at Risk

- State of Stablecoins, Part 2: The Shift Toward Institutional and Global Use - Bastion

- What Argentina, Nigeria, and Turkey Are Really Telling Us About the Future of Money - Medium

- Why CBDCs Are Called the Future Revolution - Yonhap Infomax

- Are Central Bank Digital Currencies (CBDCs) the Future of Money? - Korea Economic

- Review of the Necessity of Central Bank Digital Currency (CBDC) and Related Issues

- The Impact of Issuing Central Bank Digital Currency (CBDC) on the Transmission Path of Monetary Policy: Analysis through DSGE Model - Bank of Korea

- Will Digital Currency Complement the Dollar as the Reserve Currency? - Atlas News

- business.columbia.edu

- Did Deglobalization Add to Inflation Woes? - MSCI

- Greenflation: Challenges and Solutions in the Energy Transition - tanahair.net

- Greenflation and the Role of Prices in Clean Energy Transitions - The Diplomat

- Will Greenflation Cancel the Green Transition? - Greeneration Foundation

- We’re Getting Older, and the Labor Market Shows It - Federal Reserve Bank of Atlanta

- Population Aging, Wage Growth, and Inflation

- Global | The Changing Effects of Demographics on Inflation | BBVA Research