In Uncertain Times, Here’s Why ‘Room for Error’ Truly Saves Your Life

“Everyone has a plan until they get punched in the mouth.”

We humans love to make plans, don’t we? Without fail, we set financial goals at the start of a new year and draw up blueprints for our lives. But let’s be honest: do those plans ever work out exactly as intended? Probably not. The most crucial point here isn’t to blame yourself when a plan goes awry. The real key is to accept from the outset that all plans are bound to go wrong. As best-selling author Morgan Housel insightfully put it in “The Psychology of Money,” the most important part of any plan is the plan for when the plan doesn’t go according to plan.

This isn’t about pessimism. It’s about a stark, unflinching realism. It’s the wisdom of humbly acknowledging the existence of immense luck and risk, forces beyond our sole control. The most primal yet powerful tool for navigating this sea of uncertainty is ‘Room for Error’. This isn’t just about having a little “spare cash.” It’s a survival technique – intentionally creating a buffer between the worst-case scenario and what you can actually withstand.

So, why do we so easily dismiss this simple yet potent concept of ‘room for error’? What psychological traps continually push us onto thin ice? In this article, we’ll delve into the essence of ‘room for error,’ moving beyond personal finance to explore engineering, military strategy, and the rise and fall of corporations. We’ll also contemplate specific psychological methods for not just understanding, but truly embracing and embodying this survival skill as something profoundly important, almost to the point of reverence.

From Bridge Design to the Battlefield, the Laws of Survival Are the Same

‘Room for error’ isn’t just a stingy trick for personal finance. It’s a universal wisdom embedded at the core of every complex system that must withstand unpredictable stress.

The Engineer’s Perspective: The Undeniable Number, ‘Factor of Safety’

Let’s take a look at the world of bridge engineers. For them, there’s an absolute concept called the ‘factor of safety.’ If a bridge’s factor of safety is 3.0, it means the bridge is designed to withstand three times the heaviest load it’s expected to carry under normal circumstances. Is that wasteful? Not at all. It’s the most humble acknowledgment of human limitations in perfectly predicting the future. Unforeseen heavy rains, microscopic cracks in materials, changes in the ground nobody knew about… Engineers know that such ‘unknown unknowns’ always exist. The factor of safety is the minimum courtesy to that unknown realm, a buffer that protects our lives. Our financial plans should, in fact, be treated just like these bridges.

The General’s Perspective: The Decisive Card in Victory and Defeat, ‘Strategic Reserve’

It’s the same in military history. A competent commander never plays all their cards at the outset. Consider the Battle of Kursk, which shifted the tide of World War II. Predicting the German offensive, the Soviets dug deep defensive lines while holding their elite armored units in reserve – a ‘strategic reserve’. When the German thrust blunted after repeated battles, they deployed this fresh reserve, held back for precisely that moment, and delivered a decisive counterpunch. The result? Complete shift in the war’s initiative.

The “idle cash” in your bank account isn’t lazy money eroding returns. It’s your ‘strategic reserve.’ It allows you to aggressively counterattack when the market crashes (revealing the enemy’s weakness) while others panic and sell, and it serves as your ultimate safeguard, preventing your entire life plan from collapsing in the face of sudden job loss (an unexpected ambush).

Why Do We Ignore Room for Error? The Traps Hidden in Our Brains

It’s so rational, yet why do we constantly try to walk on thin ice? The reason lies in systematic bugs inherent in our brains – ‘cognitive biases’.

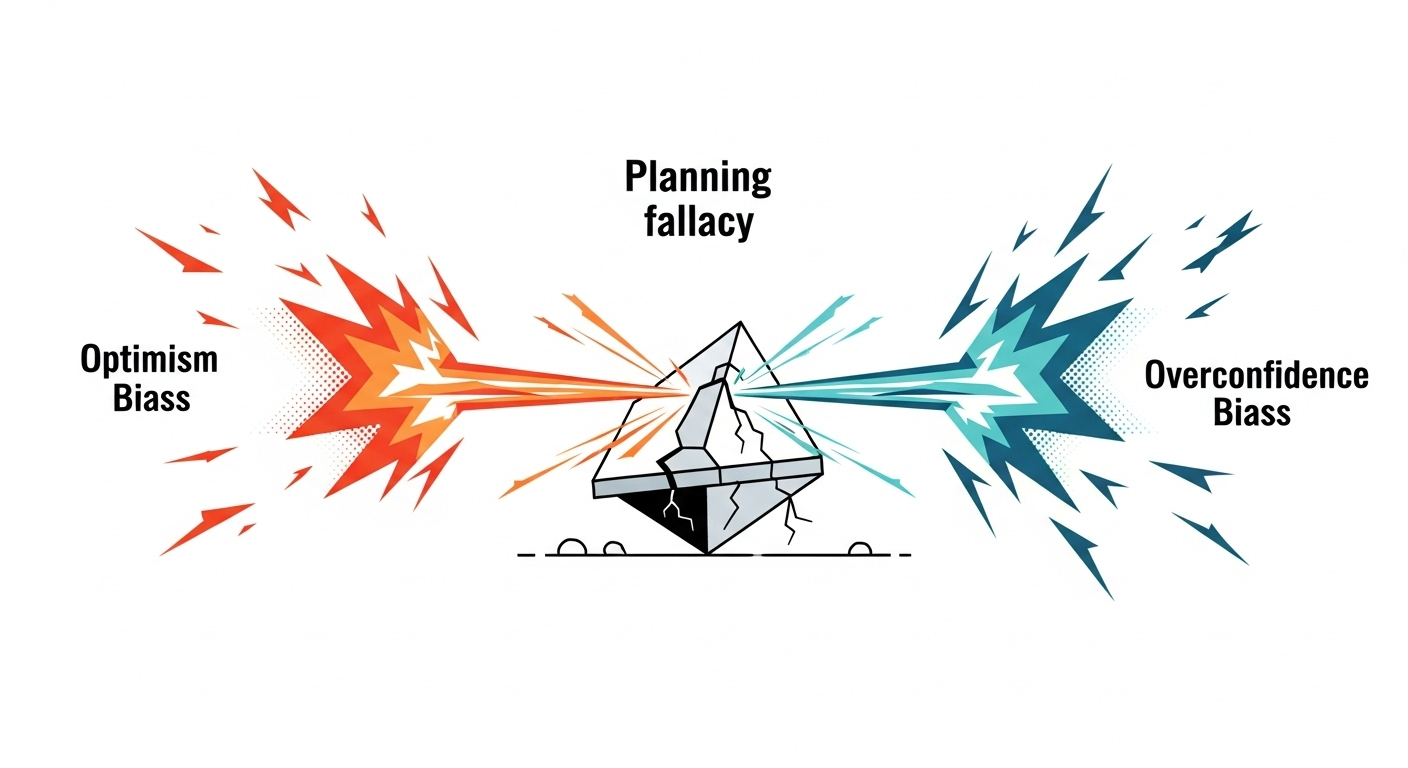

The Planning Fallacy: The Optimistic Designer Within

As psychologist Daniel Kahneman revealed, we suffer from a chronic ailment known as the ‘Planning Fallacy’. This is the tendency to habitually underestimate the time, cost, and risks involved in future tasks. The Sydney Opera House is a prime example. The initial plan to build it in six years for $7 million ballooned into 16 years and a cost 15 times higher due to unforeseen problems. Aren’t we the same? Despite countless past planning delays, we whisper to ourselves, “Well, this time will be different,” and create plans that are impossibly tight.

Optimism and Overconfidence: “Surely, That Won’t Happen to Me?”

Two fuels make this planning fallacy even more dangerous: ‘optimism bias’ and ‘overconfidence bias’. Optimism bias is believing that the probability of bad things happening to us is lower (“I won’t have an accident,” “I won’t get sick”). Overconfidence bias is overestimating our abilities (“My investment skills are above average”). When these two combine? Risks like job loss, illness, or market collapse are conveniently ignored, naturally leading us to feel no need to build up emergency funds. Especially when we leverage ourselves with debt we can’t handle, “trusting our own skills,” ordinary risks can instantly transform into fatal dangers leading to bankruptcy.

These cognitive biases reinforce each other, creating a terrifying ‘cycle of ruin’ that makes the concept of ‘room for error’ invisible to our eyes.

What Happens When There’s No Buffer Zone (Psychological and Financial Vicious Cycles)

Living without a buffer zone isn’t just about lacking money. It gnaws at our minds, paralyzes our rational judgment, and ultimately pushes us into a inescapable vicious cycle.

The Downward Spiral

For someone living without a buffer, a sudden notification of job loss isn’t just a financial problem; it’s an overwhelming sense of powerlessness, having lost control of their life. Extreme stress induces ’tunnel vision’, which drastically narrows our perspective. We have no room to consider long-term solutions, and all our mental energy is consumed by the immediate need to cover next month’s credit card bills. This eventually leads to behaviors like retail therapy to cope with stress or outright financial avoidance, like ignoring bills, further worsening the situation.

The Betrayal of Leverage: The Orange County Bankruptcy Story

A textbook example of what happens when a massive organization ignores room for error, not just an individual, is the 1994 bankruptcy of Orange County, California. Robert Citron, the treasurer at the time, borrowed an enormous amount of money – debt (leverage) – betting everything on a single scenario: that interest rates would continue to fall. But in 1994, when the Federal Reserve began raising interest rates, what happened? With no safety net, his portfolio recorded an unimaginable loss of $1.6 billion, ending in the tragedy of the largest municipal bankruptcy in U.S. history. It was a stark lesson in how overconfidence-fueled leverage can transform ordinary market fluctuations into a catastrophe.

The Power to Turn Crisis into Opportunity, Room for Error and Resilience

But here’s the thing: room for error isn’t just a passive shield against the worst. It’s a potent source of proactive strength that can turn crises into springboards for growth. At its heart lies ‘psychological resilience’.

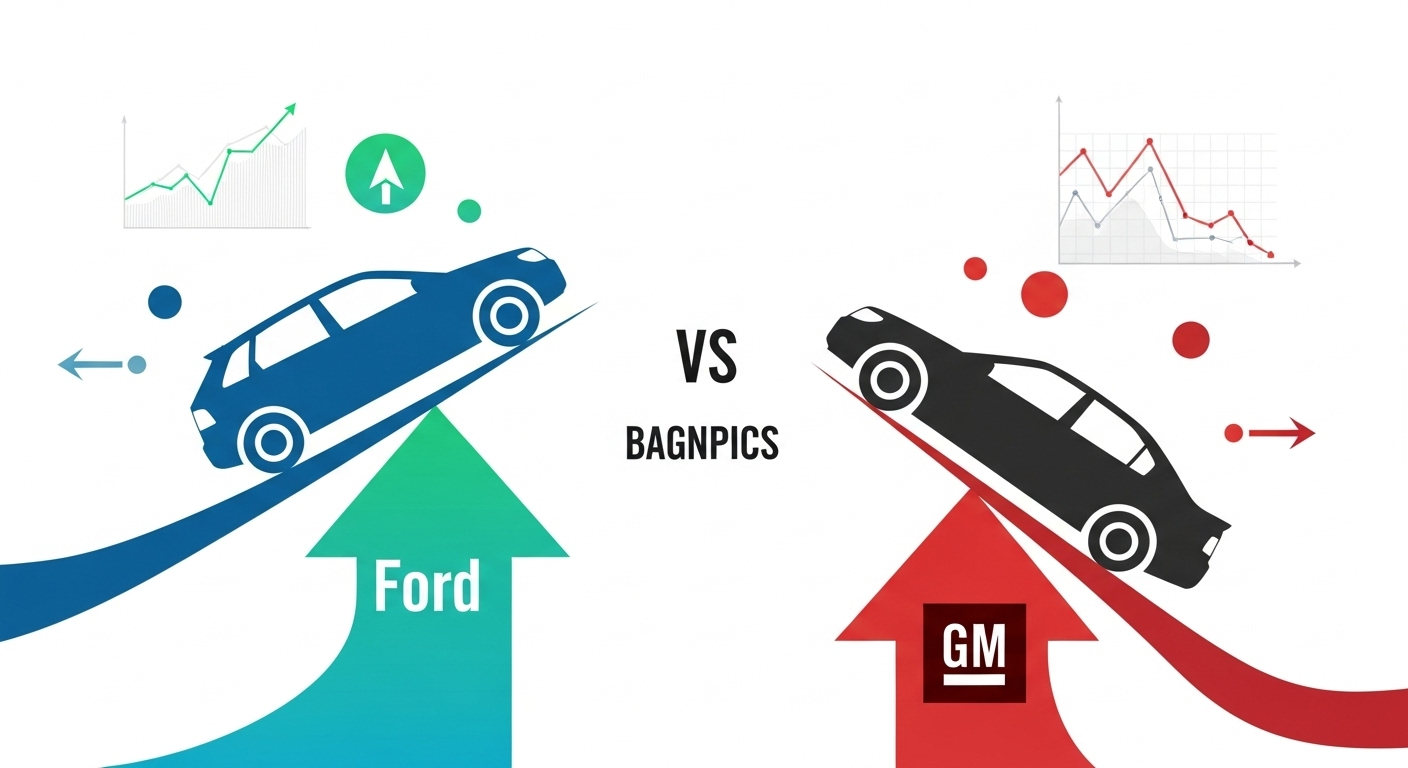

The 2008 Financial Crisis: The Divergent Fates of Ford and GM

Perhaps the most dramatic example of how room for error dictates a company’s fate is the story of Ford and GM during the 2008 financial crisis. Two years before the crisis, in 2006, Ford CEO Alan Mulally borrowed a staggering $23.6 billion by pledging all the company’s assets as collateral. While criticized at the time for “going too far,” this decision ultimately proved to be a ‘stroke of genius’ that saved the company.

In 2008, as the financial markets froze, GM, lacking cash (room for error), had to seek government assistance and file for bankruptcy protection. But what about Ford? Thanks to the massive cash reserves it had built, it not only weathered the storm without government aid but also continued investing in new car development during the crisis when everyone else was hunkering down. As a result, Ford actually increased its market share after the crisis. Ford’s room for error made the company ‘financially unbreakable’ and transformed a once-in-a-century economic crisis into a golden opportunity to outpace competitors.

As this illustrates, room for error acts as a ‘shield’ against uncertainty, but also as a ‘spear’ that allows you to leap higher than others by leveraging that very uncertainty. It is the most powerful strategic asset.

Realistic Ways to Overcome Psychological Traps and Build Room for Error

Our brains are instinctively wired to ignore room for error. Therefore, to overcome this instinct, we need conscious strategies and systems.

- Try a ‘Pre-Mortem’: When you’ve made an important financial plan, close your eyes and imagine this: “One year from now, this plan has failed miserably.” Then, write down the reasons for failure as specifically as possible. Instead of the vague question, “Will it succeed?”, the question, “If it already failed, why on earth did it fail?” calms our internal optimism bias and makes potential risks much more vivid.

- Utilize the ‘Three-Point Estimation’ Technique: Don’t settle for a single target. Consider three scenarios: ‘Best Case (Optimistic)’, ‘Worst Case (Pessimistic)’, and ‘Most Likely Case’. Then, set your plan’s baseline on the ‘Worst Case Scenario’. This intentionally injects pessimism into the planning stage, creating balance.

- Worship ‘No-Reason Savings’: As Morgan Housel emphasizes, you need savings for no specific reason, beyond goals like “saving for a wedding” or “buying a house.” This is because life’s biggest shocks always come from places we never even imagined. This ‘money without a reason’ is the ultimate room for error against those unknown risks.

- Trust ‘Systems’, Not Willpower: The resolution to “save more” rarely lasts more than three days. Willpower has clear limits. Instead, create a system where a set amount is automatically transferred to savings or investment accounts as soon as your paycheck arrives. Moving saving from the realm of ‘decision’ to the realm of ‘default’ is the most reliable and powerful way to consistently build room for error without emotions getting involved.

Conclusion: The Psychology of Wealth for Endurance, Not Prediction

Building room for error is a wise attitude that combines the humility of not being able to predict the future, the caution that circumstances can always worsen, and the long-term optimism that if you just survive, the magic of compound interest will help you.

Ultimately, financial success isn’t about achieving the highest returns. It’s about possessing ‘financial robustness’ – the ability to withstand any crisis without your entire life being shaken. In the long game of wealth accumulation, the ability to endure is the single most important skill that overshadows all others. And room for error is the unique lifeline that guarantees we can endure that time of patience.

Don’t try to predict. Just prepare to survive long enough to withstand any storm. This is the most essential, true psychology of wealth for us living in a world full of volatility.

References

- Housel, Morgan. The Psychology of Money.

- Kahneman, Daniel. Thinking, Fast and Slow.

- Buehler, Roger; Griffin, Dale; Ross, Michael (1994). “Exploring the ‘planning fallacy’: Why people underestimate their task completion times”. Journal of Personality and Social Psychology. 67 (3): 366–381.

- Major media reports and historical analysis reports on the 2008 financial crisis, Orange County bankruptcy, Battle of Kursk, Sydney Opera House construction, etc.

- Engineering and military strategy literature (concepts of factor of safety and strategic reserve)