part2. The Architecture of Trust: Deconstructing Stablecoin Models and Lessons from Failure 📉

While stablecoins aim for “stability,” the methods used to achieve this stability, the “trust mechanism,” vary significantly across models. This difference determines the strengths and weaknesses of each model.

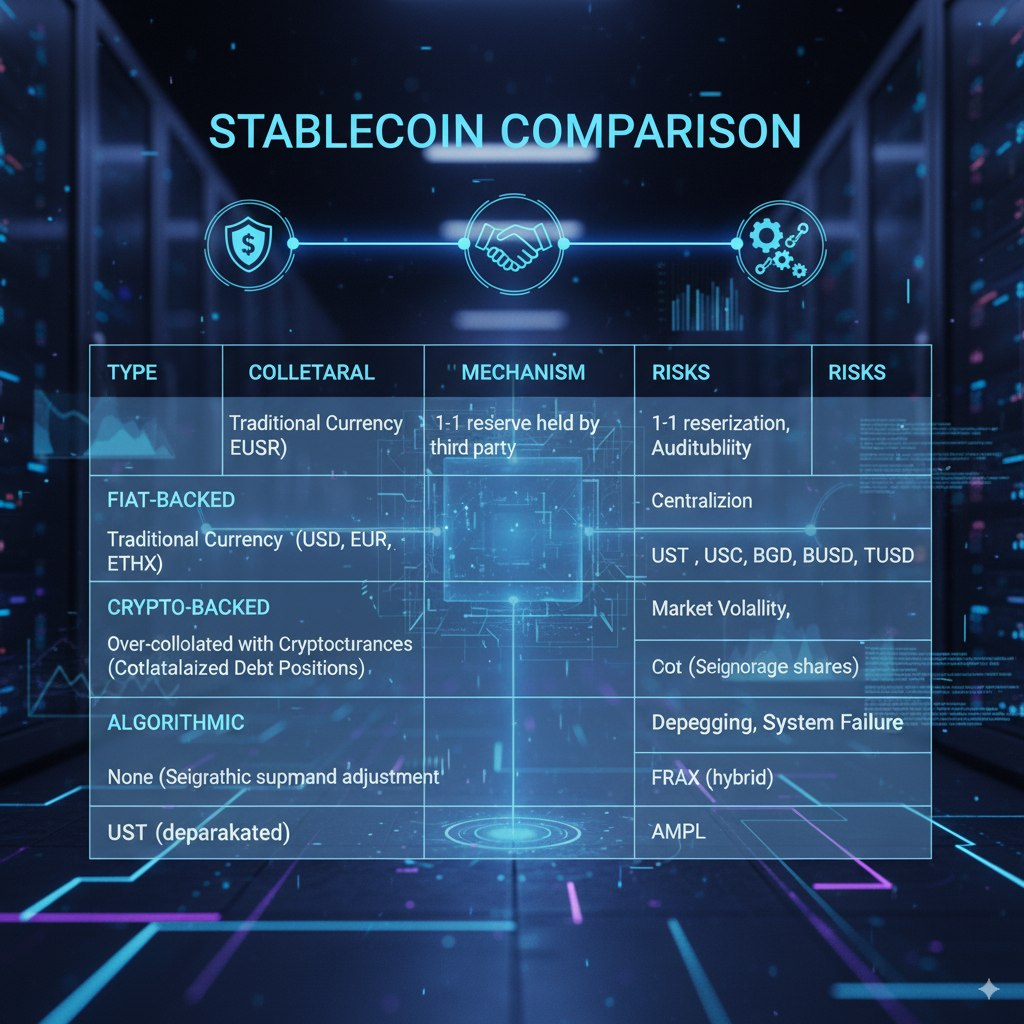

Centralized Stability: Fiat-Collateralized Models

The most intuitive and dominant approach in the market is to use fiat currency directly as collateral. In this model, a centralized issuer deposits one dollar in cash or equivalent safe assets in a bank account for every stablecoin token issued. The token’s value is maintained based on the user’s belief that they can present their stablecoin to the issuer at any time and receive the equivalent fiat currency back at a 1:1 ratio.

- USDC (USD Coin): Issued by Circle, it prioritizes regulatory compliance and transparency. Reserves are primarily composed of cash and short-term US Treasury bonds and are transparently disclosed through regular audits by a global accounting firm. This approach has earned significant trust from institutional investors, driving its rapid market share expansion.

- USDT (Tether): Boasts the largest market capitalization in the market but has historically been at the center of controversies due to issues with reserve transparency. Tether states that its reserves are diversified, including not only cash but also commercial paper, collateralized loans, corporate bonds, precious metals, and even other investment assets like Bitcoin. This suggests potentially higher risks compared to USDC.

The trust in this model relies entirely on faith in the issuer and external auditors. The biggest risk is counterparty risk. If the issuer mismanages reserves or goes bankrupt, the stablecoin can lose its value.

Decentralized Resilience: Crypto-Collateralized Models

More faithful to the philosophy of decentralization, this model minimizes reliance on centralized issuers or traditional financial systems. A prime example is DAI, issued by the MakerDAO protocol.

- How it Works: Users deposit volatile cryptocurrencies like Ethereum (ETH) as collateral in a smart contract vault (Vault) instead of dollars. They can then mint (borrow) DAI up to a certain percentage of the deposited collateral’s value. The key is over-collateralization, which forces the collateral value to always be significantly higher than the debt value (e.g., over 150%), acting as a buffer against collateral price drops.

- Automated Liquidation: If the collateral asset’s price plummets and the collateral ratio falls below a predetermined “liquidation ratio,” the smart contract automatically sells the collateral on the market to forcibly repay the loan. This mechanism is the last resort for maintaining the solvency of the entire system.

Trust in this model stems from transparently disclosed and audited smart contract code and mathematical algorithms. Anyone can verify how the code works without needing to trust a centralized entity. However, the main risks are smart contract risks (bugs or hacking vulnerabilities in the code) and systemic risks that can trigger cascading liquidations during sharp market crashes.

Collateral-Free Ambition: The Demise of Algorithmic Stablecoins

This ambitious and experimental model attempted to peg its value to $1 solely through algorithmic control of the money supply, without physical collateral. This system typically used two tokens: a stablecoin (e.g., UST) and a sister coin designed to absorb price volatility (e.g., LUNA).

- The Terra-Luna Collapse of 2022: In the Terra ecosystem, 1 UST was algorithmically guaranteed to be exchangeable for $1 worth of LUNA. If the price of UST fell, arbitrageurs could buy UST cheaply and exchange it for $1 worth of LUNA within the system, profiting in the process. This would burn UST, reducing its supply and recovering its price. However, in May 2022, a massive sell-off of UST caused its price to drop significantly below $1. To restore the peg, the algorithm began minting an exponential amount of LUNA, causing LUNA’s price to crash and spreading fear that LUNA could not back UST’s value. Ultimately, UST holders initiated a massive “bank run,” and the value of both tokens converged to almost zero within days, leading to their collapse.

- The “Death Spiral”: The Terra-Luna incident proved that collateral-free algorithmic stablecoins were built on the unrealistic assumption of perpetual market trust and demand for their sister tokens. In times of crisis, trust evaporates, and the algorithm only serves as a catalyst for collapse. Following this event, the market has almost completely lost faith in this model, with many experts deeming its structure fundamentally similar to a Ponzi scheme.

Death Spiral

Each stablecoin model demonstrates the inherent trade-offs between stability, decentralization, and capital efficiency – the “stablecoin trilemma.” Fiat-collateralized models sacrifice decentralization for stability, while crypto-collateralized models endure capital inefficiency (over-collateralization) for decentralization. Algorithmic models, in their attempt to achieve all three, ultimately lost stability itself and failed. The current overwhelming preference of the market for fiat-collateralized models like USDC and USDT clearly shows that users prioritize practical stability and ease of use over pure decentralization.

Continues to part3. Money Without Borders, Sovereignty With Borders: The Battlefield of the Digital Currency Cold War.